September: The Fidelity Conversion and Other Oddities

Rick Wayne: capital management maestro; Blue Ridge (BRBS) tangible book value, Park National's itch to acquire; my Catalyst (CLST) mistake

This 5 Points is a bit unusual in that it only addresses individual stocks. Be reminded that I’m not recommending you buy or sell these, but am giving a viewpoint on how I would analyze them. Create your own viewpoint.

In this note:

The math at Blue Ridge (BRBS)

Lessons from a sour Catalyst Bancorp (CLST) experience.

Park National (PRK): Some banks “have to sell”; it seems like Park has to buy, and what that means.

Northeast Bank (NBN) is capital management maestro. A comparison with Prospect (PSEC) and Eagle (EGBN) among others.

The Fidelity conversion (FDLA): a hot deal for a cold bank

1. The math at Blue Ridge (BRBS)

A number of bank investor friends ask about Blue Ridge, a $3bn bank in central Virginia with $200mln market cap. Blue Ridge was recently recapitalized by seasoned, highly-capitalist investors after the company’s unsuccessfully attempt to bank fintech customers.

BRBS seems a likely candidate to be sold, but figuring out the numbers takes work; 5 Points is willing to roll up sleeves.

This point reviews:

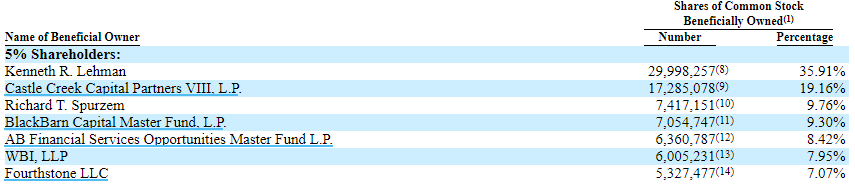

The Ken Lehman component.

Return on investment math

An M&A outlook for Virginia

The Lehman angle. “Folks do so well with Ken Lehman banks”. “Ken Lehman is really rich”.

First I would like to shamelessly point out that when I once asked Ken what he is seeing in banks he has said (joked?) “I just read 5 Points” and he readily suggests he is not a magical stock picker.

But he does have one superpower. He offers the gravitas and votes necessary to remove obstacles to mergers. The difference in owning 30-49% of a bank vs 1-2% is night and day.

We all know that banks that don’t earn their cost of capital don’t earn independence. But director prestige and greed - $30-$90k a year for networking at meetings - keeps many limping along. With a typically large position and the familiarity of a bank securities attorney, Ken is able to cut through typical obstacles to getting stuck banks sold for hearty premiums. A similar outcome with Blue Ridge in years to come is possible.

Ken does not really have to push at Blue Ridge however because the stage is already set with institutional ownership, not to mention heavy investment at the board and management level:

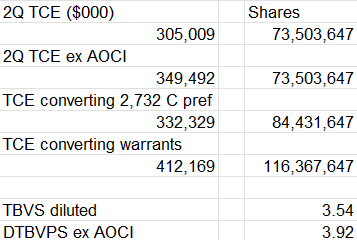

The ROI calculation

This math is preliminary because there are two sets of convertible preferred, only one of which has converted, and they come with two sets of warrants. Also the company has released a 10Q but not an earnings press release and certainly holds no conference call.

The math suggests tangible book per share is currently about $3.50 before bond marks and just under $4.00 after.

So, how much would BRBS sell for one day? As for timing, as the management of Village Bank (VBFC) was quick to point out to me, the bank is under a regulatory order that should take 18-24 months to clear. Let’s therefore make a big assumption that it takes BRBS 30 more months to both build enough franchise value and appease regulators that they can get an interested party to make an offer at 1x tangible book.

Earnings between then and now may be negligible - say $0.15. Partial AOCI recapture may take tangible book with earnings to the range of $4.00.

If you want a 15% return for a $4.00 payout in 3 years you would pay about $2.47 today. If it only takes two years then you would pay $2.75, but that would be a fast turn.

Could BRBS get over book value? This note is about to study Park National, which trades at 2.8x and may be interested in retail franchises like what BRBS manages.

