May: Will Anything Blow?

The amazing story of Janover; What's wrong at Live Oak? Beautiful de-regulation, How Preferred Bank got it right

In this note:

Will there be a Silicon Valley of this cycle? What looks fragile?

Bank Deregulation on the horizon

The 1400% move in one month at Janover (JNVR)

What went sideways at Live Oak Bank (LOB)?

What went right at Preferred Bank (PFBC)?

Brief notes:

An update to “Coastal’s moonshot” I’ll increasingly use the brief notes section to follow up on prior edition stories. Coastal Financial (CCB) is unique among public banks in the size and complexity of fintech partnerships they have signed. One of these recent partnerships was a bit downmarket for Coastal - Dave Inc. (DAVE).

Dave is in the business of giving people one-week, $100 loans to make rent, keep their car etc. Dave advertises interest-free loans but ends up making triple digit rates from fees and “tips”.

So why would Coastal pollute a client base that includes Prudential, Progressive, Wal Mart, T Mobile and Robinhood with a fast-cash operation?

Recall the “Coastal’s Moonshot” piece from late last year, discussing how Coastal could seek to build enough households to feasibly create a competitive payments network in the US (such as the one Capital One seeks with Discover to target the V/MA duopoly).

Dave has 6 million customers and is growing briskly. Coastal won’t say, but between their various partners I suspect they now serve close to half the US consumer population directly or indirectly through partners. They connect to me through two relationships already, and I haven’t even signed up for the Robinhood Gold card yet.

Next Month - two topics that got pushed due to lack of space in the note - a look at UMB Financial, and which banks are growing moat and which are eroding it?

on to the notes…

1) Will Something Blow up?

A client asked me this question. Who could be the Silicon Valley Bank of this emerging slowdown?

My initial impression is that the current tariff situation is a employment problem for people working in fields like distribution, construction, retail etc. I’m not sure it extends to become a broad credit issue.

Still, stretching and tearing parts of the economy can have ripple effects. Less shipping means less trucking and less retail sales and fewer accounts receivable etc. and if any part of the chain is over-levered, it becomes a story in 5 Points.

We also know that the President wants to move towards a balanced fiscal budget and a balance in trade. He is known for saying one thing and doing another, but if this discipline manifests, then tariffs are only part of a contractionary new economic backdrop.

The “balancing budgets paradigm” involves DOGE, making students pay back their loans, firing DC employees and many other things that can pressure they economy and markets…while we wait for tax cuts, regulatory reform and hope that M2 keeps growing.

Let’s look first at fragile parts of the economy, and then fragile parts of the financial sector.

What parts of the economy look fragile?

We can agree there should be pressure on: shipping, trucking, ports, hospitality and travel, small manufacturing, wholesale distribution, government contractors, retail, agriculture, materials, construction, maybe autos, and medical research, among others. Also, the services that support them, such as advertising and consulting.

Capital markets are morphing, affecting the cost of capital, slowing or shutting IPO markets, affecting mergers, spreads, and possibly the wealth effect.

Consumer borrowing is in flux Spare a thought for stuck student borrowers. 9 million delinquents have to start paying again, or have wages garnished / refunds withheld. BNPL providers are now reporting to the credit agencies, shutting a large consumption loophole that allowed 600 FICOs to masquerade as 650-700.

On the bank side, we are seeing clients pause on bank loan demand and capital spending. Obviously this is dependent on sentiment but we need not just lower tariffs but also consistent policy in order to reignite plans.

What parts of the lender complex are most fragile?

I believe SBA lenders, lower end consumer lenders, and BDCs among others will have a volatile 2025. Some will see an “earnings event”, meaning companies miss earnings, and others a “capital event”, meaning companies lose money or worse.

Let’s bring out the contestants.

Transport lenders: Already a capital event: Triumph (TFIN) is now on the verge of losing money even before ports emptied out. Ongoing heavy corporate overhead and lighter volumes left the company with a 0.00% ROA in 1Q. Below is a snapshot of the freight market:

Cass tells us that “the trade war is likely to extend the for-hire freight recession as higher prices reduce goods affordability and consumers’ real incomes.”

Cass and Triumph are two different models. Cass focusing on forward freight market and run as a bank to support a cost-saving software. Triumph focuses on the spot market and wishes to be seen as a payments company while also lending on commercial real estate and truckloads.

Both have seen recent hiccups but Triumph much more so than Cass.

Despite consistently missing estimates, Triumph still trades 52x forward estimates that they presumably will be challenged to hit? Colarion thinks there are safer places elsewhere to invest into 2025.

Consumer lenders: earnings event for most

Bread Financial (BFH), Enova (ENVA), SOFI, Affirm (AFRM), Upstart (UPST), Ally, Capital One (COF), Synchrony (SYF) among others.

This is a tricky subsector and you should study each of these companies in depth before making a directional bet. Charge-offs have remained steady although bad loans ramped 30%+ at ENVA in 1Q. Bread is thinking loss rates will remain consistent in the 8.2% range.

However if you expect a) higher unemployment, b) enforcement of student loan repayment for the 3% of the population delinquent, and c) higher goods prices and BNPL disruption, then most of the above will be negatively impacted.

Trade lenders: C, EWBC, HSBC, STAN.L, PFBC: Hard to know yet.

East West, like its name, has 3-4% of the loan book in trade finance across the Pacific, but sees minimal credit disruption. If a shipment gets paid for then that’s that and the loan rolls off. The issue could be loan growth, but the 4-6% East West is expecting is still respectable.

Moreover, East West and Preferred Bank are both repurchasing common in the midst of this disruption.

Surely we will see a change in trend at these lenders but this is not the eye of the hurricane. One surprisingly weak sector however is the…

…SBA lenders: Capital event

The pain began before April 2, and presumably has worsened. I think of Anthony Joshua fighting David Dubois. Joshua got tagged at the end of round one, and for the balance of the fight was just trying to hold on until Dubois ended it.

SBA lenders got tagged in the first quarter and are currently clinching to hold on until Trump administration pivots to more constructive policy to avoid a 2Q / 3Q knockout.

Our contestants:

First Internet Bank (INBK): 1Q25 ROE: 1%.

Live Oak (LOB): 1Q25 ROE: 4%

Bayfirst (BAFN): 1Q25 ROE (1%)

Newtek (NEWT): not yet reported, expected nicely profitable.

Nonperforming loans are a growing problem at these banks:

Government guarantees on a portion of SBA loans should minimize charge-offs, but those are elevated and in some cases growing as well:

On top of this, the sector is working through rules that increase borrower fees and change underwriting. Here’s “proof” from a dramatic headline at the actual SBA website:

In good times we should appreciate Newtek’s willingness to push boundaries on what kinds of credit can be accepted under a bank holding company. I don’t think this is one of those times. Both Newtek and Live Oak have expanded more into business loans without real estate collateral, which is where we could see greater “credit evolution” as the year progresses.

The most aggressive business lenders: (BDCs) capital event

A reminder that business development companies are a type of tax-advantaged “private credit” fund that pay out most of earnings. Every time I look at BDCs I conclude the upside is not far above the dividend yields while the stout recession downside is 50-100%. It’s hard to know the tipping point on this downside, but a few observers are tracking the “cracks in private credit” that we should continue paying attention to.

We also should mind the 13%+ look-through management fee of the BIZD ETF, below, that we pay for this investment opportunity.

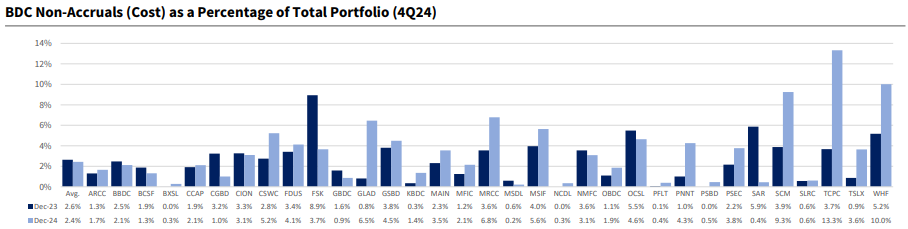

Moving to individual situations, one place to start would be this chart from Raymond James showing bad loan levels across the complex. Pardon the font, the tickers showing the most bad loans are TCFC, WHF, SCM, MRCC, and GLAD

Companies that have sustainably earned less than their dividend include MRCC and WHF.

