Mid-Month: Inefficiencies in Small Banks

also: Truxton repurchase math, tangible book growth & total return, Homestreet's valuable license, and multi-family credit.

Good afternoon,

In this note:

Brief notes on apartment credit and HomeStreet Bank’s apartment loan servicing, then 5 Points on:

Market structure continues to change, leading to inefficient situations like Blue Ridge (BRBS) shares rising in front of a nasty credit event.

The similarly-inefficient bulletin-board bank lag: Mountain Commerce MCBI, vs Servisfirst (SFBS) and Southern First (SFST), and how bulletin board-listed banks trade differently from their Nasdaq-listed competitors

Whether Truxton (TRUX) or other fee-heavy banks trading above tangible book should repurchase shares

How tangible book growth helps explains long-term outperformance.

The consumer loan gain on sale model that the market seems confused about.

Brief notes:

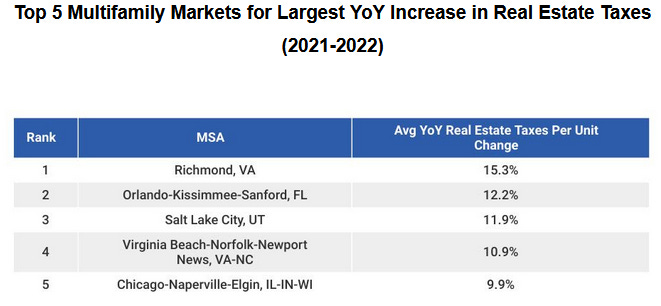

Continuing with our pattern of credit indicator monitoring. With the Wall Street Journal warning us about apartments, Trepp (Trepp.com) has recently shared some interesting color on the market. Asset quality issues that continue to pop up among certain banks and REITs (ABR, MBIN among many) are not necessarily just from higher rates. Keep an eye also on expense ramps:

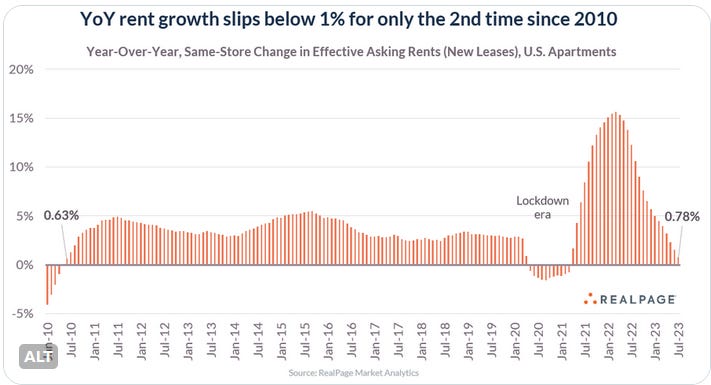

I am not a multi-state property manager but I suspect these expense increases have not subsided much in 2023 either. However, rent growth does seem to have subsided, according to property management software provider RealPage:

HomeStreet (HMST) and their valuable license

HomeStreet is a Seattle-based lender that aggressively issued fixed-rate commercial real estate loans for many years. With higher rates, the bank is now looking at possibly losing money while at the same time running only 5.5% tangible common equity. In light of this it trades 38% of tangible book and has hired an advisor to help it find options to exit its tight position.

Blue Lion Capital, which has had differences with HomeStreet management over the years, has suggested the bank monetize its rare license to originate and sell Fannie multi-family loans, called Delegated Underwriter and Servicer (DUS).

This is a valuable license, because it lets banks act on Fannie’s behalf to make an apartment loan, then sell the loan to Fannie, then collect fees for monitoring the loan.

HomeStreet’s CEO has downplayed the value of this license however, leading many to wonder if he has an agenda.

I won’t go into my discussions here on the specific market value of the license, but there are some good takeaways from this. They are:

With their funding stabilized, many banks are stepping back out into M&A and a bank like this is going to have a bullseye on it, particularly with the license: A capitalized buyer can pay a large premium for this pile of assets, improve funding, and potentially create substantial accretion in 2024. This is particularly the case if the buyer has light loan demand and would run with excess capital or liquidity. Note - almost every bank in America currently has light loan demand.

Multi-family servicing - maybe more banks should do it Freddie and Fannie generally make it manageable to get started and servicers scrape excellent fees for sending out emails, plus they generate low cost deposits for escrowing funds.

Why hold fixed-rate apartment loans with no offsetting deposit on balance sheet, when you can shift that to the government and still keep a scrape? Do you want to end up like HomeStreet, or trade 5x book 17x earnings like leading servicer Walker Dunlop (WD)?

On the topic of Walker Dunlop, their servicing net margins are around 25%:

On to 5 Points: