Mid December: The banks trading under 6x earnings

Good morning,

I’ve included some “brief notes” about the updraft in bank shares before discussing some valuation- and corporate governance-heavy topics.

Truist is giving this season - competitors are finding market share under the tree.

The banks trading under 6x 3Q annualized earnings, still.

Share repurchase incentives: Why a few banks have been shy about repurchasing shares at recent lows.

Asian banks sorted

First IC and Solera, two banks trading at 2-3x earnings

Brief notes:

Lets all get rich: After the last few days, as tempting as it is to start trading any number of financials that are ripping like FFWM or UPST, step back a moment.

First, don’t even try to forecast macro, unless you are paying 6 figures for data and have a process honed over several years.

You may want to try to understand positioning, sentiment, and market structure. If you don’t understand it (you probably don’t), then acknowledge that you are speculating and use sell stop orders and some kind of defined process and a log.

If you are new to a situation, you cannot assume you have an advantage just because you have an opinion.

Instead, perhaps try being patient and looking at angles less widely considered. For example:

Mortgage may benefit from this unusual bond market. Who still runs a mortgage company and are they otherwise attractive? (HTH, WAL, WSFS, NYCB are a few that still do mortgage)

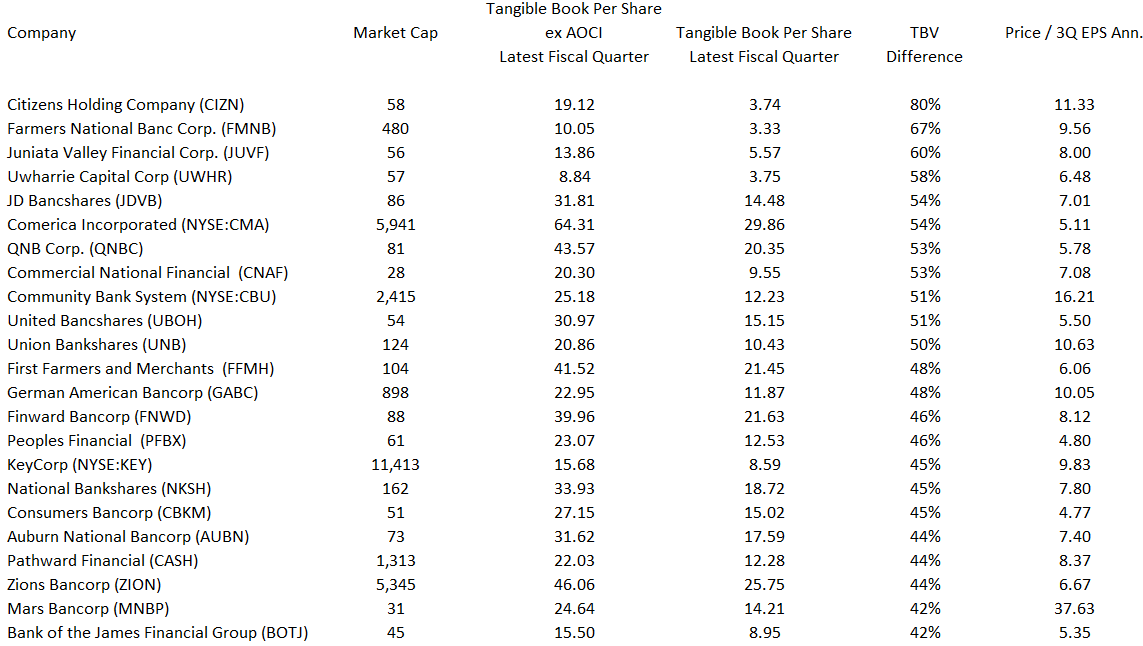

As noted two weeks ago, more valuable bonds can mean balance sheet upward marks. Which banks might now access the liquidity from underwater bonds to fund loan growth? BAC, CBU, FFIN among many others have been patient here. This angle is why I published the AOCI chart in the last edition, which I will show again here (sorry, that P/E column at right is no longer very reliable):

Finally, banks trade differently depending on whether they are bulletin board or listed. If you don’t want to chase the listed companies up 20% in a few weeks, many bulletin board banks are often superior quality and tend to lag.

The point is to get out of the macro investing big leagues and try to find the open gate into slow pitch softball.

On sentiment then, do banks have more upside?

You can gather a number of sentiment surveys but I’ll save you some time. Bankers aren’t 100% on insider buying vs selling but selling has been particularly intense lately.

PNFP Chairman Rob McCabe, who is not a clown, just let go of 100,000 shares worth $8 million.

at JPM Marianne Lake sold $5 million worth

On the island, FBP CEO Aleman dumped a half million worth.

An M&T director sold $5 million worth.

Huge sales also at RF, IBOC, VLY, and SNV

All this is before the Fed pivot rip. Bank valuations remain on the generous side (few are over 10x next twelve months eps even now) but again, study what you are buying before you just press buttons.

On to the 5 Points:

1. This holiday season, look to Truist (TFC) for the gift of market share.

Anecdotal evidence is tricky, but a common hypothesis is that Truist is on a path similar to Regions (RF), where a large merger generated years of market share transfer.

Today 15+ years after the Union Planters and AmSouth mergers, 27% of Regions’ loan book comes from shared national credits. Regions might argue this is because its markets are deposit rich, but as a Regions observer I wonder if local high-value commercial relationship customers have simply moved on from the bank, and been replaced with wholesale participations.

As one bank investor friend shared with me “It’s really a great business. They get deposits from the folks who are willing to be treated like (badly) forever, and then they lend the money out with no credit risk.”

The issue is there is a finite and dwindling supply of people interested in that level of service.

Today, Truist is showing similar tendencies, if public surveys and numerous anecdotes are to be believed, plus the fact that mergers can be highly disruptive and difficult to manage:

To a degree, this is showing up in the numbers. Alongside difficulty with bond portfolio positioning, the bank’s operating challenges have led to earnings shortfalls for 5 straight quarters:

Again, I can’t say I would do a better job if I were in management’s shoes - merging two mammoth banks is extremely difficult and much of this market share is the kind they cannot handle or do not want anyway.

So let’s look look at the opportunity for smaller banks as customers consider options.

In years past, Regions’ challenges led to the success and growth of Pinnacle (PNFP).

Likewise Truist should feed banks like Southstate (SSB), Ameris (ABCB), First Bank (FBNC), Servisfirst (SFBS) among larger subregionals. Almost any $1 - $10bn bank from Florida through Tennessee, Georgia, the Carolinas, and Virginia will benefit just by opening the doors and banking with a human who makes decisions. This could include BHRB, SMBK, FBMS, SYBT, SFST, THVB, IBTN and CBAN among others.

Next edition we will look at another catalyst for market share transfer - the changes in risk weightings affecting most banks over $100mln, again helping small banks and non-bank lenders alike.