November: A 13% Day for Banks and What's Next

It's not taking 3 months for the market to price Trump in this time. The Most Interesting Bank in the World, Merchants of Indiana (MBIN), Arbor's advantage, Optimum Bank re-review, Bitcoin miners

Good morning,

In this note:

Parsing the Trump trade, and an inefficiency

The most interesting bank in the world.

Merchants Bank (MBIN) seems complicated, but is actually simple

Arbor (ABR) has an advantage in lending relative to banks. It’s another reason for banks to look beyond traditional banking.

Do bitcoin miners / “developers” count as financials? Yes. We look at the numbers for three of them.

Keeping it simple: I sometime get feedback that 5 Points is written in bank nerd language. If you just want to read the bold text that should be a reasonable shortcut for novices or the time-constrained.

Optimum Bank clarification: Last edition I profiled Optimum Bank (OPHC) as selling shares at $4.75 when tangible book value was close to $9, a no-no. While it’s true that Optimum is selling shares at $4.75 and that tangible book is ~$9, it’s also true that Optimum has a complicated ownership structure that hides 50% book dilution. There are large convertible preferred stakes out at strikes between $2.50 - $4.50, not always convertible at the holder’s option, which makes look through tangible book closer to $4.50, a more forgivable level.

Optimum runs an interesting merchant advance servicing business and is led by a hustling nursing home magnate as executive Chairman. It’s still not for me at the moment but they are doing some things well.

1. What is the Trump trade in financials?

I covered this some back in February when nobody cared but times have changed to say the least; let’s go over loan growth, regulation, and mergers among others.

Before we do, a word from the horse’s mouth with a 3-minute snippet from a long forgotten press conference that not many bothered to watch on Youtube:

We can particularly appreciate the 45 second mark when he discusses the problems of Dodd Frank and his desire to roll it back in the first 100 days - “It’s out of control… We want to get out and make our country work properly again” followed by “You are very special people doing a very special job.”

This is not something we would ever hear from his opponent but now that banks are popular again, keep in mind the next 6 months are not just going to be “so much winning.”

It will take some time to trickle through to our sector. What to expect:

Possibly higher loan growth. Regardless of who won, we would get this due to a clearer outlook.

The business of America is again business, but some of this will depend on interest rates, and some reforms will take a while to adjust to. For example Trump in the past has preferred to pull funding from HUD and create incentives for private sector building instead for lower income. Banks may need to rejigger their process to adapt to this.

Last edition profiled a few banks with clearer path to growth, like TBBK, CCB, NEWT but post-election the majority of the sector should benefit; it might just take a while to be seen.

