Mid February: The Regional Bank Existential Question

NYCB's ace, Primis' gain, bank directors getting sued, is Ares worth it?

Welcome all,

In this note:

PNC wants to grow by hundreds of billions, which may create interesting acquisitions.

New York Community, Western Alliance, and the “Wal Mart vs Target” issue at regional banks. 2a. NYCB’s branding slight of hand.

Proxy season reminds us of best practices to avoid a $50mln lawsuit.

Primis Bank (FRST) stumbles on a value creation strategy that more banks should use.

ARES is up 500% in 5 years. How did this happen, what’s next, and how might we take advantage?

Brief notes:

Cheering for a bank captive: Apparently there are two primary insurers for bank boards, Travelers and ABA’s mutual insurer. Given shareholders bear the costs of the constant flood of nuisance lawsuits, and neither of these insurers has managed to dis-incent such lawsuits, why don’t banks aggregate on a captive? Captives have a tendency to fight back, to set a precedent.

You may say “who really cares” and the answer is you probably do, because you may own some $200mln market cap OTC bank that doesn’t want to join Nasdaq because post-listing insurance fees can ramp $1-2mln+ thanks to entities like the one in the picture. Or you own a bank already paying the extra premiums.

In my experience these lawyers don’t just sue because a banker misled investors. They sue because two banks want to merge and they find someone who pretends to be damaged because page 198 of the S-1 did not include a discussion of counterparty hedge risk or some other contrived nonsense. The bank bribes the firm and plaintiff for walking away and allowing an orderly merger, and shareholders pay.

A 2024 wish is for a captive to emerge.

On to the notes:

1. PNC wants to acquire regional banks to get huge, and how it matters.

They want to be too big to fail, and get there via acquisition is how I interpret the below from the 4Q call:

First, no kudos to Congress and regulators for allowing this to become a goal. When Dodd Frank handed the issue of FDIC coverage to Congress they might have done better to give the authority to the guys drinking beer in front of the corner store, who at least might have gotten a moment of clarity and common sense.

But we are here, and the timing will be ideal for PNC. First, Trump may get elected and streamline the Biden merger bottlenecks. Second, regional banks may be cheap - they are in a bind as discussed in point 3) below.

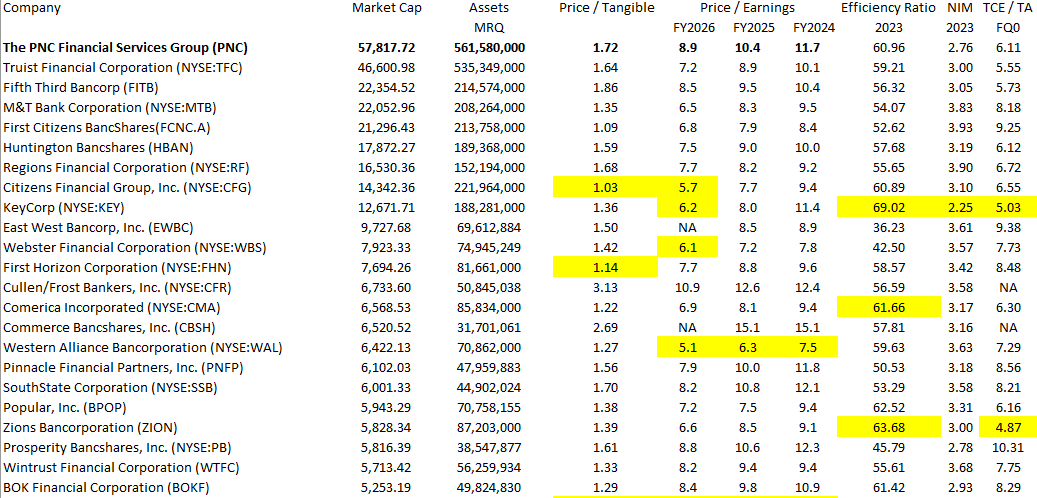

Some regional and sub-regional banks that today seem to have an unclear strategic path, are particularly cheap or temporarily wounded and may be targets include:

BankUnited (BKU) Comerica (CMA) Key (KEY)

First Horizon (FHN) TIAA Bank Zions (ZION)

Mechanics (MCHB) Citizens (CFG) NYCB (a complicated transaction)

We might also include 10-15 others. Every case is unique but the theme is regionals are caught between being small enough to fail and not providing the service that grows customers.

Below is a broader screen of the contestants, ranked by market cap below PNC.

Yellow highlights indicate issues at certain targets. For example Key and Zions are each offsides on swaps, loan yields or securities, as is Citizens.

Interestingly CFG has almost no overlap with PNC’s retail locations.

Regional bank directors understand fiduciary liability so if PNC wants to grow, with their multiple they can do business quickly.

PNC map is below: