Lessons from Ready Cap’s 90% haircut

Time for Inbank (INBC) to move out, DCF for First Northwest (FNWB), North Carolina banking paradise; forced selling at CLBK; Column and Cross River are resetting banking.

Good morning,

Congratulations to our readers investing in the AI “bottleneck”! We don’t have any Microns in the financial sector but we have some possible 40% IRRs listed towards the bottom of the note.

This quarter’s donation goes to the Vandiver and Dunnavant Alabama volunteer fire departments.

A reminder, apparently substack lets free subs unlock the paywall once, so I hope you will use that if the sub price is not to your liking (I believe it’s about 25% the cost of most sector notes and goes to nonprofits).

In this note:

Brief notes: A nasty Slide, “Cold Money”, Private credit distress tracker

The 5 Points:

Turning banking upside down by fixing what’s inside - why banks will want to follow Cross River and Column to build their own core.

ReadyCap’s 90% haircut

Why banks in North Carolina are printing money.

Time for InBank (INBC) to move out?

First Northwest (FNWB) is run by a clever CEO and sits at 60% of “unadjudicated” tangible.

Forced selling in the $1.4bn Columbia (CLBK) offering.

Brief notes:

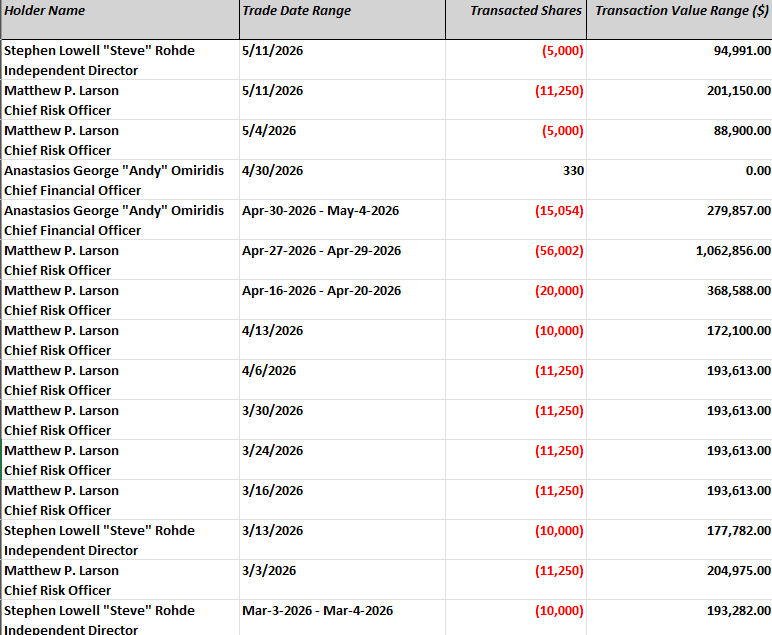

Slide (SLDE) is a strangely-named property insurer in Florida. Slide is this month’s winner of the “worst optics award” as its Chief Risk Officer systematically “insures” that he has no equity exposure to the company (these are all option exercises and puns are always intended in this note).

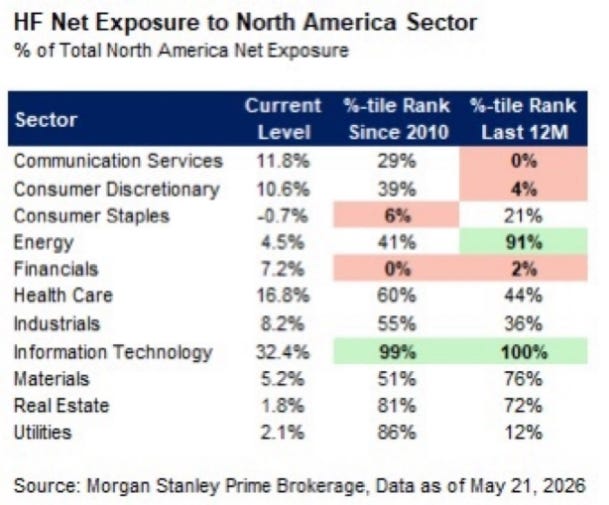

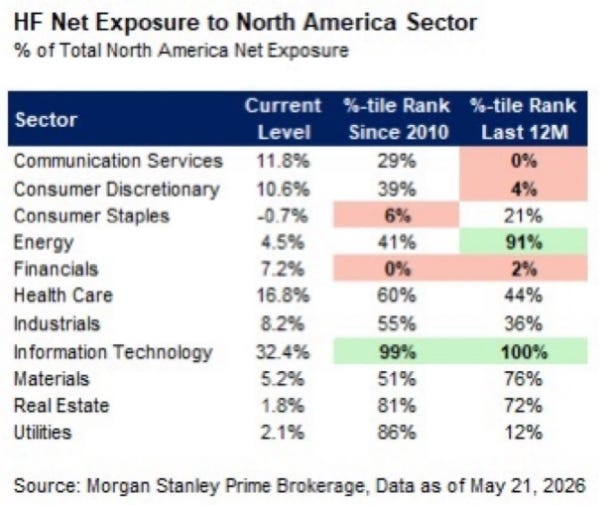

“Cold money” is the opposite of hot money. Hot money is basically hedge fund money.

