October: Why does Esquire print money? Why can't Ponce do the same?

The new FDIC merger policy and best practices for banks to evolve alongside, the Northern Virginia banks, credit union acquirers in New York, the bad loan marketplace

Good morning,

In this note:

The recent regulatory update for bank mergers, and how it affects both bank and credit union acquirers. I also suggest some bank best practices among recent tighter regulation, on behalf of appreciative shareholders.

How Esquire Bank (ESQ) prints money, and a few others that are learning.

Ponce Bank (PDLB) has some tempting catalysts. Why don’t profits drop to the bottom line?

Cleaning up the North Virginia bank market - A number of Northern Virginia banks are not “earning their independence.” The realities, with a quick look at EGBN, MNSB among others.

Credit Unions are buying banks in New York! This is a meaningful change, encouraging some underperforming New York banks to justify independence amid potentially high premiums.

A few brief anecdotes first:

Mystery unveiled - You may wonder whether the thoughts coming out of this letter lead to performance. Colarion’s performance and portfolio characteristics are now available to accrediteds on our website at top right. This disclosure covers our pooled vehicle - The Mint Fund. Colarion also manages separate accounts, each with unique performance and risk profile.

A timely donation Given the situation in the Carolina mountains, it’s an easy decision to send this quarter’s gift to Samaritan’s Purse, a faith-based international disaster relief fund located in Boone, NC.

Banking is evolving in one important and underappreciated way

I’m writing this after being added to an email list marketing nonperforming loans.

Funds and banks are working together more closely than before and I’m not sure many bank investors understand this.

Specifically, in 2008 there was no deep pool of liquidity to buy bad loans. If a bank had 100 foreclosed lots outside of Atlanta, it sat on those lots sometimes for several years hoping for another developer or someone to raise money and buy at 30-40 cents on the dollar. Signature Bank (SGBG) of Atlanta still held several of these loans into 2018!

Today it appears there are tens if not hundreds of billions looking for non-performing bank loans, as part of the distressed debt market fundraising between $10-$40bn a given year recently.

Moreover, these funds act in waves - one fund closes and another goes into marketing, so there is a potential for dry powder to soften the credit blow from a recession. If we do have a recession, do you think Blackstone’s marketing would go into software, chips, infrastructure or distressed? I suspect distressed would see significant interest.

It may surprise you how deep this market is - there are well over $100bn in bad loans to transact in (thanks shadow banks!):

It would be foolish to say “never again” to a 2008 style credit event but the market structure is significantly more supportive for bank credit resolution because of this evolution.

A preview of next edition - the republican bank and the democrat bank The note will profile Amalgamated Bank (AMAL) vs Chain Bridge Bank (CBNA), in process of IPO. The first handles deposits for liberal causes, and the other for conservative causes. Fortunately for investors they both seem to win - politics are a distraction from pushing for the highest deposit rate.

On to the 5 Points:

1) What does the recent FDIC policy update on mergers mean? What can banks do to get around value subtracting regulation?

There is a new FDIC September 2024 Policy Statement on Mergers, with a number of changes that readers should be mindful of, including:

FDIC will look at how mergers “affect communities”, which seems to suggest that material branch closures and cost saves will be frowned on more than in past. Banks like Prosperity (PB) had a good run cleaning up inefficient banks all over Texas - it would be a shame to end that.

Deals resulting in a bank over $50bn now require congressional hearings. You’d expect Congress would have more pressing work, but the FDIC wants this.

A nod to taking a closer look at the credit unions that are buying banks. This appears to be more bark than bite,

This point expands on the politicization of FDIC regulation reviewed in the prior 5 Points discussing the Chevron ruling. Specifically there are other ways banks can shield themselves from regulatory (d)evolution like this latest policy change. Let’s look at:

Getting around delayed mergers

Board restrictions

Reducing taxes

Using the holding company for lending programs

Whether credit unions can still buy banks.

a) Speeding up delayed / costly mergers.

It used to take 6 months to get a bank merger closed, now typically a year. What happened?

It seems that community activists are sending the FDIC more letters complaining of a bank’s lending practices. The FDIC apparently used to address this issue in an efficient manner but now uses the letters as a lever.

This issue / problem / grift was addressed in the policy statement:

“Frivolous letters are not included”. Truly?

Shareholders pay for all this and much of it needs to stop. One possibility is acquisitive banks can apply for the Federal Reserve to become their primary regulator. The Federal Reserve has not updated its merger guidance in the way the FDIC has and due to its board makeup is possibly more balanced than the FDIC, primarily with Mike Bowman quite vocal on these topics at the moment.

The OCC is a another possibility, but the OCC sometimes reminds me of Judge Smails in Caddyshack: “I’ve sentenced boys younger than you to the gas chamber Danny. Didn’t want to do it. Felt I owed it to them.”

But the strongest weapon is Chevron. From my discussion with a merger attorney, community activists are a bit like accident attorneys in that they don’t actually want to go to court. Filing a lawsuit may counterintuitively speed things up.

b) Board meddling / taxes

I recently spoke with a west coast bank executive about regulatory input on his board. His bank is also paying an elevated income tax.

