Mid April: A Tour of Higher Rates Jail

also: banking as a service survivors, CCB, FIBK, and the rate sensitive screen

In this note:

Touring “higher rates jail” - some of the financials more sensitive to a sustained higher-rate yield curve.

Banking as a Service consent orders: regulatory issues are widespread but those still unaffected are building a moat.

Coastal Bank (CCB) has an opportunity to be among the better risk / rewards in banking.

First Interstate Bank (FIBK): do outside shareholders come second?

A quick rate sensitivity screen for banks.

Brief notes:

Charity: We sent the $5k to Ronald Mcdonald House on March 28. Thank you to subscribers who supported this.

We all know that RMH fulfills a great need by housing children whose families are already dealing with significant health bills. However, every time I wire money to Regions Bank I wince a little. A theme of this note is the contributions of smaller banks; perhaps by extension it would be good to find smaller charities that support those same banks.

If a subscriber has a great little children’s charity that banks with a forward-thinking smaller bank then please let me know so I can add them to the list.

The pull of fintechs to look more like banks.

Robinhood is offering 3% cash back on their credit card. Chime pays you a day earlier. SOFI and Robinhood are both offering 4-5% on savings, and low fees.

Hold that last thought. You’re not a real bank unless you charge NSF and inactivity fees, and penalize clients $100 for transferring brokerage assets out, as SOFI just quietly announced. Welcome to the bank club, Sofi!

Robinhood likewise is not going to make any money paying 3% back on swipes plus sharing a material portion with Coastal Bank, so we might expect similar switch on that platform over time as well.

The laws of financial physics state that core software platforms and payment processors like FIS and Fiserv will make their fees on swipes and ledgers regardless of who offers the service. That is much of why banks charge their list of fees in the first place.

On to the notes:

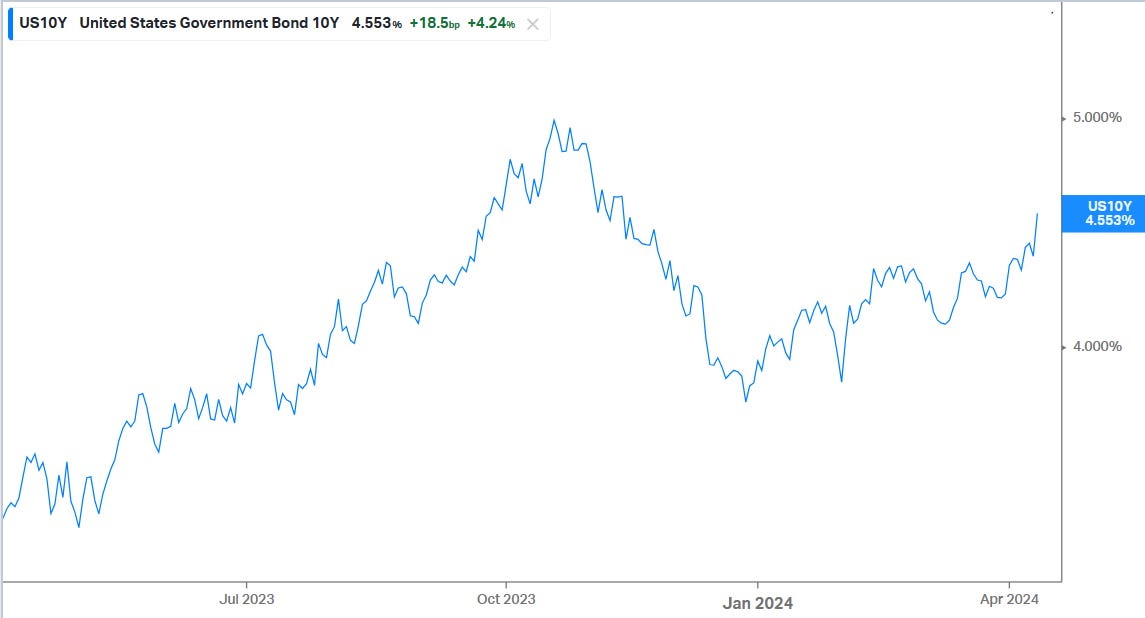

1. In light of recent rising bond yields, we take a tour of “rate jail” - companies more sensitive to the recent move in rates.

Today we have a surplus of generalizations about the damage higher rates cause to financials, but a shortage of people actually gathering data and reading 10ks to sort through specific examples. This bullet point does some of that digging.

