Mid September: An end to bad bank regulation?

Why Axos has outperformed 2000%; why humans can beat machines in bank investing; the bank / private credit opportunity as practiced by Newtek; Avoid the Northways.

In this note

Punitive regulations have been a challenge to the bank sector since the Obama administration. The problem may be fading (with a discussion of BaaS and brokered deposits).

The machines have taken over equity markets, but they do a clumsy job with banks. A look at Hanmi (HAFC) and why humans often still win.

Axos Bank (AX) has outperformed its benchmark by 2000%+ since 2007. The proxy shows how.

The evolving world of private credit in banks: Newtek’s (NEWT) angle.

Investing in low-quality bank merger targets is hard; Northway’s (NWYF) cautionary tale.

I ran out of room to address Esquire’s (ESQ) engrained advantage and a discussion of TC Federal (TCBC); look for those in future editions.

1) Are arbitrary, punitive bank regulations behind us?

This is Rohit Chopra; he runs the Consumer Financial Protection Bureau

He is also on the board of the FDIC after Jelena McWilliams was inexplicably removed in a political coup. In each role, Chopra was not elected but nonetheless took on substantial rule-making authority.

Much of what Chopra handles is appropriate. A glimpse at CFPB’s recent enforecement actions confirms the stereotype that the consumer finance industry is filled with goons.

But his CFPB tenure has been controversial and his FDIC coup was inappropriate. Further, Chopra is the mascot for an FDIC that increasingly is leaning political. It is:

Not doing its job with mergers. For decades it took 6 months for banks to combine. Today, for no explained reason it usually takes over a year. This is incompetence at best, but bias against the industry seems more likely.

Proposing rules like the brokered deposit overhaul, which basically penalizes fintechs and their bank sponsors for attempting to access the banking system. There is no question that actors like Synapse and Evolve need to be removed. This rule hurts the good and bad actors instead.

Fortunately OCC Comptroller Hsu must go along and needs actual data to pass a rule, and with brokered deposits I’m not sure there is any because fintech deposits held solid in March 2023. Hsu isn’t on board with political vendetta regulation, so it may not ultimately be enforced regardless. Bless him. We will see.

This brings us to FDIC head Martin Gruenberg, Chopra’s partner in politicized regulation.

It’s beyond the scope of this note but in calling around on this topic I heard stories of how Gruenberg’s brokered deposit proposal was part of a vendetta to roll back Trump policies. Many believe the vendetta stems from conservatives leaking the Gruenberg FDIC sex and harassment culture story to the WSJ.

With this stage now set, relief from this behavior may be at hand! Multiple sources suggest the recent Chevron deference ruling could be the industry’s ace in the hole.

As many of you know a few months ago the Supreme Court ruled that fishermen did not have to pay about $710 a day for government workers assigned to their boat to ensure they fished legally. In doing so they redrew the concept of whether agencies got to interpret a statute as reasonable, or courts. Congress should do these jobs but they seem to focus on squabble and spend.

Raymond James’ DC analyst suggested at the recent Raymond James Banking Conference this will at very least help in watering down the brokered deposit rule.

The law firm Venable LLP writes:

...banks and other parties may now seek to challenge what they perceive to be agency overreach or error, without having to overcome deference to the agency’s interpretation of its statute.

Whatever the outcome, the point is that just the threat of prolonged litigation can blunt the regulatory overreach sword.

OK but why care? How do we make money? The BaaS angle.

The brokered deposit rule has been seen as a risk to BaaS banks, which create APIs to give nonbanks direct access to their balance sheet (or indirect, if they are doing it incorrectly, but this is stopping). If you are new to 5 Points, I believe BaaS banks are among the best risk reward in the sector.

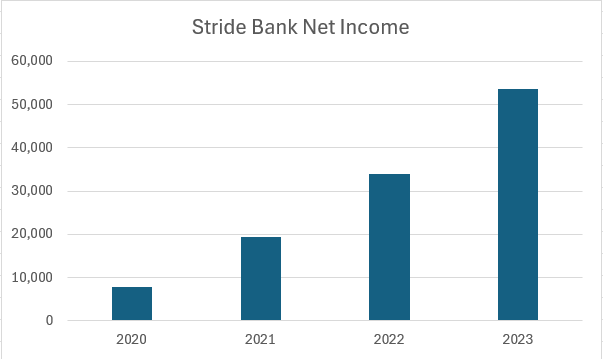

Let’s take a look at Stride Bank as an example, which may come public at some point. They bank Chime credit card and deposit verticals. Stride has asset quality issues and 90% non-interest bearing checking. With the income trends below, I’ve seen worse.

BaaS banks are a “heads they win, tails they don’t lose” proposition in the sense that they collect toll fees from fintechs and other partners for banking system access, plus get the same spread income as normal banks. The difference is they often get the partners to reserve for loan losses as well.

