January: Mike Bell Can Make Us Money / An Interview with FINW CEO

Also - overlooked bank catalysts, PFBX, CFBK revisit, ranking the capital raises, Lessons from a strange Japanese bank

Good morning,

I hope you all enjoyed your holiday break and were satisfied with this “Old Year” as we look to the next…

In this note:

Brief notes on the yield curve, an interesting setup at PFBX, and CFBK revisited.

The 5 Points:

Mike Bell can make us money. Mike Bell represents credit union buyers of banks - some of whom are aggressive - and recently shared developments the market may be missing in an online conference.

Evaluating the many recent bank capital raises, including VBNK, FFIC, CCB among others.

Overlooked catalysts for banks large and small. Chevron is already showing an impact and may be transformative, plus a look at deposit insurance and Durbin limit adjustments.

The Japanese bank retiring shares at 50% of book value gets us to rethink what we know about bank investing, and the potential for some US converted mutuals.

An interview with Finwise Bancorp (FINW) CEO Kent Landvatter, whose shares are up 80%+ from 2024 lows before recently retracing. Finwise executes unique programs that are not easily understood.

Brief notes:

The yield curve’s gift

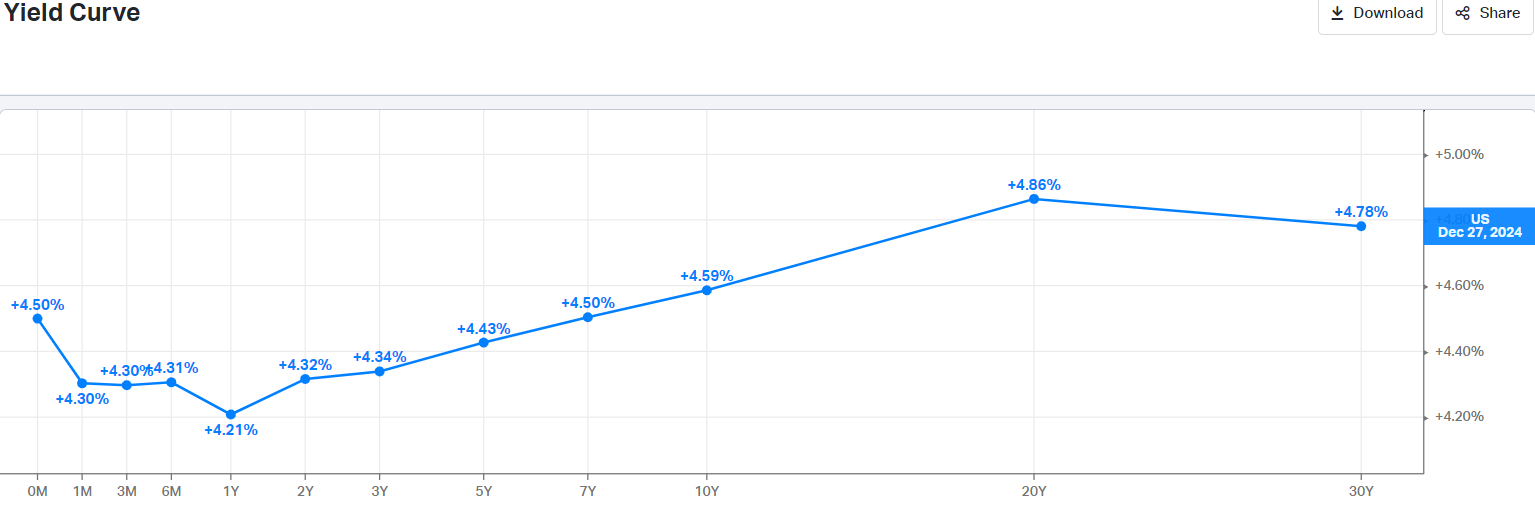

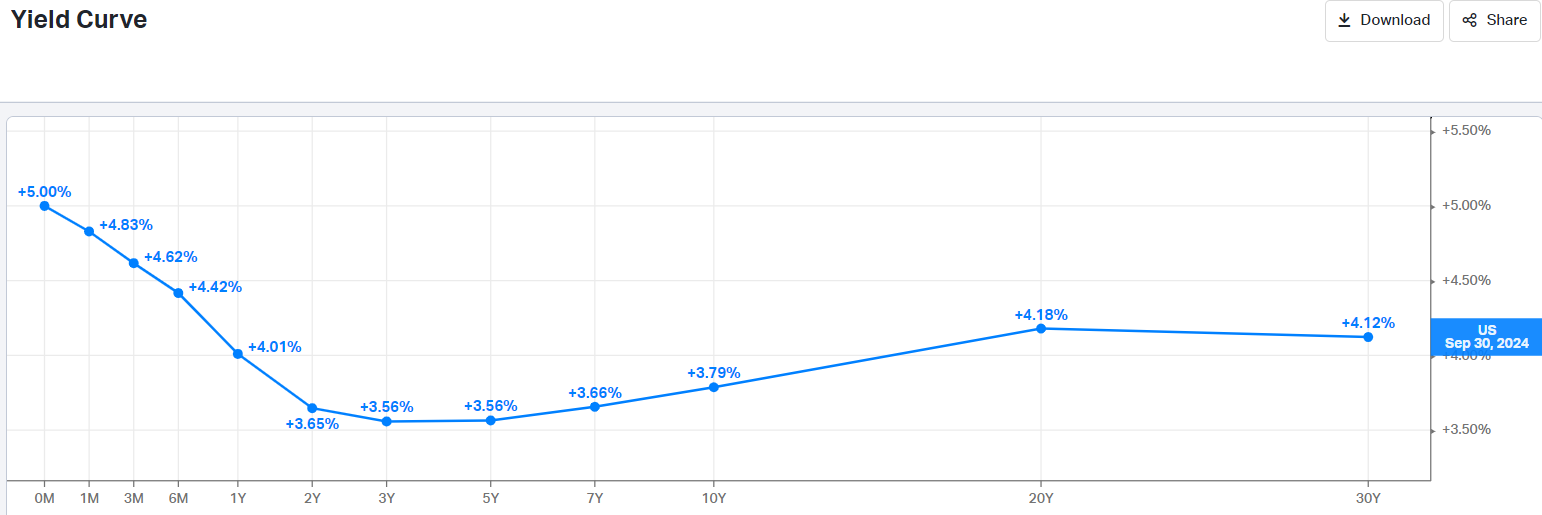

Many in the market are nervous. FRB lowered rates 75bp, and usually when this happens all other rates fall. However the 10yr yield instead rose 75bp. Should we be concerned?

Maybe so if it continues, but for now it helps the banks. New 5 year bond or CRE loan issuance picks up an extra 1% vs 3Q, and the cost to fund these has fallen 0.75%. A guesstimate is that this free 1.75% for a portion of the balance sheet, if sustained, could drive 2026 ROE for a typical bank from 12% to closer to 15%, so keep watch…

Below is the curve from Dec 27:

and below from Sept 30:

Peoples of Biloxi (PFBX) has gotten more interesting.

This bank has undergone a fascinating turn. For decades Peoples struggled under poor credit and market share losses, run as a family bank but owned by the public. PFBX was a near-lock to underperform the market, and did for decades.