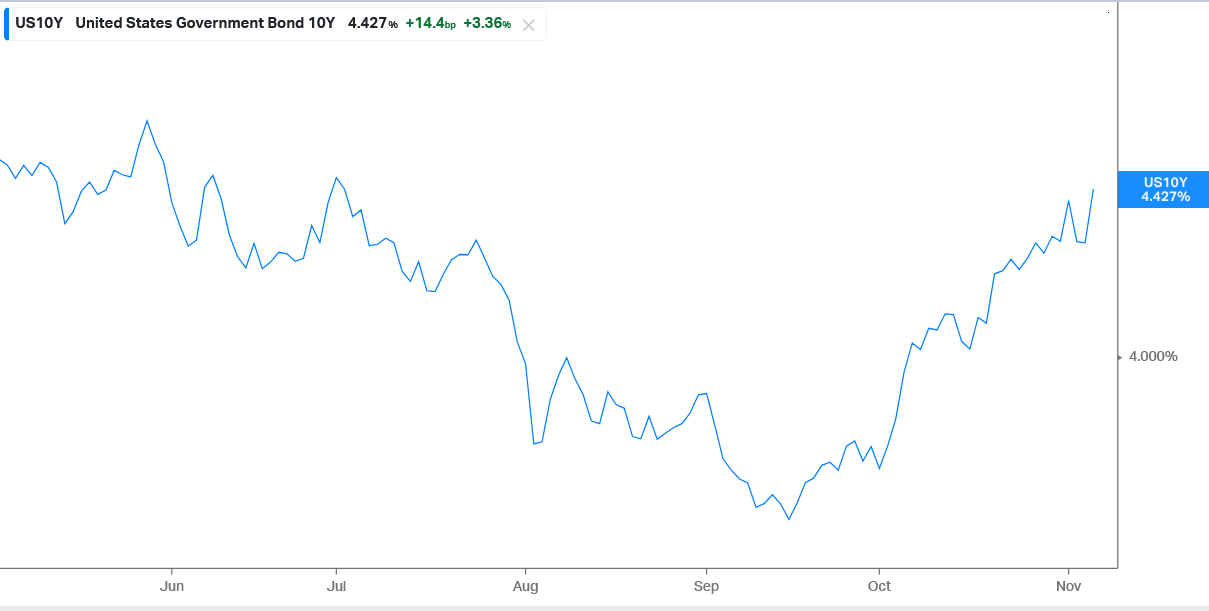

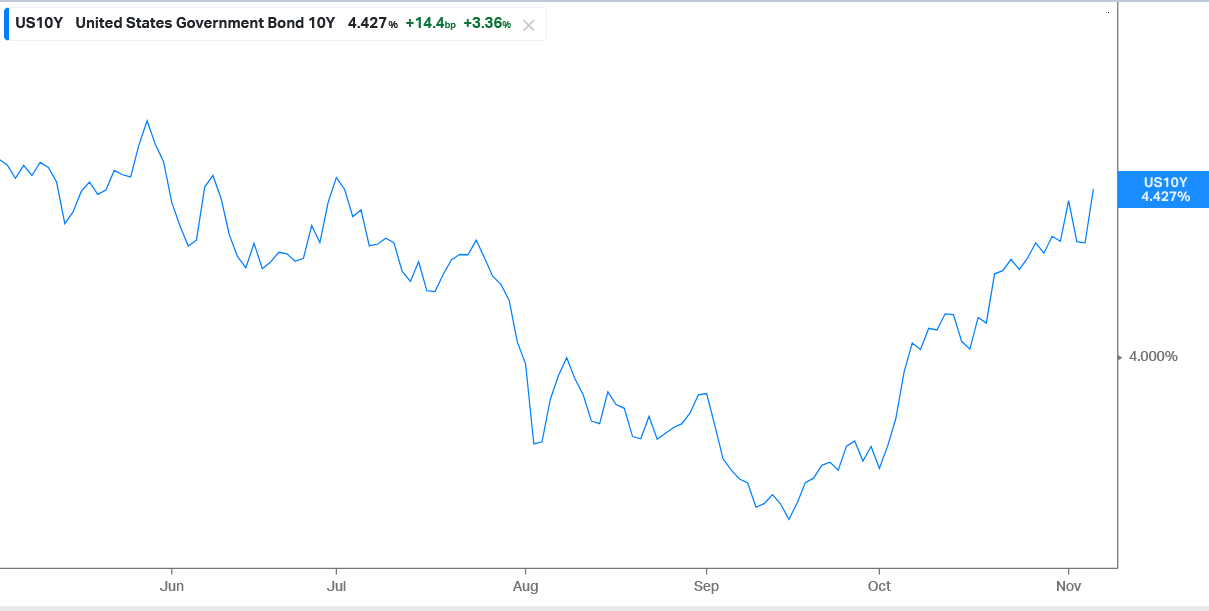

Higher long rates. After the sugar high, this is a serious issue.

The market is rightfully cautious on whether Trump can grapple with out-of-control deficits and stubborn inflation.

Today the job of Treasury Secretary is a de facto “authority over the global yield curve”. The Secretary rolls an astounding $28trn.

We can see that Secretary Yellen chose to pass the job to the Federal Reserve and put almost all the issuance in bills, to avoid concerns around a possible 5-6% 10 year yield:

Perhaps the new Secretary will do the same but markets should be prepared for even a modest increase in long end issuance to move longer rates above 5%.

Koyfin To keep this process orderly, we can cheer on the promised Office of Government Efficiency initiative. Every hundred billion dollars of waste matters!

Mergers

These might explode in a good way.

Recent 5 Points issues covered all the impediments that have cropped up for mergers lately, including congressional hearings for mergers, surplus capital charges, and delays because of community groups.

We may be back to 6 month merger approvals, which from an investor standpoint is beautiful.

This helps merger targets like Homestreet (HMST) or perhaps a few Virginia banks including (BRBS), among many others. Pennsylvania, New York and California are likely to be active.

Taxes: One would hope the corporate rate doesn’t fall to 15% until major spending cuts plus Medicare / Defense / Disability reforms are enacted, but it’s likely to get proposed regardless and this fact won’t hurt bank share prices.

Large banks vs small banks. Dodd Frank created a regulatory apparatus that cemented too big to fail. Trump’s administration sought to soften it. In 2023 it was cemented again, and nothing has happened since.

Do we dare dream of higher FDIC insurance limits? I can think of nothing more bullish. I would also expect Intrafi gave tens of millions to politicians to keep it from happening.

On the technical side, today we can participate in mis-pricings after yesterday’s ETF rip.

There is a small index that tracks smaller, OTC banks. Yesterday it rose 2.8%. If you are looking for banks to buy, try some on the OTC.

In contrast, the ETF that tracks exchange-listed banks rose 13%+. That seems inefficient in comparison.

It is not a policy action but we include it in the wash of the Trump effect…

Take advantage - the OTC names often catch up over time.