In exchange, the BaaS banks have to provide compliance, which can be enormously difficult. About 10-15 banks have spent the time and money to get it right, while many others have not. Because of the others, including standout Evolve Bank and Trust, we got the baby / bathwater vendetta rule that potential hero Hsu and our Supreme Court friends may have blunted.

Keep an eye on public BaaS banks with strong prospects, including TBBK and CCB profiled in prior editions of this note.

2) Machines vs humans investing in banks - why humans can still win

Noted investor Cliff Asness recently wrote a paper about how markets were becoming less efficient with the rise of indices and social media.

When it comes to banks, I think he’s right, and I believe the inefficiency is increasing over time.

First, let’s discuss outperforming managers in the bank sector.

The right kind of active management and banks can do extremely well over time. I’m not allowed to write here what Colarion performance (I would have to certify this as an advertisement and confirm readers as accredited) but we are working on a portal that will allow us to do that.

What I can say is that Colarion’s performance makes it relevant, and I believe the firm has some similarities to my friend Derek Pilecki’s Gator Capital.

Gator Capital is a financials specialist in process of closing his fund given its run of outperformance. Derek and I often have similar views and we both take advantage of superior management styles or special situations in the sector. I believe Fourthstone, Down Range, Blue Lion, and Mount Grey among several others are also in this category of strong performance from financial sector inefficiencies.

I believe this outperformance is getting easier over time, for two reasons.

a) Index funds continue to gain share and are 100% forced buyers. Forced buyers are at a structural disadvantage. I believe the disadvantage is minor with large caps, but greater at smaller / less liquid companies, and materially so around index reconstitutions.

b) Quants continue to gain share. These quants can move large amounts of money. Sometimes these trades are done in a sharp manner off valuable cues, and with little market impact. Other times they are done clumsily, and always without an understanding of management quality or insights on the progress of the business.

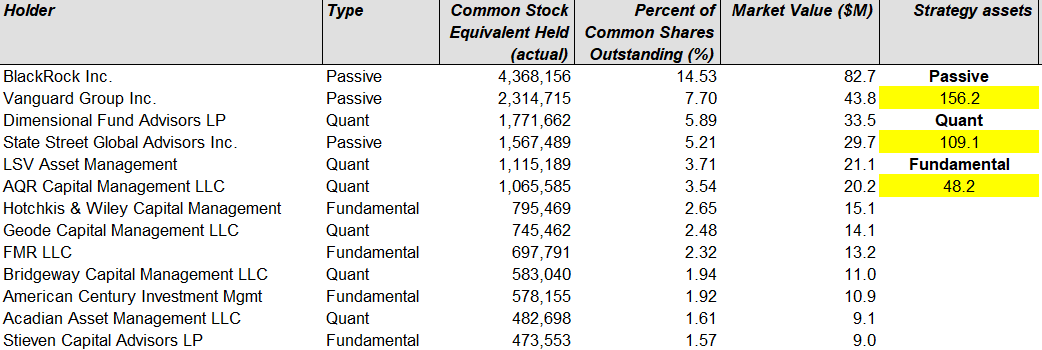

As an example of the numbers we are discussing, see below the largest holders of Hanmi (HAFC), a little bank I am visiting with tomorrow:

In other words, for every dollar among the largest holders that is speaking to management, five dollars ignore management quality / strategy and half the money is completely oblivious.

Quant and index are the best way to scale an asset management business. I don’t know that they are the best way to make money in small company investing.

Finally, as these trends continue, it can take longer for value to be recognized. Every time I meet with CCB CEO Erik Sprink I wonder when the message will get completely out. Many of you likely have similar examples but I’ll use a different one below.

Fifth District (FDSB).

Fifth District is a New Orleans converted thrift with bad financials. It runs a 2% margin, 100% efficiency ratio and no net income. No quant strategy based off income statement figures would assign much value to FDSB.

At $60mln market cap it isn’t in any index yet except perhaps the Vanguard Total Market Index, so there is no passive buying pressure for FDSB.

Third, the owner base, which is largely recent depositors, has incentive to sell so that they can participate in the nearby Fidelity conversion, profiled in the prior edition of 5 Points.

FDSB is an orphaned loser.

However FDSB has a CEO who is motivated to return capital to shareholders and at 46% of tangible book, a $57mln market cap vs $130mln of tangible equity, could repurchase the market cap 2x and still have sufficient capital left over.

Again I don’t make stock recommendations here but the point is only the folks engaging with management and cross-checking proxies and insider behavior would have an understanding of this potential. I’m glad I did that.

Mr. Asness is onto something. Many sector speclialists aren’t guessing on macro data. We are looking at blindspots and reading documents other people don’t want to read to play special situations. This can be more effective than forced-buyer or data-only strategies.

for another example, we can look at…