Mid June Weekend Reading

The Bank of Fukushima and other Japanese banks, FCNCA math, Lending Club math, what is not sustainable? Banks vs Nasdaq

In this edition:

Japanese Banks have been a black hole for 3 decades. Today, there is light with shares rallying. We take an outsider’s look at margins, profit trends, and the $50 million market cap / $5bn asset Bank of Fukushima.

5 Points’ Believe it or Not! A look at some surprising or potentially unsustainable trends in the financial sector.

Is this Banks’ year 2000 moment relative to Nasdaq? Or is the sector stuck a while longer?

The math at Lending Club (LC)

The math at First Citizens (FCNCA)

Brief notes:

Enjoy the thumbnail graphic.

Substack shows a little profile picture for each 5 Points note on the site. So in light of the recent short report on Axos (AX) I am going to have fun with the thumbnail. To offer both sides of the story, an excerpt from the Axos 8k has been added:

Giving update:

5 Points has sent $5k this month to Camp Smile a Mile for children with cancer. Thank you to paid subscribers for supporting these gifts.

To elaborate on this process, we get to give away 4 $5k grants this year but that will leave some excess, which will go into a tiny foundation that files a form 990. Because the foundation invests in flywheel small banks it should grow over time. Between that cushion and subscriber growth, next year we will hopefully be able to give 4 $10k grants.

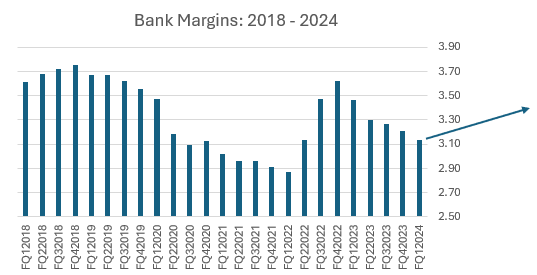

Banks are not all gloom - watch margins.

Making money in the financial sector is often a function of owning what sparks the imagination of generalists. Few generalists feel compelled to invest in the sector today for various reasons, including the average net interest margin chart for US banks over $10bn, shown below.

However if you ask any reasonably-managed bank they will tell you they are likely to start seeing some margin expansion in the second half of 2024, which should continue into 2025. This is supported by surveys and earnings calls across the sector. The blue arrow below is a potential direction, even with only one rate cut into year end:

On to the notes:

1. Japan: The land of the rising bank multiple

Have you given thought to visiting Japan? There is impressive skiing, the cities are clean, and Japan has 414 Michelin-starred restaurants. Now that the politicians have so dramatically weakened their currency, Tokyo hotels cost about as much as an interstate Red Roof Inn:

With interest rates rising, Japanese banks have finally gotten a bid as well. See Bank of Yamaguchi below as one example:

But I will stay stateside when it comes to investing in Japanese banks. Anyone with reasonable banking acumen can see why this sector, although shares have been rising, is structurally un-investable for longer-term investors.

