October: How far do Sofi, Affirm, Dave etc. have to run? Eagle Bank upside math.

Recent Fintech IPOs are governance problems, Ciaran McMullen makes money for owners. Why go for 20% annualized discounts on credit union acquisitions? Sound Financial (SFBC)

Hello everyone,

Inside this note

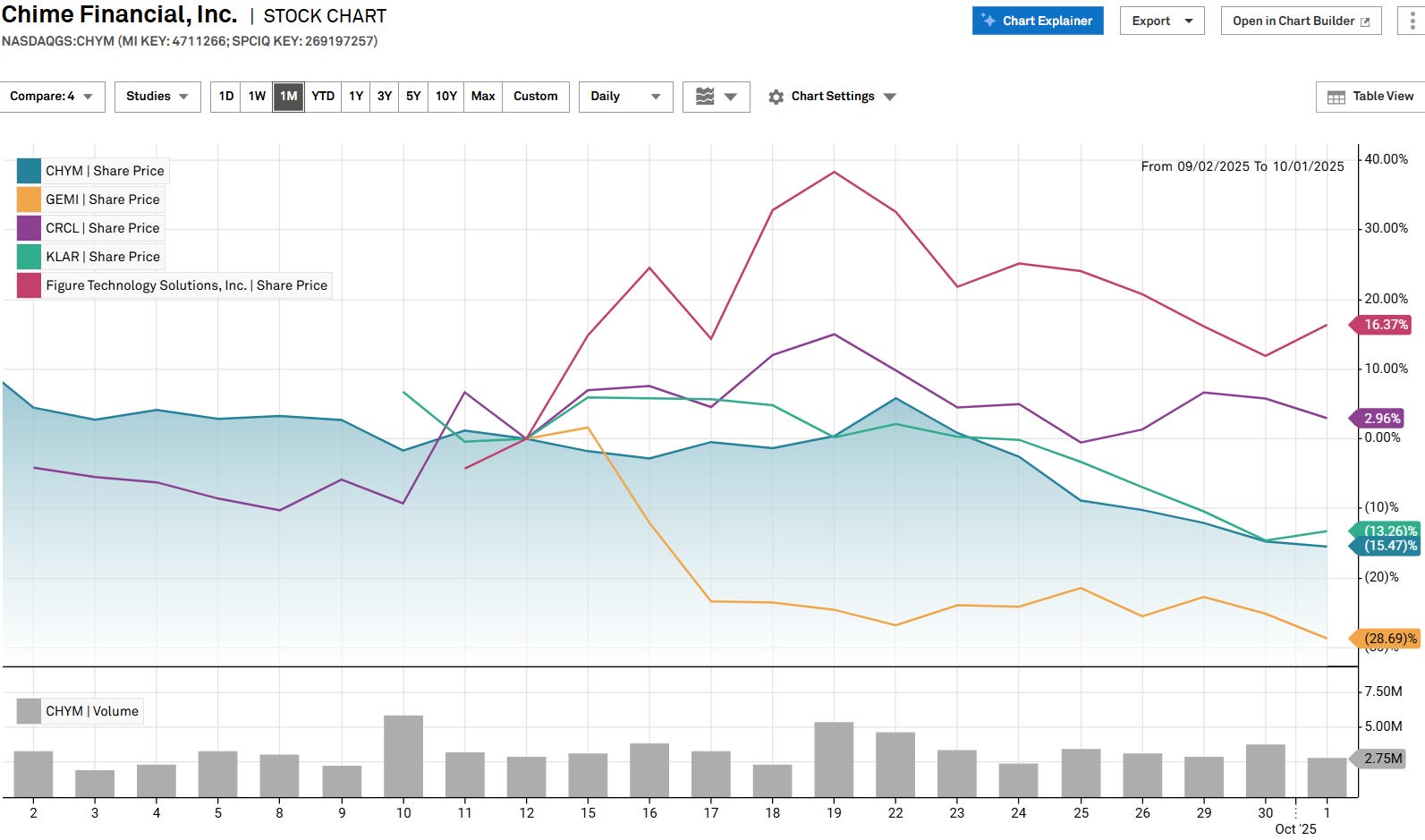

A check of corporate governance at the latest fintech IPOs leaves me wanting to take a shower. Should we care? Post-IPO (under)performance suggests maybe so. (GEMI, FIGR, KLAR, CHYM, CRCL)

How far do the consumer fintech lenders have to run? A look at the foundation of the rally. (AFRM, DAVE, SOFI, KLAR, UPST)

“Tough investing” - the simple math to 50% upside at Eagle (EGBN) for those ready for what’s coming.