MRCC can justify this by earning net investment income greater than their dividend, such as in 4Q when NII was $0.28 and the dividend was $0.25, the difference coming from portfolio marks that pushed EPS negative. This seems like burning the furniture to keep the house warm but it maintains retail investor confidence and presumably MRCC’s market access.

How these companies manage their capital to avoid margin calls is impressive - tight dividend coverage, tight cash flows with 10-20% of the book paying in kind, tight debt service coverage ratios from their lenders to avoid margin calls on illiquid assets, and marks required for secondary-market sales.

My hats off to the management teams - so far!

Are you seeing additional pockets of stress in the markets? I’d appreciate hearing about it.

2) Beautiful, underappreciated, bank deregulation - do we have any other choice?

Tariffs dominate the headlines but a deregulation impulse is under way in the banking system. Bessent and Fed nominee Bowman both want to pursue it, but it’s perhaps not a matter of them wanting to as having no other choice if we are going to tame the debt spiral and handle bond market volatility.

Jamie Dimon introduced the topic on his 1Q JP Morgan call:

If you have to fix LCR, G-SIFI, CCAR, SLR and I think would free up hundreds of billions of dollars for JPMorgan annually of various types of lending to the system. Some would be market, some would be middle market loans, et cetera. And I pointed out, if you wanted to look at the big numbers, that loans to deposits are now 70% for the banking system large. That used to be 100% and the reason for that is it's not just capital. It is also LCR. It is also G-SIFIs

An additional 30% loans / deposits from the big 4 plus PNC and USB would be $2.4 trillion in loans. That is about the size of the entire private credit complex.

A good question is why we aren’t growing loans part of that $2.4bn to generate tax revenue, instead of going the “leave ‘em guessing” trade war route.

Here’s more math, from Treasury Secretary Bessent:

There’s a capital charge to banks for buying Treasury bills … If we take that away — it’s become a binding constraint on banks — we may actually pull Treasury bill yields down by 30 to 70 basis points. Every basis point is a billion dollars a year.

Bessent is referring to the SLR is Dimon’s lineup. The issue is this ratio requires large banks to carry 5% capital to assets regardless of the asset. The bank could hold 100% gold and T bills and the ratio needs to be 5%. Dimon argues that treasuries or particularly T bills are cash and should be exempted from this calculation, as they were post Covid until early 2021. JPM holds massive amounts of T bills to support trading and liquidity requirements, and would probably hold more if not punished for it. Bessent and Bowman seem to agree.

So we might conclude that:

The straightjacket that led to the market share shift from banks to private credit could loosen.

Bessent can unleash much lower yields and materially stronger GDP simply by exempting cash from capital requirements.

Once Trump figures out the power of this lever he will demand it be pulled as soon as possible.

This would be a very positive development for large bank ROE and capital return.

We are also seeing:

Fast merger approvals, including the flexibility for larger banks to transact again.

Fast consent order resolution, judging for example from Wells Fargo closing 6 of 12 consent orders this year alone.

An approach to remove obstacles to small bank formation and growth rather than add them. This is a broad topic championed by Fed Head of Supervision nominee Bowman

We may even see a rollback of pointless penalties on banks for owning Mortgage Servicing Rights. Here is Bessent in March - finally we have someone who understands!

When considering the effects of bank regulation on community banks, we should ask ourselves why so much financial activity has moved out of the regulated banking system. For example, the shift of mortgage lending to nonbanks has undercut an important line of business for community banks.

It is clear this shift out of the banking system is to some degree driven by regulation—and in particular by outdated capital requirements on some exposures that are well in excess of the latest evidence on the actual risk of those exposures. (https://home.treasury.gov/news/press-releases/sb0078)

If Bessent does in fact have a way to overturn archaic capital charges against mortgage servicing rights it would be a boon to JPM among others (hundreds of small banks) and impede Rocket (RKT), which has become the 800 lb gorilla of the mortgage market, with a barely investment-grade rating.

2025 Bank de-regulation could be as helpful to the sector as several interest rates cuts, yet seems to be ignored by the broader market thus far.