What’s wrong with Nevada? In addition to board or other political constraints, Oregon charges 7% state tax on banks. California and New York charge 8% and 7%, respectively vs 0% in Nevada. Ohio and Texas also charge no corporate tax.

Axos (AX) and Plumas (PLBC) have recently made the move to Nevada. This is a much bigger discussion but I certainly don’t see any banks regretting their decision to move.

c) Lending outside the bank charter. We touched on this with regard to Newtek (NEWT) in a prior note.

The risk adjusted margins can be far superior for loans that don’t fit the regulatory box.

Bank holdcos may benefit by establishing a separate asset management sub using outside capital, or a levering an internally capitalized entity. This allows more “private credit” style lending. If you agree as I do that regulators are often value subtracting, this line of business can make sense.

d) Sell to a credit union (!). For WA, NY, GA, FL, IL banks.

I won’t expand on this because I write about it almost every edition. However in the context of this first point we should look at the discussion of credit unions buying banks in the FDIC policy statement. Bloomberg wrote a scary article about it. However the guidance is actually not particularly alarming; I don’t believe it changes anything assuming the FDIC is timely in its review of the CU:

The best banks will evolve in tandem with the FDIC.

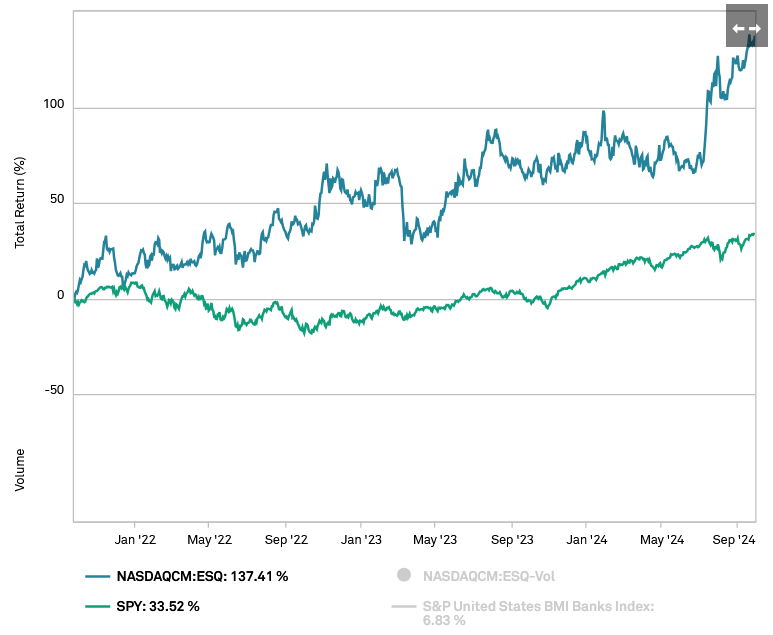

2) How Esquire Bank (ESQ) prints money, and a few others who are learning from it.

Esquire Bank is the archetype of the kind of “flywheel bank” Colarion focuses on - a highly profitable, specialized bank that has found a blip in the competitive landscape and levered its advantage.

I have discussed ESQ previously after they announced no client defection post Silicon Valley. The story is worth revisiting with changing interest rates.

To that end I visited with ESQ CEO Sagliocca last month. After the usual 10 minutes of contentious questioning around the NYC apartment portfolio (a topic for another note), we discussed Esquire’s unusual rate positioning.

Esquire is a bank that does very well when rates rise, because it pays nothing on most of its deposits, and gets roughly prime + 1 on its portfolio of law firm loans. But falling rates should impact profits. Another analyst asked: “How much would a down 150bp+ interest rate scenario affect Esquire?”.

Sagliocca offered imprecise guidance: “We’re still going to earn money like a mother-——-.”

Sagliocca is confident because Esquire focuses on one of the most profitable banking verticals, and importantly offers a service that a number of other banks don’t compete on because they don’t understand how to. Fortunately, his vertical has capacity to expand for many years.

Specifically:

a) 90% of loans have floors. In other words, if rates fall, a 7.5% loan may stop falling at say, 6% because the loan agreement mandates it. The customer might not like it, but again, a limited number of banks offer the service in the first place so what can the customer do?

b) Esquire can grow its core lawyer business, in the process diluting down its lower margin CRE / multifamily loans. This was Sagliocca’s primary point - Esquire is growing its high margin business by double digits a year due to outreach efforts and the relatively immature marketplace for loans against case inventory. Many of the firms his bank calls on don’t even understand that they can borrow.

c) The core business is excellent. Notice the loan / collateral at 13% vs other degen banks like Valley (VLY) hoping they get repaid on CRE at 60-75% entry loan to initial appraisal.

d) Deposits The core lawyer banking deposit base is among the best in banking, as shown by this piece chart. NOW accounts pay about 0.1% in New York.

e) Moat As mentioned, lending to attorneys is slightly unusual because there is typically no real estate collateral and the inventory is cases in progress. Given banks stopped training lenders long ago, most banks simply say “we don’t have that expertise”.

The moral of the story - high rates or low rates, if you are a banker who isn’t banking lawyers, you should consider building your expertise.

Other smaller banks that understand the potential of this business include USCB, PBAM and AMBZ.