Specifically, these companies typically lent heavily on CRE in 2021 and 2022 and now are hoping for relief from capital markets, on bond marks, or some other benefit from lower rates.

One note before we begin our tour - you will not find Hawaiian banks or rural depositories on this list. Their trapped bonds are aging well as they move slowly to par and typically carry no credit or refinance risk.

Rather we are looking at CRE lenders hoping to sell buildings, get access to funding, and otherwise buy time to stay alive. Stressed CRE loans tend to age poorly.

Let’s begin the tour:

New York Community Bank (NYCB): Everyone knows about the recapitalization, and analysts have gotten comfortable with the idea that the next two years are going to be unpleasant while the bank repositions.

NYCB is on this list however because of two new items:

a) Three different banks, not including smaller banks like FSBC, have taken out teams overseeing billions in operating account deposits from NYCB.

Perhaps this, and regulatory liquidity requirements, are why NYCB is offering 5.55% for savings accounts, an APY above the top end of the Fed Funds rate and an admission of difficult funding. If NYCB can still meet its 4Q guidance of margin around 2.4%, it would be a rabbit out of a hat.

b) Governor Hochul’s rent stabilized expansion.

New York Community has $37bn of multifamily, but the market was only really worried about the ~$10bn that was entirely rent stabilized out of $18bn that was stabilized in whole or in part.

Now some in the state house are in process with Governor Hochul on a bill to stabilize rents across the rest of NYC’s market rate apartments(!). Presumably this will drive capital out and affect NYCB’s ability to refinance out what could be an incremental $5-$10bn of market-rate multi-family that it would otherwise like to see gone to help diversify its balance sheet.

Next on our tour are REITs

Granite Point Mortgage Trust (GPMT) was profiled in the prior version of this note in the subscriber portion. Management is kind in the 10k to disclose loan marks that make the situation clear on page 44 of the 10k.

KKR Real Estate Finance (KREF): a 7x levered pure senior floating rate CRE lender, primarily in large cities.

I will spare us the alarmist discussion of mark to market insolvency. At least management thoughtfully termed out a meaningful portion of their debt, so they have some time, assuming delinquencies are manageable in the CLO portion.

Switching to loans, unfortunately 80% of the book is from 2021 and 2022 so the disclosed loan-to-values are not reliable.

KREF primarily does higher-risk bridge lending.

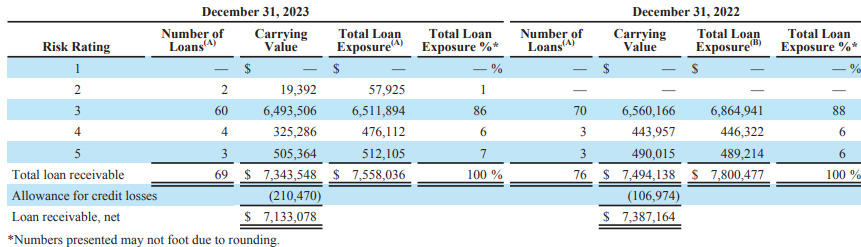

Because much of the book is multifamily, investors must go through the same “how good are the sponsors?” investigation as at Arbor, Bancorp, Merchants Bank and others. More on this in the company’s loan grading below.

The near-term challenge is from the loans rated 4 and 5 in this table. The intermediate-term challenge is the migration below 3.

Rates staying high, or in the case of the 10yr perhaps going higher, tips the scales on many 3-rated loans and that’s why KREF is included in this discussion. You can see the entire list of loans, in a book that is filled with $100mln+ credit sizes, in the 10k on pages 63 and 64 here.

Orion Office REIT (ONL) is sustaining substantial GAAP losses as it positions assets for sale to repay debt. Removal of the dividend would not be a surprise and the stub equity, currently around 25% of tangible book, would remain as a call option on inflation falling later in the year. One urgent issue outlined in the risk factors section below:

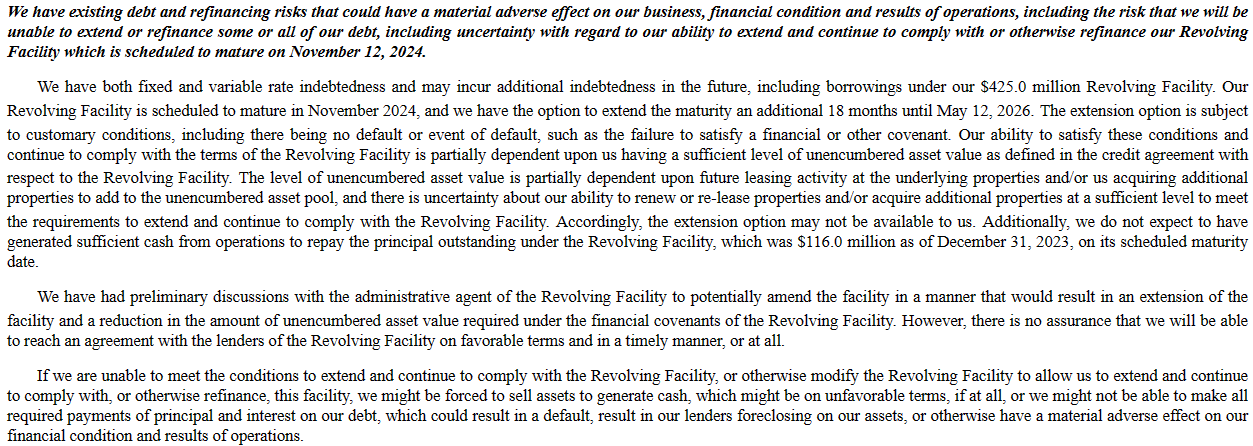

Office Properties Income Trust (OPI) is another office REIT whose 10k speaks for itself:

Moving on in our tour, we cannot ignore a bank know for loan modification prowess, Eagle Bank (EGBN):

For perspective on all of these office lenders, PNC CEO Demchak came to speak at a local function last week and was asked about the sector. He said PNC only lent on class A in major markets, at 50% LTV from initial appraisal with normal variations for location and data of origination. He said 14% charge-off was settling in as their median to mark a loan to market. That suggests that A-properties among these REITs at 60-75% ltv could have 25-40% to go upon default or maturity.

There are so many others. Sachem (SACH) referenced a hope to regain access to capital markets in its 10K. Ready Cap (RC), Blackstone Mortgage Trust (BXMT), and a list of BDCs are part of the discussion. BDCs of course tend to make levered loans on businesses but a few gathering higher nonperforming loads include FS KKR (FSK), Stellus (SCM) and New Mountain (NMFC).

Many of these funds, banks and REITs are trading at steep discounts to tangible book because the market understands that they are interest rate call options with 1-3 year lives. Perhaps the options market is the best way to participate in them.

Alternatively, some entities trading at record highs and 20-30x earnings are their GP parents, Blackstone, KKR, and Ares among others. It would be a surprise to see those companies, whose inventory across businesses and real estate is debt-funded transactions and whose real estate divisions manage hundreds of billions, continue to do so well while their LPs come up so short.

2. BaaS consent orders, and the moat from their wake

BaaS stands for “banking as a service”. As an example, if Carvana embedded a loan approval engine on its website, and a bank funded that loan product, that would be a form of banking as a service.

It can be a straightforward extension of banking in the widget economy, or a way to process payments at a fintech issuing cards. Those payments tend to get dangerous because recently there has been an “I got it, no you got it” fumbling of the process of fraud and crime prevention at many partnerships.

As a result the current state of BaaS banking looks a bit like the below.

Among the banks that have recently received regulatory orders for failing to enforce compliance, off the top of my head:

Sutton Bank (yes, since we wrote about them last edition),

Evolve Bank and Trust,

Piermont Bank,

Cross River Bank,

Lineage Bank,

Vast Bank,

Blue Ridge Bank (BRBS),

Green Dot (GDOT),

Metropolitan (MCB)

I would recommend Jason Mikula’s Fintech Business Weekly for more detail on this topic - he almost specializes in the latest regulatory consent orders for BaaS banks.

Part of the reason for this “demolition derby” is so many banks took shortcuts. A few years ago banks had a choice for how to partner in embedded banking / BaaS. They could either:

Sign on with software providers, who not only assured them of compliance but also provided fintech partners, or

Invest millions of dollars over several years building out their own infrastructure, developing the inhouse ability to detect fraud and laundering. On this path the banks have to recruit fintech partners themselves.

Almost nobody chose the second route. Some who did include Coastal (profiled below), as well as TBBK and CASH.

Who do you think the largest, most desirable widget companies now want to work with?

A good compliance infrastructure is hard to find. It has also become very valuable, with more detail on why through the Coastal example below…