You should know about Ciaran McMullen at Bank34 (BCTF).

Banks selling to credit unions can see deep discounts to announced deal value. These discounts may be too high in some cases. (PMHG).

Thanks to subscribers we are giving away $6k to Christopher Kids, which is an unusual cause that customizes living spaces for disabled children. I’m always looking for children’s charities. The ideal is to find a small version of St. Judes that banks with a community bank. All the nonprofits around here bank with Servisfirst or Regions. Next quarter’s gift will likely go to Smile-A-Mile barring a good suggestion from a subscriber.

Next month we will look at some large recent failures (such as Tricolor and First Brands) and see how the credit cycle affects banks differently than in years past.

Brief notes:

In a few weeks, Coastal Financial (CCB) will do their first quarterly conference call. No longer will it be a mystery how the “pick and shovel” behind Robinhood, Dave and Walmart et al operates.

M&A Q&A

Q. Turning to another Seattle bank, Why hasn’t Sound (SFBC) sold yet? A year ago 5 Points suggested Sound may be a seller, given the board allowed an activist to join without any contention, and the bank is located in a credit-union friendly state.

A. I have not heard of an investment banker Sound may have representing them, but I have heard rumors of boneheaded mistakes, plus the state of Washington recently enacted a credit union acquisition tax. Selling a bank properly requires skill, luck and timing. Global CU recently closed its deal with FFNW and I suspect they could use more presence in Seattle. Perhaps Sound can find the proper path in the months ahead?

Bayfirst (BAFN) sold a chunk of loans after all! What next?

Last month 5 Points wrote that Bayfirst had a tricky process placing $123 million of questionable quality SBA loans with a buyer. Kudos to Bayfirst for finding Bradesco to swallow $103 million of the $123 million close to par, with the rest presumably taking a substantial hit. I am told also that some of the $103 million was guaranteed. A welcome evolution given board halt to preferred dividends plus the potential for heavy losses.

The fulcrum was loan buyer Banesco gets 1% servicing on the entire original loan balance. Given BAFN sold about 85% of the guaranteed portion of these loans, that’s 1% a year on about $800 million of loans.

As a result, Banesco paid 97% for performing loans, and the servicing strip kicked in what could have been an extra 20% of value on the package. Banesco’s need for yield plus the servicing value is the upside surprise.

What now? Before we celebrate too much we have a few obstacles still to clear:

a. Bayfirst must still charge off or sell at least $20 million more of product. Can they get through without a capital raise?

b. BAFN will be on hook for recourse for reps and warranties on the nearly billion worth of high yield loans.

c. BAFN is now an inefficient, 3.3% cost of funds bank that will need overhaul, but management is the same.

d. Will management overhaul, or sell? Management is telling some folks that they now intend to build the best community bank in the Tampa Bay area. If the starting point is around a 2% net interest margin and 90% efficiency ratio, the Bayfirst may be as the least best bank in the area, so there’s much to be done. We may be back to waiting for fiduciary action, just without the massive profits from the Bolt program.

This was a golden opportunity for a BRBS-style cleanup and sell situation. It’s still a matter of time until this underperforming bank gets a large premium, but we need to keep a finger on the pulse to see if that means one year or five. Given capital levels, this could be an odd situation where a bank’s regulator ultimately pushes a big win for shareholders.

on to the notes:

1) The recent fintech IPOs aren’t good enough businesses to get away with their corporate governance games

We have heard of “catching a falling knife”, but what about “catching a set of ginzus”? That what we get from the recent set of fintech IPOs:

Part of the issue is these businesses are not good enough to get away with their corporate governance schemes, much less their valuations.

