May: Why Does NU Trade at 8x book?

A 5 Points scorecard, Citi's potential, Triumph Financial, Capital Bank's acquisition

Good morning,

1. Grading some recent 5 Points editions: several winners, a few juries still out

Citi (C) has gotten started creating a functional organization; there is far more work to do

Triumph (TFIN) is still struggling with generating a proper return on capital; the 10k shares a concerning corporate segment datapoint.

Why does South American bank NU trade at 8x book?

Capital (CBNK) and the constructive approach to a bank acquisition.

Brief notes:

The Russell wave. Today is the day for ranking who will be added and subtracted from the Russell 2000 this coming June. For some small banks this can move shares almost as much as a merger. As Russell publishes its list, Blackrock et al are forced to buy about 15% of the float, sometimes in companies whose additional surprises the market.

The market capitalization cutoff will be between $130-$140 million. VABK and FINW are a few to watch, with PWOD hoping to make it.

Affirm, Walmart, and the challenge to fintech from embedded banking.

Affirm is a company that lets you pay for something in 4 installments. They have a partner relationship with retailers like Walmart:

Or at least, they had a partnership.

We discussed this a bit in the prior edition with a review of Coastal Bank (CCB). What’s interesting is that this may be a new paradigm for delivering financial services.

In this relationship, Walmart finally gets to take the attributes of banking it has always wanted to control. Affirm’s margin on BNPL is Walmart’s opportunity. This extends to point-of-sale lending that might have otherwise been funded by an outside debit or credit card.

Home Depot, Delta Air Lines, or any other entity with millions of customers may be tempted to do the same, because Banking-as-a-Service, or Rent-a-Bank as skeptics call it, has properly evolved at a few select banks.

The Pathward ($CASH) conference call transcript has helpful color on this process.

The Walmart marketshare shift in BNPL may be the first in a pattern of transfers from consumer fintech lenders if this template holds. It may create an EPS bump for large retailers. The potential impact for those select bank partners can be proportionately much larger.

1. The 5 Points scorecard

While this note does not recommend stocks, it may help readers understand sector opportunities. To that end, it’s helpful to pause from time to time to see if the note is adding value. Looking back….

- The Mid April note profiled Coastal Bank’s partnerships with fintechs like Robinhood and One Finance before Coastal shares ramped 10%. Coastal just gave back some of the gain in a 1Q earnings report (the note also predicted that result). A few weeks is a short timeframe to tell but keep an eye on Coastal’s model, which sidesteps credit risk but keeps the spread.

That note, as well as the November note, also critiqued credit risk at Eagle (EGBN). EGBN fell 13% on April 25, due to credit.

- The April note suggested there may be better shorts than TBBK, a recently popular short, in the low $30s. TBBK then printed 3% ROA and 28% ROE April 25. Shares remain a “battleground” because TBBK management is unconvincingly trying to suggest credit is strong. We look further into this below.

- 5 Points was cautious on TBBK before becoming more balanced. The Mid March note profiled the same TBBK credit risk that ended up pushing shares down 25%. This was a follow up on the November note, which mentioned the credit from the call report that everyone began worrying about 4 months later.

Mid March also introduced FCNCB as a beneficiary of a First Citizens buyback; it has since materially outperformed.

March discussed the return profile of the BANC preferred, a redemption candidate trading at a discount, before it bounced 10% plus accrued interest.

February posted that estimates at New York Community (NYCB) were too generous and that valuation was not compelling. Shares have since been cut in half.

5 Points’ hit rate is not 100%, but on balance has blended enough common sense and sector knowledge to be relevant.

If compliance allowed me to discuss Colarion’s track record, that might be the most convincing argument that 5 Points is worthwhile. As it stands the note will continue to dig for data and stand on its own merits.

A picture to follow up on Bancorp (TBBK).

As noted I recently wrote that TBBK is, despite its Betsy Cohen-inspired apartment book, too profitable to be a great short in the low $30s.

Sometimes we forget that stocks are an auction and the reason to buy a stock is because we think someone will come behind us wanting it more. It’s a good exercise to think about who that could be given TBBK’s volatility in recent days.

