March: Why Capital One is Doing This

The return potential from BANC's preferred; AI and banks

In this note:

AI and Banking

Capital One seems to have greater aspirations than it leads on

PNC targets in pictures

Mergers: Credit Unions are paying best.

The Banc of California preferred

Brief notes:

1Q bank results are shaping up to be boring, which is exciting. Bill Belichick used to scream at his players to do their job. A boring result for a bank is akin to a cornerback covering his man or an offensive tackle not giving up a sack. Many banks are instruments of levered high-yield credit, so boring wins over time.

Thank you Substack tells me over half of you open the 5 Points email vs. the platform average of around 20-25%.

Dear loan officers and debt traders: As you may know a big reason for this note is to improve Colarion’s research process. There are gaps in the market’s perception that would be helpful to better fill in. I suspect 50-100 people reading this have had a role in distressed asset purchases or sales, or loan workout at some point in the last few months. This is a sorely under-reported topic and I would appreciate the chance to compare notes. As always you can simply reply to this email if you like.

Something to look forward to - I couldn’t get to them this edition, but next time look out for: MYFW - a stressed situation leaving the Russell 2000; bank 4Q classified asset trends, Who might buy Dogwood (DSBX)? FCNCB; and First Sunflower’s purchase of Homestreet.

On to the note…

1. AI and banks:

Companies are clamoring for AI chips:

This lead me to look into how the related technology can help us.

But first, can you identify which of the three companies in the table below is AMD, which is Citi, and which is Bank of Utica? Utica is the nepotistic butt of jokes, the bank at an extreme discount to book that makes few loans and ranks among the sector’s lowest performers year after year.

You knew the answer already: the top performer is Utica and the bottom is $285bn market cap AMD. At least AMD is improving.

But moving on, let’s establish what the next 5 years will look like as influenced by AI. Some facts:

Amazon has begun scaling factory robots to do the work of humans.

AI teaches truckers how to stay in their lane, drive alert, and not speed.

As models perfect themselves, US white collar employment will be reduced by 30%+ by 2035, leading to debt and tax-funded universal basic income by politicians emboldened by Covid to further spiral taxes and deficit spending blue state-style to remain in office. This will accelerate a move by the wealthy and productive to Puerto Rico, Abu Dhabi and Singapore, leaving behind the luddites, the under-motivated, and criminals. Domestic wealth and standards of living erode, while the departing model masters revert to a global crypto-based system of exchange driven by token. The US dollar goes the way of the Argentine peso.

Oops that last paragraph must have been generated by AI trained to read a twitter feed. Perhaps only 2 of 3 above are facts, but now that I have your attention we can segue into the topic of how AI can help bank stockpickers.

A few things I think I know:

Bank shareholders are well-suited to benefit long-term from AI. If you want a deeper dive, this linked report goes into the nuts and bolts of the AI process, which is starting with fraud and data security, expanding to chats, then compliance and doc review, and onto analytics for strategic decisions.

AI fraud prevention is either already in place or will be soon across US banks. AI is absolutely necessary and is widely used today to prevent fraud, for false-check reads to payment validation. Regions really should not be losing $200mln a year to check fraud as they did recently. When I meet with smaller banks many are currently in the AI-for-fraud transition.

AI should also be help with marketing and in telling managements how to optimize resources.

AI data can help “stupid proof” a community banking strategy by giving management better clues on where to allocate budgets.

Large banks have been on this for a year or two but many small bank management teams remain lost on what products to offer which customers, where to expand (by product or geography) etc.

Consumer lenders are AI hot spots. Over time, consumer product financials like Amex, Capital One, Ally, Rocket and Mr. Cooper are increasingly AI companies.

This is for two reasons:

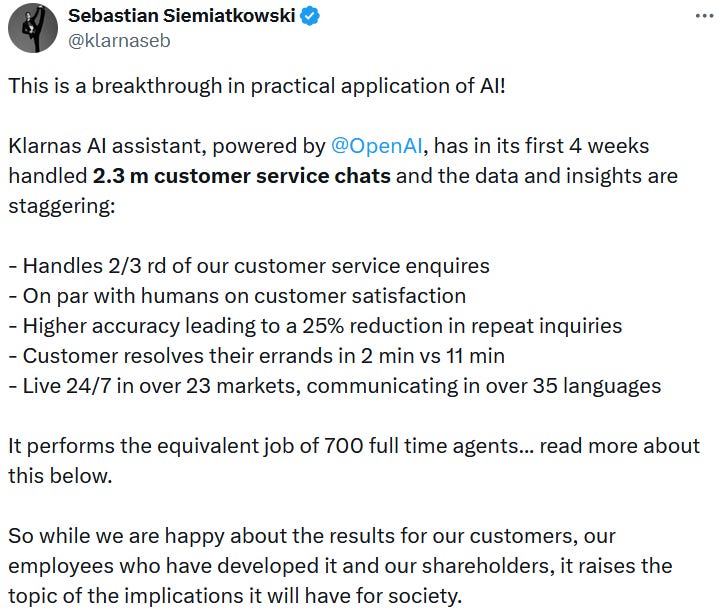

First, AI is as well suited to efficiently serving small-balance customers. The loser here is the high school graduate call center worker and the winner is sometimes the customer and most of the time the shareholder. To wit:

Mr. Siemiatkowski goes further to share that he just displaced 700 lower-level employees (and is concerned about their employment).