It begins with use of A and B shares. Years ago Google, Facebook and others created structures where insiders voted a supermajority and IPO buyers got little or no vote. They could do this because the issues were hot and their businesses were industry leaders.

Executives argued that they kept skin in the game through ownership, so presumably they would not turn into Solera Bank majority owner Quagliano and a) buy a fleet of jets b) put daughter on the board c) reprice options d) push out the CEO and put yourself in charge e) fill the loan book with participations f) pay yourself a chunky percent of income and g) use the jets to fly from Florida to Denver to watch basketball.

Back to Facebook, Zuckerberg has famously vaporized billions on projects such as the Metaverse and is now at work spending $50bn+ hoping to advance AI to the point of being able to fire many more employees. It doesn’t matter when you amortize the cost and dominate online advertising. But what if your business is not exceptional?

That is these IPOs. But they act like they are Facebook.

Of the businesses we will look at, Circle is an lightly capitalized quasi-bank, Gemini a subscale broker, Klarna a competitive marketplace lender, Chime is living off thin debit-interchange, and only Figure has scalable, higher-margin potential.

Let’s dig into the disconnects:

Klarna (KLAR) sold $1.3bn in shares on Sept 11: I assign Klarna a grade of D for voting rights and B for executive comp.

Klarna competes with Affirm and Paypal among others in the increasingly commoditized BNPL sector.

Klarna 2Q EPS release Votes: Legacy holders own B shares with 10 votes. IPO buyers get 1-vote A shares. CEO Siemiatkowski gets special 10 vote C shares.

Comp: Klarna’s compensation program is unexceptional except that the CEO receives over $20 million in compensation, mostly stock, which is not offensive for a Sequoia-backed, ~$16bln market cap company.

Should Klarna get away with the super-voting shares and tens of millions in comp?

After not growing revenue in 2024, Klarna’s US expansion and large corporate partnerships have grown revenue from $442mln in 4Q24 to $604mln in 2Q25.

Yet Klarna’s EBITDA and net income have fluctuated wildly and the company lost money in 1Q and 2Q, leading to questions about operating leverage.

Regardless, KLAR is 40x 2026 “adjusted EPS” consensus which for an unsecured consumer lender making layaway loans is questionable value. Combined with the corporate governance, there is no temptation to follow Sequoia into shares.

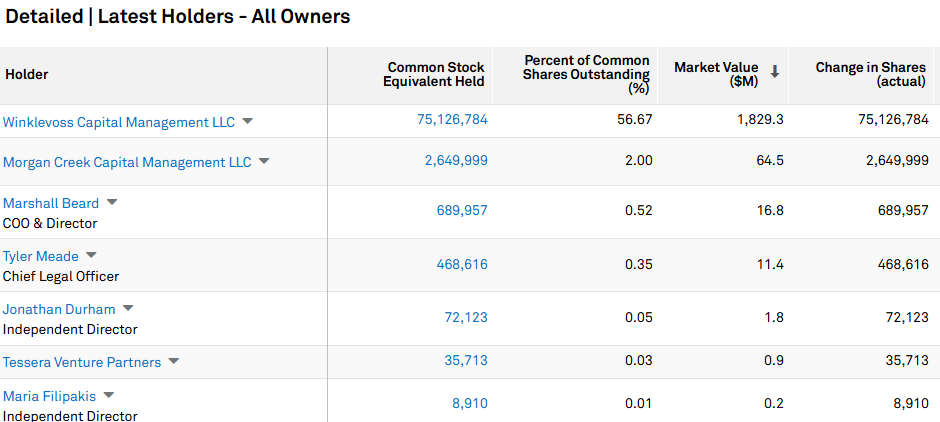

Gemini Space Station (GEMI): $446mln IPO on Sept 11

Vote: As at Klarna, Gemini’s new shareholders will have effectively no say:

Comp: On executive compensation, the company has set aside about 23% of shares outstanding for employee restricted stock grants and options, which is not ideal, nor is the fact that the business is not solvent per se until salary stops taking almost all the company’s revenue:

Strangely Gemini shares the wealth because despite the massive comp line, the S1 discloses modest cash comp to executives in 2024. Perhaps this is because the twins own so much stock they have incentive to show good results?