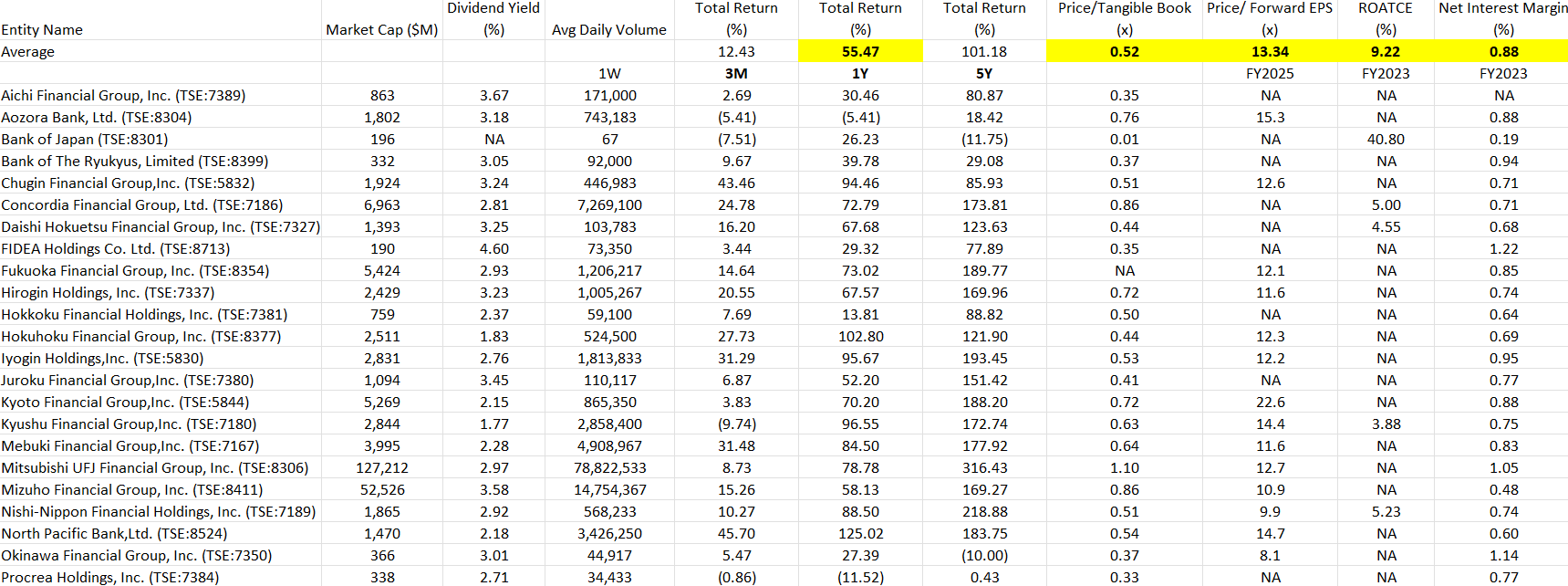

Below are all the publicly-traded banks in Japan. Note the unusual averages below in yellow:

A few notable statistics from the tables above:

10 of the banks above carry more than 6% tangible equity. In the US, 8% is low. By this measure the entire country’s banking system is under-capitalized, barring perfect credit (credit is not perfect).

Despite not having much equity, only 4 of the banks trade above book value. Trading above book value is a shorthand for a bank’s right to exist as an independent entity. In other words 90% of the Japanese banking system is priced as if it should close or merge.

Related to the above, 19 of the banks make a margin over 1%. I consider 2% enough margin for a spread bank to safely exist, because of the math for how levered a bank has to be to make decent ROE with a margin that low (about 30-35x levered).

Let’s look at Bank of Fukushima to illustrate. This bank is, pun intended, a “hot” stock up 30% or so during the last year, despite only $50 million market cap.

But I might not go within a 3 mile radius.

Fukushima has $5bn in assets but only $160mln in capital, which is at 2.5% is too low a ratio for any bank.

Credit has been melting, with problem loans at 42% of equity.

Fukushima has 560 employees, or about a person per million in assets, which is perhaps 3x too many in this westerner’s eyes.

The company makes $1 - $2 million in a typical quarter, which is not desirable on an asset size that big.

Japanese banks are of course a repository for Japanese government bonds and Fukushima owns $1bn worth. Because Japanese bonds pay 0.99% on the 10yr but Japan carries over 200% debt / GDP, these are among the more questionable risk / rewards in the global capital markets. But someone has to own that; and that entity is Japanese bank shareholders.

On the positive side, the bank does a number of commendable services for the local area.

What have shares done? Longer term, the chart is radioactive:

We must say sayonara to the idea of trapping capital in any of these businesses.

2. 5 Points’ Believe it or Not!

Do you ever see something in markets and think “I can’t believe that’s taking place.”

Roaring Kitty, Davey Day Trader, a 2x NVDA ETF up 450% year to date etc. We all remember SPACs, of which 90% subsequently underperformed the broader market.

The financial sector also has a number of items that we could include in a 2024 Financial Sector Believe it or Not! museum.

Let’s look at some nominations:

Payment in kind loans: “Those are as good as money” Some lenders run 30-40% of revenues from PIK loans. Prospect (PSEC) and Monroe Capital (MRCC) each run over 30% of their loan book, and New Mountain (NMFC) and Blue Owl (OBDC) carry just under 30%.

Banks see PIK as another word for nonperformer but in the business development company world this is a widely-accepted strategy.

BDCs may further be delineated on whether the PIK was an initial part of the loan structure or represents a subsequent material restructuring in a stressed credit This practice has been more prevalent at Investcorp (ICMB) and again Prospect (PSEC) at over 10% each. Be sure to check this disclosure before adding a BDC to your portfolio.

Credit Unions: taxes are for the little people (banks): Leona Helmsley was speaking off the record but it’s publicly known that credit unions are on track to buy over 20 banks this year, as not paying taxes is a better deal than paying taxes. CU managements also get to increase members and executive compensation with these deals.