Bidders at the auction are coming and going. Below is a picture of some attendees:

Why was this picture out of balance Friday and the stock fell 7%? Because of the swing vote below.

As TBBK management talked around potential delinquencies in their 1Q call, shorts were emboldened.

Longs have to be patient for the repurchase - typically companies are mandated a quiet period before they can repurchase after an announcement (TBBK announced an incremental 3% repurchase in the quarter).

After that period is over, management then will fit $50 million of additional buyback into the remaining 8 weeks of the quarter. 50 million / about 42 trading days is ~38k shares a day, on top of the ~27k shares already being bought. 65k shares a day of demand the next 42 days is about 10% of volume.

This repurchase represents about 6% of shares outstanding and presumably will influence the auction. Later, we might expect volatility again as the 10Q is filed with credit disclosures.

2. Citi’s initial foray at cutting expenses: “Once more, with feeling” (then build a habit).

As many of you know, in the short period from 1998 to 2003, Citigroup CEO Sandy Weill, famous for firing Jamie Dimon, acquired Associates First Capital, Salomon Brothers and Banamex among other acquisitions in an effort to create an empire that ultimately become too complex to effectively manage.

After this ball of twine was created, his successors could not manage the inefficiency that dragged the organization down. High performers tended to leave in a bureaucratic environment. In recent years, Citi has consistently returned 5-8% ROTCE, near the bottom of the US banking universe.

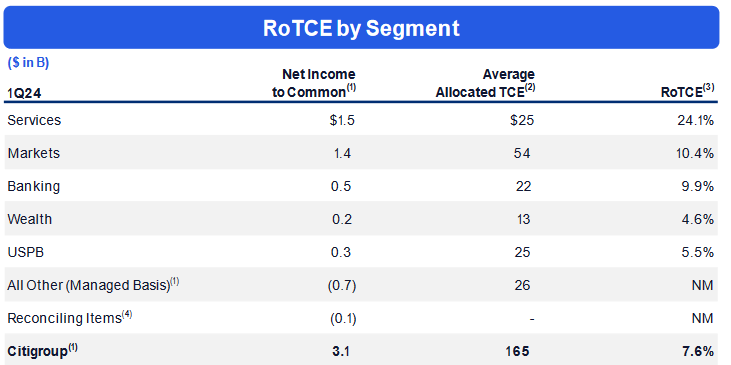

Helpfully, Citi discloses two tables why it does so poorly. First, we see it by ROE below in the 1Q presentation:

Then, they share it through net margin in the 10k:

We can see that services (treasury management, payments, “data solutions”) is a good business.

Markets is an average business at best, yet Citi allocates $54bn in capital to it and almost a trillion dollars in cash. They are at least trying to address this by shutting municipal underwriting.

Banking is a bad business the way Citi does it - with excess overhead and not enough spread on corporate borrowing, but they claim it feeds into wealth and markets.

Wealth can be a reasonably good business, but clearly seems bloated.

“Other”, international operations like Mexican and Asian consumer banking can be good business but Citi is quitting on much of this.

Obviously Citi is inefficient. Lately they have cut 7,000 jobs to save a $1.5 billion run rate. That seems like a lot, except that the total expense base has run $54bn.

CEO Fraser is getting credit in the market for her “transformation” but is a 2% expense cut all she wants to enact?

Suppose you are a city that is fixing a pipe under the road. What we might envision is two guys in the hole working on the pipe and eight people with orange vests directing traffic and smoking cigarettes. This demoralizes the two workers because they would rather make more money and not listen to the smokers tell them how to work.

Similarly at Citi the company can cut its way to growth and efficiency by empowering its “A” players with greater responsibility and incentives, paid for through layoffs. Another example is like pruning a plant to let the stronger branches flourish.

If Citi gets in the habit of cutting to grow, then we know they have found the way.

3. Triumph (TFIN)’s ROI challenge: a follow up.

This post is an update to a November 2022 post questioning whether Triumph could turn around its stock price.