Has Gemini earned the right to push this compensation and and skewed voting scheme? Crypto exchanges might be good businesses if run efficiently, but Gemini seems subscale in its current state. Revenue is flat both sequentially and annualized and EBITDA is pinned at negative $50mln a quarter. Gemini has a $3.2bn market cap.

GEMI gets a D for shareholder vote and a D for compensation because comp needs to come down materially (or revenue increase materially - it is flat the past four quarters) for the business to sustain itself.

GEMI shares are the worst performing of our group since trading opened.

Figure (FIGR): $787mln IPO on Sept 10 Figure has real potential among this otherwise questionable group and as such has earned more leeway in its governance practices.

Figure S1

Vote: Once again management gets 10 votes and enablers get one.

Comp is not so out of line as elsewhere, at least not so far this year. To Figure’s credit, the company generates enough from fee streams, primarily gains on sale of loans, to generate a profit so far in 2025. Last year they did not make a profit, because they paid the CEO $37 million and two other officers $5 million each, mostly in shares.

Most of these IPOs are single business lines that grew into a company. Whether they add value is open to interpretation. Figure actually works on interesting things, solves problems, and can scale its solution - streamlined real world financial transactions using blockchain and its own token. Others may be able to do the same in the future, but Figure is first.

About $8bn market cap for less than $500mln revenue run rate assumes Figure’s progress accelerates more rapidly than it likely will. Still, Figure is the only one of these fintech IPOs where I would have an interest at a lower price.

5 Points assigns Figure the customary D for voting and C for compensation.

Circle (CRCL): $1.3bn IPO on Aug 14

Vote: Founders get five votes per share, outsiders get one.

Comp: The board is not stingy with stock for executives:

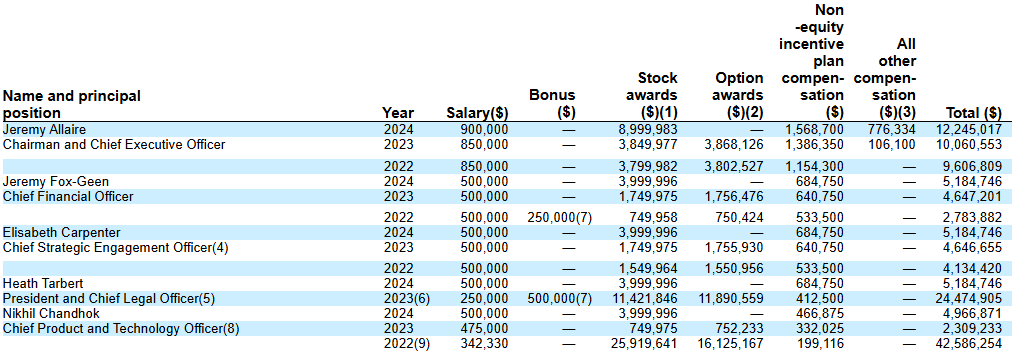

For 2024 Annual Grants, grants made to the NEOs were as follows: (i) Mr. Allaire, $9,000,000, (ii) Mr. Fox-Geen, $4,000,000, (iii) Ms. Carpenter, $4,000,000, (iv) Mr. Tarbert, $4,000,000, and (v) Mr. Chandhok, $4,000,000.

For 2025 Annual Grants, grants made to our 2025 NEOs (Messrs. Allaire, Fox-Geen, Tarbert, and Chandhok) were as follows: (i) Mr. Allaire, $9,000,000, (ii) Mr. Fox-Geen, $6,000,000, (iii) Mr. Tarbert, $7,500,000, and (iv) Mr. Chandhok, $6,000,000. For Mr. Tarbert, $1,500,000 represents a one-time promotional grant.

4 officers also each got $1 million cash for doing the IPO. Circle seems like a good place to work as an executive.

Circle is a “decent” business during periods of high rates. It could be a “good” business but the company splits economics with its distribution partners. Revenue is running around a $2.5bn run rate with 10% net margins; there is not a barrier to launching a stablecoin today as there was when Circle was ramping within a legal grey zone. Yours for $30bn market cap.

We have seen more piggish comp arrangements elsewhere. Circle gets a C for votes and a C+ for compensation.

