Mid Month: The Other Side of Schwab

Earnings notes, fixed to floating bonds, real time short interest, how loan funds take more risk, Schwab vs IBKR

Charitable update: Our first donation went to Children’s Hospital of Alabama a few months back, and we have another $10k+ to give. I’m working now with a former colleague who is setting up her own operating foundation around social work in Mobile, AL. I will have more to share on this in coming months.

Narratives: Use them to your advantage. Maybe I should put this in the footer to this note as an evergreen message. Bank sector investing tends to be driven in the short term by narratives. Folks who have read more than a few of these 5 Points have picked up that a lot of the content is me finding popular narratives, and giving data on why they are wrong.

But rolling with narratives, whether true or false, can support short-term performance. “The 10 year is broken” “Banks are insolvent” “First Citizens is the only same name to own because the FDIC has blessed them”. In the short run the game is to not fight them when they are developing, but rather to wait and see how far the market will take things before acting. Then you can generate returns.

The current narrative is that margins will continue to compress, deposits will leave the system, and credit will begin to spiral. That narrative is expressed through short interest data shown below in point 4). But ultimately narratives intersect with fundamental data. In 2008, the data matched the narrative. So far in 2023, we are not getting much follow through on the catastrophe thesis, at least thus far in 3Q results.

Think now what the next narrative might be - reversal of short rates, contagion etc. Then spend some time away from other people’s opinions and find as much data as you can.

On to the 5 points:

1. What you might have missed during earnings

Throughout earnings season, management will make conference call comments that most people ignore but which have broad longer-term impact. A few examples are below:

a) PNC on nonperforming assets

First, let’s hear from the commentators with crypto backgrounds:

CEO Demchak is not speechless. “Our criticized list didn’t really move.” I’m not involved in PNC but at this point in the cycle this is another better-than-expected credit metric, even in the context of office weakness.

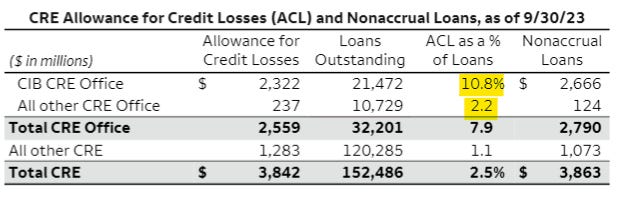

b) Wells Fargo (WFC) outlines the difference between CRE of their large corporate clients and CRE in their retail book, highlighted below. Perhaps this is a microcosm for the banking sector as a whole. I write about this every edition so will not belabor it here.

c) Schwab (SCHW) saw some short covering post 3Q results. There were enough “Schwab can fail” threads in social media that lack of contagion is positive. Moreover, on the conference call management is hopeful that deposits will turn up again.

The reality is that Schwab’s deposit performance is among the worst in the entire banking sector and there may be longer-term repercussions given the customer experience, with more detail in point 5) below.

Mortgage: Some mortgage providers remain in business (!) While origination volumes were no better than the weak 2Q levels, gain on sale margins rose 0.2 - 0.5% at PNC, Wells and JP Morgan, and servicing rights were of course also marked up.

It’s possible that mortgage could again become a material contributor to bank income statements in 2024.

2. Fixed to Floating Bank Bonds

Often during recessions the bank bond market becomes less efficient. There are some signs of this today.