An M&A outlook for Virginia

We have spoken about Ken Lehman. Who is E.J. Face, Jr. aka Joe Face? He is the Virginia Commissioner of Financial Institutions…since 1997. Before that he was an examiner since 1979. In a power move he attended the University of Alabama and in another power move he has not approved a single credit union purchase of a bank in Virginia.

It’s not so bad; Blue Ridge is a bit large for credit unions anyway and there are other contestants.

If there were a Tinder app for Virginia banks it would have on one side the proven buyers: Park National (PRK), City Holdings (CHCO), Peoples (PEBO), Atlantic Union (AUB) and United (UBSI).

The other side would be potential sellers: Blue Ridge, First Virginia (FVCB), Freedom (FDVA), Main Street (MNSB), Village (VBFC), First National (FXNC), perhaps Primis (FRST), and John Marshall (JMSB).

The complicating factor keeping these banks, most of which don’t earn consistent 12%+ ROEs, from consolidating is thought to be aggressive asks combined with a litany of issues including bond marks, credit blips, and execution issues.

There is no aggressive ask at Blue Ridge and the company is being designed to be a simple as possible. Perhaps it will be among the first of these to swipe in favor of a buyer.

Anything else?

BRBS is now a likely Russell index candidate, for readers who like a trade.

2) The Catalyst Bank (CLST) lesson I had to re-learn:

Watch what they do

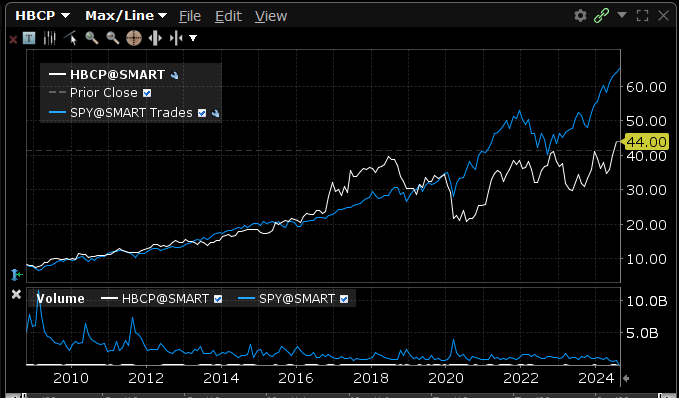

This is Home Bancorp (HBCP), also known as “Hubcap”, a $3bn Louisiana bank that converted from a mutual thrift in 2009.

HBCP shares rose from $10 to $40 from 2009 to 2017, at one point gapping the S&P bull run despite an ultra-conservative Louisiana thrift balance sheet. This was because HBCP management aggressively repurchased shares, and when they were not repurchasing, they were acquiring banks at low multiples. Louisiana banks have the benefit of being in low demand, so often could be bought for below book value (some were FDIC deals).

The man doing the repurchasing was HBCP CFO Joe Zanco. Zanco got to play Kirby Smart to CEO John Bordelon’s Nick Saban as Hubcap ran a 15% IRR for 8 years.

A quick story - the defensive coordinator who came after Kirby Smart at Alabama was named Jeremy Pruitt. He was arguably a better defensive coordinator than Smart, and was hired by Tennessee. Yet while Smart has won championships at Georgia, Pruitt lost games and was fired around the same time as it was discovered he was not just losing but also handing out bags of money to recruits.

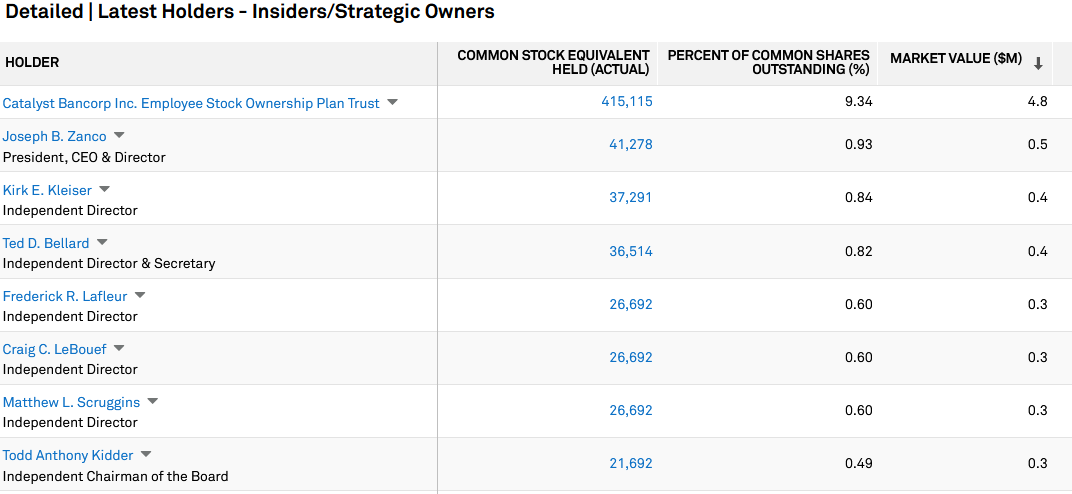

Back to Zanco, he too left his employer to get his own head job as CEO of $200mln Catalyst Bancorp (CLST). I liked what Joe did at HBCP and figured he would do likewise at CLST the playbook was simple and who doesn’t like high returns?

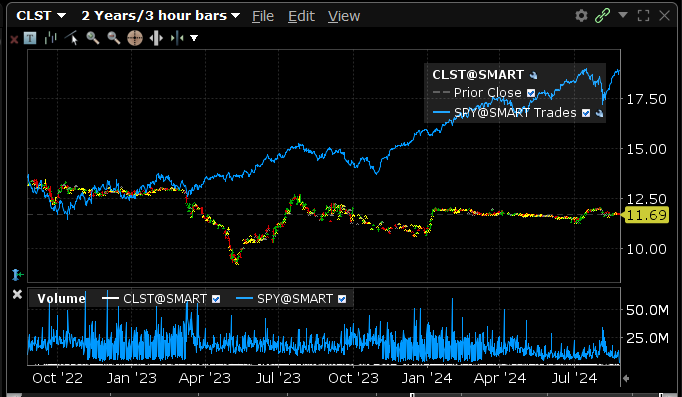

The first few seasons are in the books and the record more closely resembles Pruitt than Smart. CLST has underperformed the S&P by about 60%. What happened?

Continuing the football analogy, what if the goal isn’t to win, but to sustain? To please boosters, or break even financially.

At Catalyst my conversations with management always suggest that repurchases were a priority. However I came to understand that while the company did repurchase, it was not a top priority. As the rest of the market came to understand this, it created a unloved stock.

Trading at 65% of book with 25% capital you might expect 10% authorizations but instead CLST has been slowly implementing a 5% program.

The company could in theory retire 100% of the shares outstanding at current prices and still have 10% capital against $300mln assets. To use a different sports analogy I look at this like sitting in the batters box and watching 75mph fastballs sail down the middle for strikes.

My best guess as to why this is happening is the board wants CLST to sustain for a decade or longer.

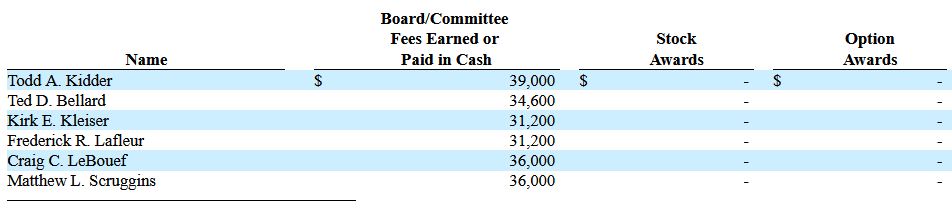

Consider that board compensation relative to ownership runs in the 1:1 range for most directors.

In this backdrop a director has incentive to perpetuate the organization rather than fully lever the capital, potentially ending up sub-scale, vulnerable to take over.

If the question is whether Catalyst is run for maximizing shareholder value or for sustaining board fees, that is certainly an awkward question in this backdrop.

One day the priorities may change, and CLST shares will become very interesting. I would watch insider activity as the tell.