Per a Morgan Stanley table shared by a friend below, hedge funds own a rock-bottom allocation to financials. These funds are relatively overweight healthcare and are all in on tech. They must have a variant perception on AI!

We will welcome the liquidity when rotation occurs. In the meantime let’s appreciate our low number when the three vortices - SpaceX, OpenAI and Anthropic - suction hundreds of billions of liquidity from the popular sectors.

Next month: a) A private credit distress tracker, and b) How do the NYC lenders (DCOM, FLG) get out of rent stabilized? Impressions from a sit down with Dime management.

The 5 Points:

1) Cross River and Column Bank have built their own cores, which could affect the entire industry

Column Bank in San Francisco is a $1bn bank focused on banking-as-a-service, or “rent a bank”. It is also among the most successful and profitable banks in the country, with equity having grown from $85mln to $145mln over the past year from profit alone. Column sees itself foremost as a software company. Here is Column lightly dunking on the industry:

I’m not sure about 100 years, but certainly the next 5!

And here is Cross River’s way of saying the same thing differently, in a blog post about how their core will more readily support agentic payments, which means letting AI pay simple bills for you. Try getting that from the corner community bank or even PNC:

A “core” is the ledger and security backbone that tracks customer accounts. It used to be that when banks built their own cores, they were subpar. Long hapless Carter Bank and Trust (CARE) used to use their own core, and could not even offer online banking until about 2019.

Now, a few cutting edge banks (those above) have built ground-up cores with more flexible features than the legacy oligopoly offerings (FIS, FISV and JKHY). Today we can expect it is easier (though not easy) and less expensive to build a core, or important parts of a core like a ledger, than it used to be.

This is why the event below and so many others like it remind me of the Matrix. All these bankers are in the legacy core straightjacket, hoping for new crumbs every year so customer-facing technology will be less bad.

I sense Column CEO William Hockey will never be found at “Jack Henry Connect”, rather he will be grinding with his 14 engineers on their own unique product suite.

Bank investors need our “investees” to get away from dependency on patchy core oligopoly as soon as reasonably possible.

Many will say this is too difficult - the cores are secure and regulator compliant. How can Column rebuild the code and practices to support ATMs, checking and mortgage processing?

They won’t. Just like Teslas use your phone to open the door instead of a key, Column et al leapfrog. They won’t support ATMs or Kids Klub checking with paper checks. From my conversation the folks at Column expect banking to go the way of Mercury, Brex and Ramp. They are working around online adoption, not paper.

Moreover Column may be coming for you and your crappy core, to buy and control the legacy deposit value while gradually retiring the marketing overhead / Linkedin army employed by FIS / FISV / JKHY.

Yes, I’m told by a reliable source that Column is looking to acquire. Hopefully the seller doesn’t have too many Kids Klub devotees or drive through clients.

While this will surely dilute their industry leading ROE, why not rip-and-replace at scale?

Bank customers will come to appreciate it, and I hope bankers will likewise invest to keep up.

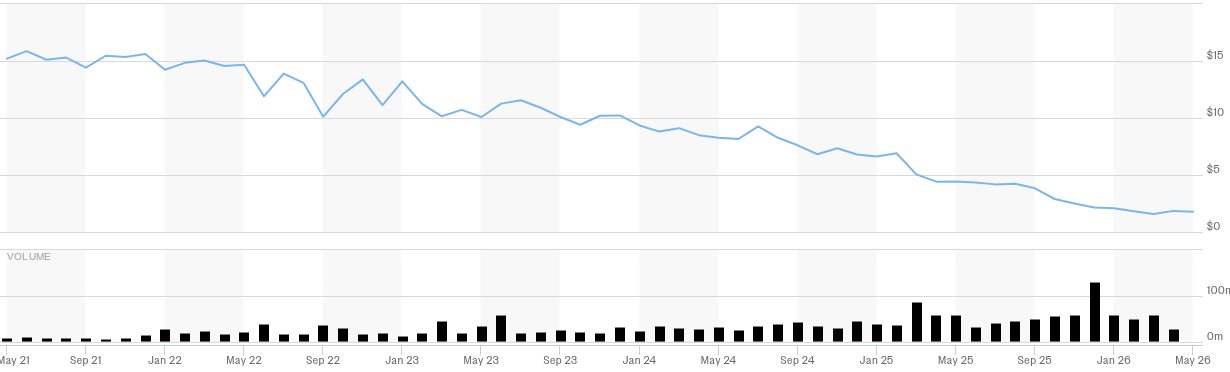

2) Lessons from Ready Cap’s 90% “Pullback”

A friend was in the SBA and CRE loan brokerage business. Our relationship was worth its weight in gold, I just didn’t know it. A few years ago he said the most aggressive loan buyers were First Internet (INBK), Bayfirst (BAFN), and Ready Cap (RC), with Sachem (SACH) nearby.

So I stayed away from them. But they were brilliant shorts! Today all four have run into the ditch on credit.