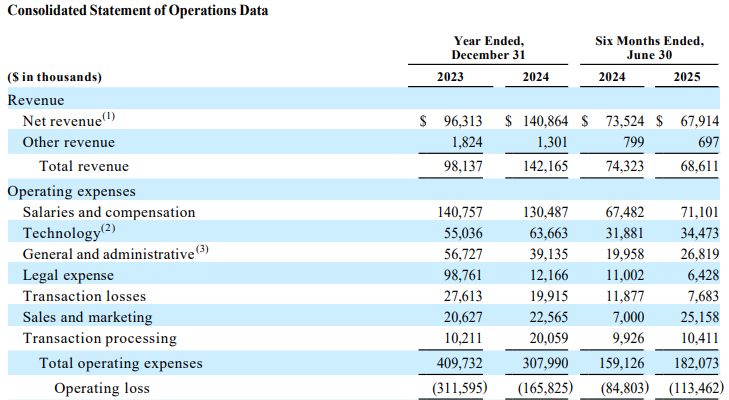

Chime (CHYM): $993mln IPO on June 11

Vote: 20 votes / share for insiders. I wonder why stop at 20? This is worst in class, F.

Comp: The two founders took $15mln each in 2024 and other executives got closer to $1mln. Unusually lean. Co-founders get large stock grants if shares rise 1x, 2x, 3x etc., generating incentive to pump shares in the style of Tesla.

Chime grows; revenue rose from $1bn in 2022 to $1.7bn in 2024. However in 2Q revenue grew sequentially from $518 million to only $528 million. The company effectively spends on marketing to bring in interchange revenue, which is not a spectacular business (banking Chime is a good business, as TBBK share price indicates), and Chime is now breakeven in 2Q2025 in part due to IPO cash interest.

Breakeven, except for $928 million of stock compensation expense!

All yours for a $9bn market cap. F / C-

Summing all this up, most of these fintech IPOs are not particularly good businesses. They smartly used a open window to fund future operating losses or 9 figure executive comp annuities. The market seem to be rethinking valuation and, I would like to think, governance, so readers may feel free to allocate to companies that care more about accountability.