Second, AI should be able to better drive underwriting. How well it can do this remains to be seen but it’s really a simple expansion of already complex in-place models.

As Ivo Tjan of CommerceWest (CWBK) told me back in 2007, commercial loans are the only segment in banking that can never be commoditized. The rest will be increasingly modeled, including over time CRE.

But isn’t CRE tricky depending on location trends? Yes, and…

…Data is oxygen in an AI backdrop and data aggregators are of course already valuable but will become more so (data aggregators make up 4 of the magnificent 7). Crime, traffic, and average income block by block are a few of the relevant datapoints.

Crypto lives on because AI open-source platforms have a tendency to want to interact in tokens rather than Yellen scrip. Crypto banking was a shortseller thesis in 2023. In 2024 banking compliant crypto platforms seems to be a source of 5% overnight funds margin for JP Morgan, Bank of New York and the small number of banks who have managed to properly deal with it.

I hate to sound like a broken record but as already mentioned in the prior 5 Points, the winners tend to be the banks that lead on technology - JPM as always, plus Ally, Synchrony, Affirm, Block, Capital One, and among smaller banks perhaps CCB, AX, CUBI, OZK, LOB among others.

Part of the rationale Capital One gave for Discover was that Discover benefits from Capital One’s large technological lead. This brings us to…

2. …Capital One is not buying Discover for just a little more interchange revenue. The opportunity is larger.

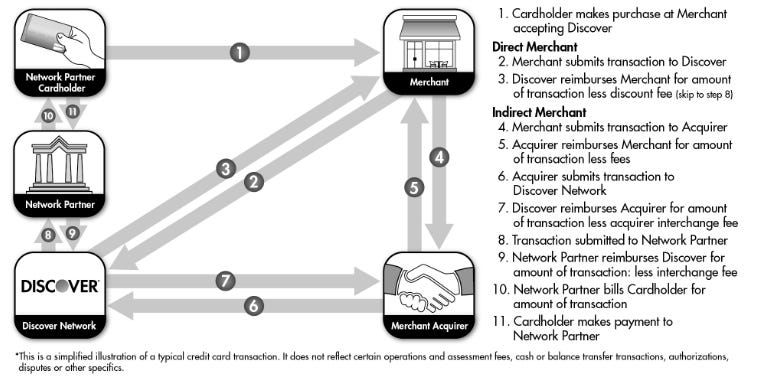

Capital One CEO Fairbank has presented some reasons for his transaction on the merger call and again this week at the KBW payments conference. I get the sense nobody knows what to make of what he is saying. Below are some numbers to help us understand the biggest issue - why is the network being emphasized?

First, some simple definitions. Look at the yellow numbers below in Discover’s income statements:

After you finish chuckling that these network items are completely overshadowed by provision for credit losses, you should know that:

“Discount and interchange revenue” is folks using Discover card at a merchant. Ideally for Discover it is processes 1-3 below (via DFS 10k):

This is helpful for Discover because they get 1.5% - 2.3% gross of each transaction, less their costs for charge-backs and many other costs. It is all described in detail here.

What Capital One can also do is take the assessment fees of around 0.15% (included in the ~2% above) it was paying to Visa and Mastercard and pocket that over time as it blitzes ads to encourage everyone to use the Discover network. It can also earn a lot more of that 1.5% - 2.3% if it chooses to, which it must.

The “Transaction Processing Revenue” line that is quite small is PULSE Network and Diners Club. PULSE is a way to rent a debit card processing system to US banks.

Why care?

You have seen this number in yellow below:

Again, we have to chuckle. $1.2bn is only about one quarter’s worth of legacy Capital One net income.

Here is where we stop laughing:

First, this is US only.

Second, Capital One is moving $175bn over, but that is a sandbagged number made to be broken because COF is currently facilitating over $600bn of payments and growing. Go inflation!

I suspect the real reason Capital One wants to do this deal is to drive what could be $3 - $4bn of incremental operating income through its network. There are puts and takes -I am extrapolating from the $600bn volume and presuming some international contribution.

In addition, Capital One can potentially incent merchants (to the degree they can) and consumers to take volume from V & MA. It’s why Fairbank talks a lot about “merchant relationships” likes the term “vertically integrated”. Visa, with a market cap of $573bn and a forward multiple of 27x earnings, is not vertically integrated.

Fairbank has to balance different factors affecting approval of his transaction, including a compliant Visa and Mastercard. It may make sense for him to forecast initially modest impacts, but enough so his shareholder still vote for the transaction.

If we model this incremental operating income at 15x earnings (Amex trades 17x) instead of the cellar 8-10x earnings that COF and DFS have been getting, then we have up to $60bn of value.

The deal announcement value is $35bn. All the rest of Discover - the loans and deposits to help COF scale like PNC wants to do, get thrown in seemingly for nothing.

Granted, this will take a long time, so it is not a table pounding recommendation to buy COF today. Also, there is much else to discuss around this deal, like regulatory approval and near-term dilution. You can feel free to respond to comment at bottom to add color or request detail.