Ready Cap was perhaps the worst of all of them, a REIT lending on SBA and apartments and a regular punching bag in this note. And yet I only shorted a small amount and covered too early.

Part of the reason for this is shorting is hard so I don’t short large positions in anything. But there are some lessons here on staying bearish.

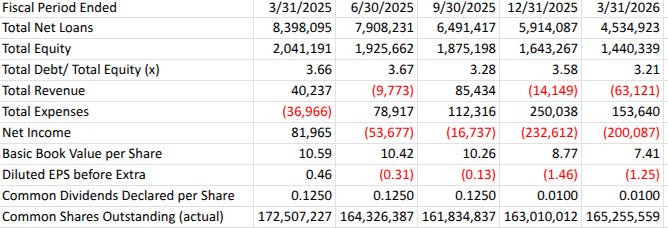

Before we dig into how RC blew up, admire the numbers. The book value implosion. The runoff of almost half the loan book in just a year. The decision to repurchase stock(!) just a quarter before cutting the dividend again, this time from $0.125 to $0.01. RC was paying $0.30 in 2024. The negative revenue.

There is a two page condensed Bible of how to lose money in credit recently published by the creatively named Shitty Situations substack. We can select from his lessons to apply to Ready.

Among them:

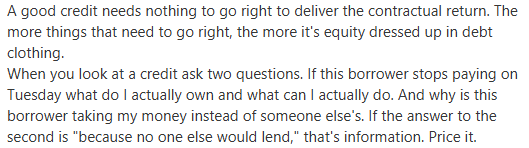

Ready Cap was making equity-style loans. These loans that require things to go right, and when they don’t, the borrower owns sand through his fingers and a legal bill.

Examples of equity loans include loans to growing software companies at the typical 6x EBITDA, many LBO financings, the unguaranteed portion of SBA (why BAFN is not a long at current prices ex rights and despite the Russell), and many reconstruction or “bridge” loans for “workforce housing”.

RC did those last two in size, in 2021/2022, and funded them with exploding financing (CLOs).

“Situations” asks “why is this borrower taking my money and not someone else’s?” Before RC shrank quickly, it grew quickly, From $4bn in 2020 to $8bn in 2021, to $10bn in 2022. Borrowers took Ready’s SBA money because the firm was spraying it out to gin revenue, during the worst possible vintage.

This note long ago covered how Broadmark Capital, which Ready Cap acquired in 2022, ran an almost impossible loan shark model trapping borrowers with high rates.

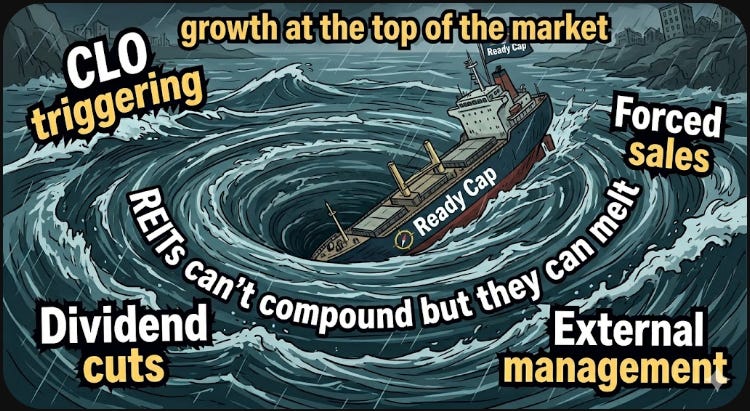

This is a long topic and your attention is finite, so here’s a picture:

To quickly explain the vicious cycle,

Ready Cap misprices clear risk, lending to Tides Equities or the Portland Ritz Carlton. Portland Oregon not Portland Maine. Buys Broadmark, makes SBA loans in 2021 etc.

Borrowers default.

Ready busts triggers in CLO covenants - it pledged loans to securitized financings, and when those loans stopped paying, it had to meet margin calls.

Margin calls trigger forced sales of performing assets.

Selling the good to make up for the bad creates the spiral you see in the financial highlights above, including dividend cuts and slashing the loan book back to 2020 levels.

So what do we learn?

A) talk to loan brokers

B) It can take years for loan weakness to play out. If credit shorts are working, let them play out!

C) Avoid companies aggressively using loan brokers.

D) Expect several more Ready Caps within the private credit complex (looking at FSK among others).

Before we go, the peanut gallery is shouting “Thanks for the recap, but does it bounce back to $10?!”

No, and it’s not obvious it bounces to $3 from just under $2 currently. Ready is at 26% of tangible book. Management is selling $1.4bn in loans the first half of this year to pay debt maturities down. This means its lenders won’t extend credit to it unsecured and the secured room is taken, which means the cost of equity probably needs to be over 20%. You can decide how much higher after the 2Q report shows the carnage given delinquencies are still 15%. There is about another $2bn in works to be sold as well.

A guess is you are left with a cigarette butt with book value near $4, loosely based on a more pessimistic view of forward estimates, a new business model, and still significant corporate overhead.

I’d rather buy small conversions for 50% of book.