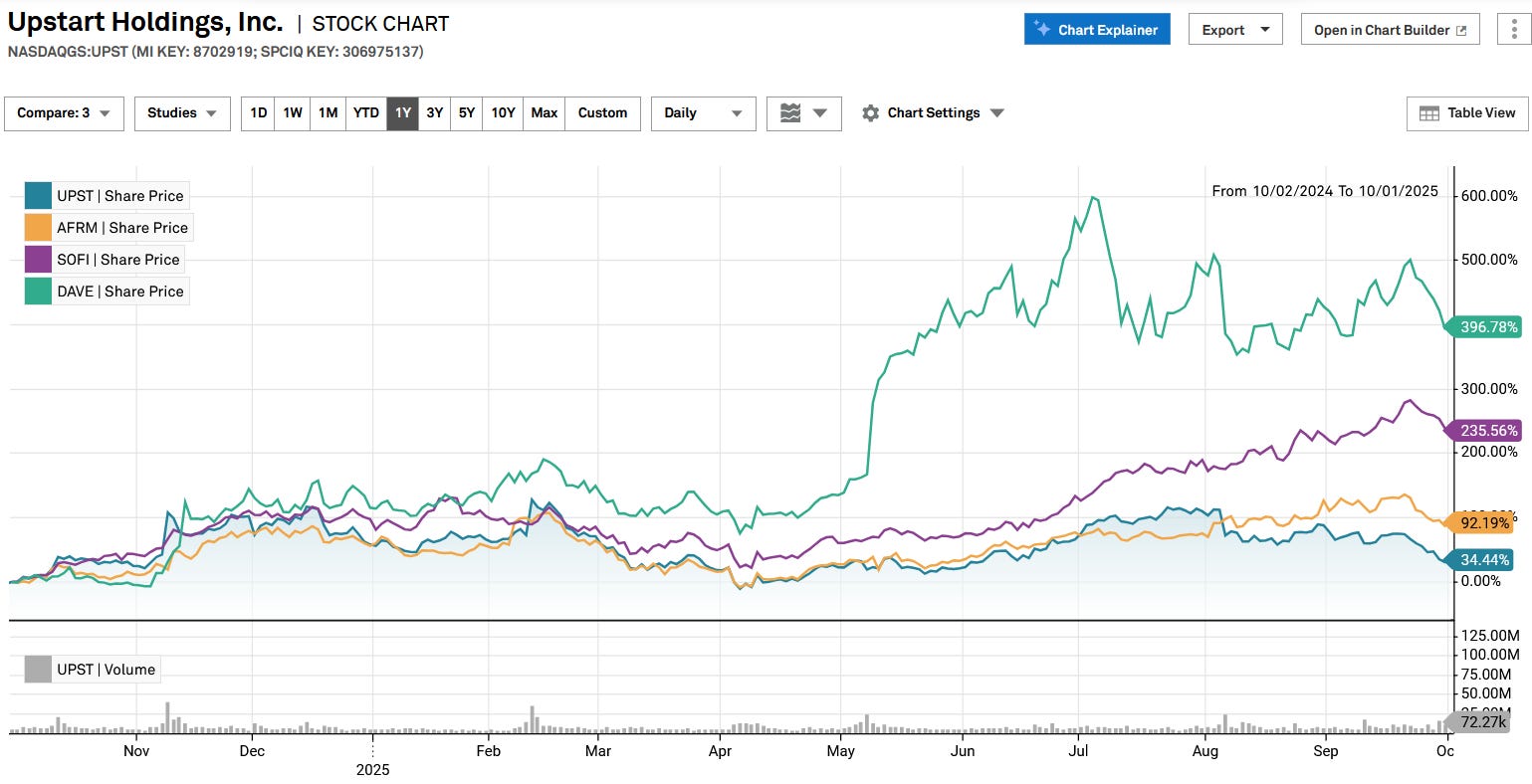

2) How far do the consumer lenders - Affirm (AFRM), Sofi (SOFI), Upstart (UPST), Dave (DAVE), have to run?

This note presents two theses:

a) Unsecured lenders are doing very well because of a precarious set of circumstances that are showing signs of change.

b) This change doesn’t necessarily end with a bang, to quote T.S. Eliot, but more likely a whimper.

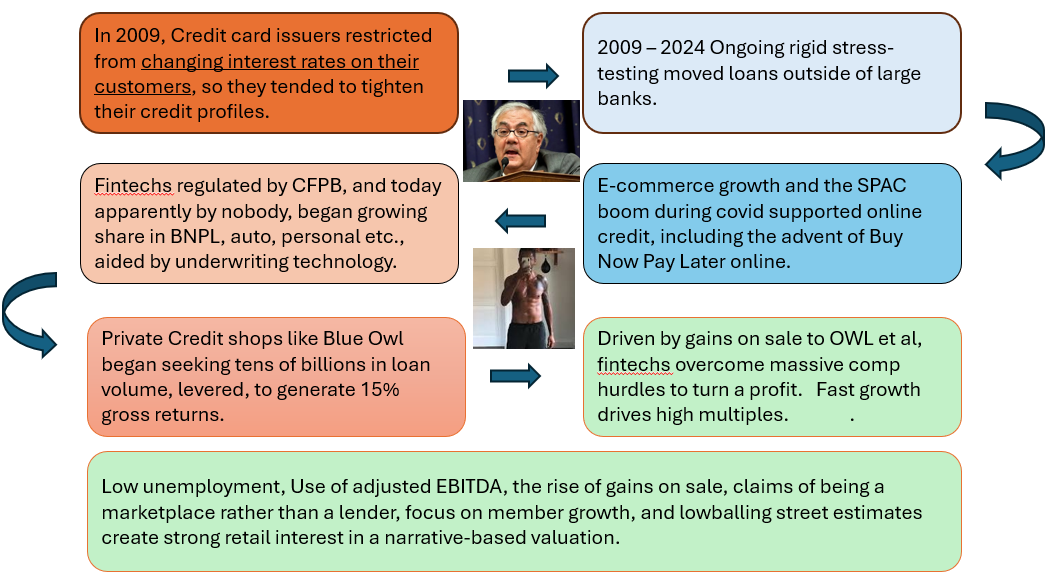

A long time ago, some small changes made a big difference. How credit card lenders could underwrite began rolling a ball downhill that today has resulted in about $100bn of loans running through fintechs. The same loans that credit card lenders valued at 10x EPS made are now being made by fintechs valued at 30x:

The history:

Eh voila:

Why is unsecured credit hot but vulnerable?

a) The ideal conditions that supporting its growth are flagging.

These include covid stimulus, low unemployment, and hopefully more loopholes to avoid student loan repayment. Most importantly, it requires private credit capital injections and the belief that credit will stay benign.

b) Like mortgages in 2007, constantly pumping loans into the system creates its own cycle.

Let’s begin with point b) above. The market thinks that eye popping origination growth of a commodity loan product is bullish. True, $10bn here and there is not going to break a $5trn market but fast growth in consumer loans has always been and will always be painfully self-correcting in the long run.

UPST:

SOFI:

AFRM:

These lenders tend to sell off much of their origination volume. Let’s look then at point a) above - conditions are good for loan buyers. Will that remain the case?

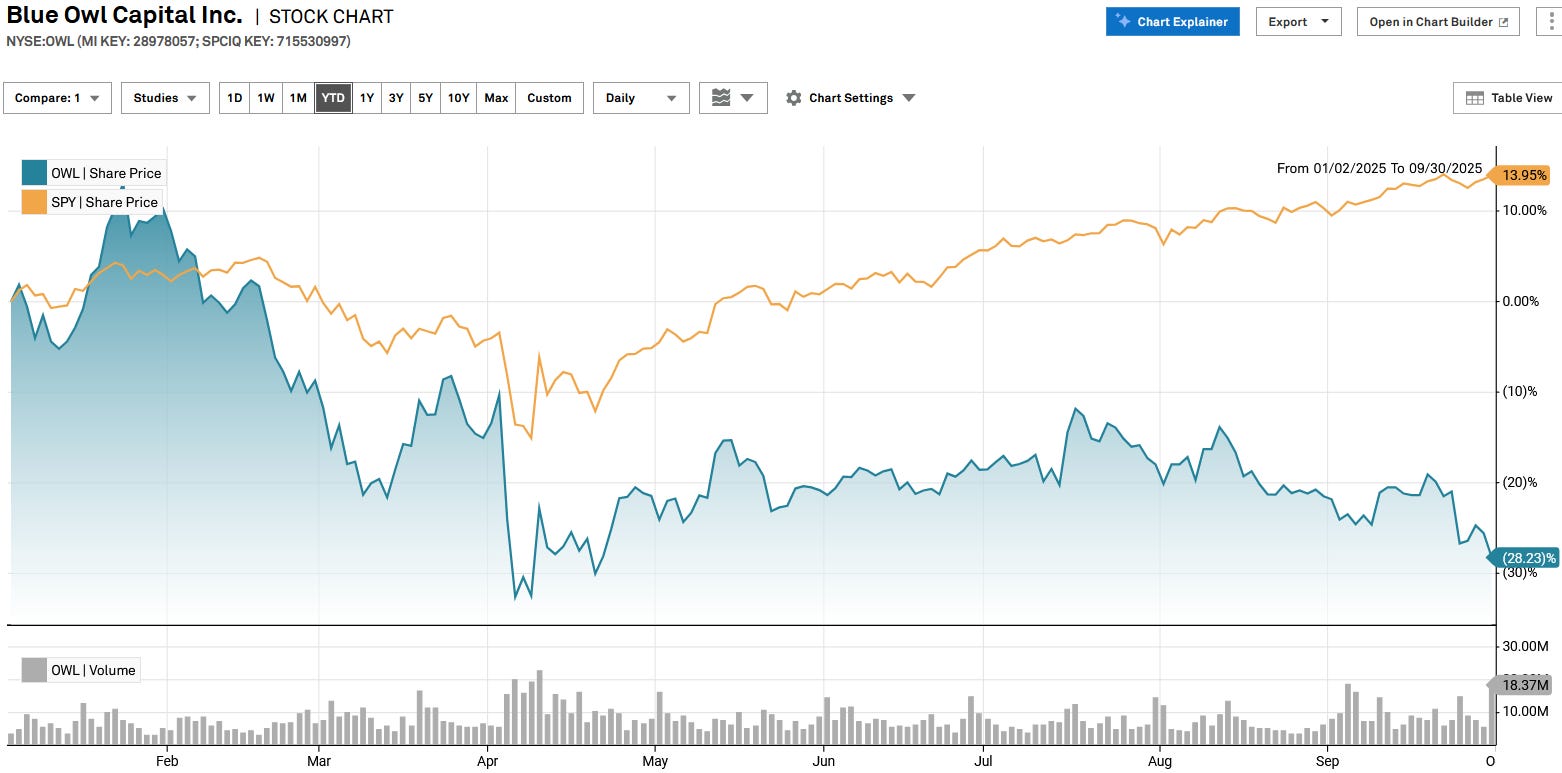

The leading indicator (the stock price) of the leading indicator (the largest unsecured loan buyer) suggests maybe no. Why are Blue Owl shares off 28% this year?

An ad hoc online essay on this divergence, with some interesting points about the lags in private credit is here.

Of course only a small portion of OWL assets are sourced through flow deals with SOFI and Paypal and Upstart and Lending Club.

Much of the market’s concern is instead with their steady growth in restructured payment-in-kind loans, and their methodology for marking loans. Specifically, a number of 2021 and 2022 loans are rotting on private credit books to drive “bad PIK” numbers increasingly higher.

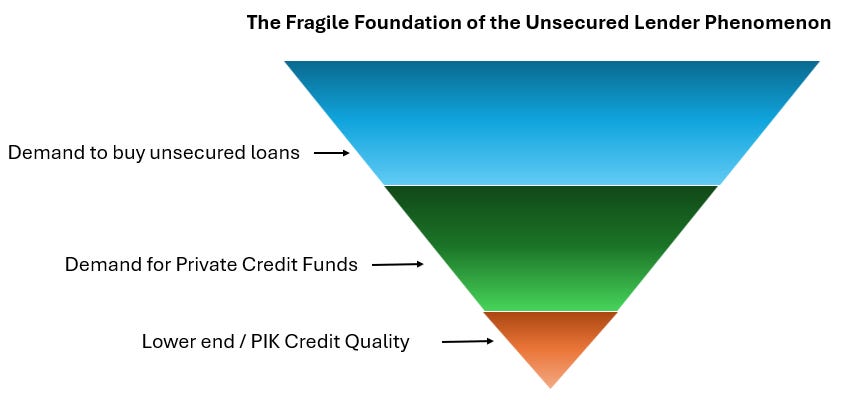

So the foundation for the rally in unsecured lenders may look a bit like an upside-down triangle:

Yes, fintech lenders sell to other buyers, not just private credit firms like Blue Owl. They sell to Wall Street and credit unions. But if you read the transcripts you learn that private credit is the driver, in size, of the origination growth at most of the unsecured lenders (though strangely AFRM has no deal with OWL as yet).

This is admittedly a complex topic with more factors than 5 Points can concisely address, so let’s also check everyone’s wallet.

Putting their money where my mouth is. I prepared a separate segment on insider activity in these names, but there is so much selling from so many insiders that it would be excessive to list it all out. The highlights:

UPST CEO Girouard this summer began selling ~$3mln worth a month. Insider selling is a feature at UPST; $135mln worth net over the past year and $2.3bn over the past 5 years.

SOFI: Offered $1.7bn common at the end of July, and insiders are lopping off an additional $600mln over the past year and $2.6bn over 5 years.

DAVE: COO and Chairman are selling $5mln worth combined in mid September.

AFRM: CEO sold $26mln worth a week ago, and $15mln worth in August.

So why end with a whimper? These stocks are 30x EPS selling loans with a somewhat low barrier to entry (CBNK is looking into the game given management’s expertise from Capital One).

Because private credit doesn’t carry much leverage. There is no run on the bank, no hung securitization. The fund just stops buying and SOFI does not send as many mail solicitations.

This “whimper” could lead to 50-75% declines in some lenders’ share prices, whether in happens next year or some other time, but the root cause probably will not make many headlines.