In November 2020 this changed. Activist investor Joe Stilwell announced an 8.9% ownership and the intention to “maximize shareholder value”.

Activism is hard as is, but activism against a bank where the CEO is set on independence and family control is a step harder. However Stillwell has been persistent.

Since his first filing he has run 4 proxy contests, sued all directors personally for a total of $50 million, filed an additional court complaint against the company for books and records, shut down a director enrichment scheme, filed 20 13D amendments including 7 pages of exhibits of companies Stillwell has driven to sale, built holdings to 13.7%, and gotten approval to get to 19.9% ownership.

Meanwhile Peoples has begun a series of measures to try to improve performance. Management has instituted a share buyback, special dividend, recaptured a tax asset and run rate close to 1% ROA and 15% ROE the last three quarters. The 70% efficiency ratio and 30% loans / deposits remain a problem, as does the point of the lawsuit - the CEO’s son buying bonds at the top of the market to generate a $50mln unrealized loss.

With the tax asset recapture PFBX is today at 95% of tangible book and Stilwell and Swetman seem to still be competing for shares (book value could fall in 4Q due to bond marks).

Swetman is 75 and is holding out to hand the bank to his son Tanner. I’m told that Stilwell, an attorney, is confident that the opposition is tiring and victory is near. As long as both sides are jockeying for shares below book, Stilwell is involved, and the board fatigues, longs may find time is on their side.

Why isn’t CFBK performing?

It’s time we look at a recent writeup of CF Bancorp (CFBK). I would be glad to dwell here on some ways 5 Points has helped readers - posts about VBNK before a 20% drop, supportive GGAL before a 20% move, ESQ 25%+, CCB 40% etc., but whenever I highlight positives and the shares fall or things change, as at CFBK, it’s important to re-examine.

I suggested CFBK was a merger target, and would go into the Russell. Shortly afterward the CEO sold shares and the stock is off over 10%, no better than the sector.

What’s the problem?

- On the Russell, CFBK recently screened above the likely cutoff. I’m told insider ownership has kept it off some published lists of banks to enter the index. One source suggests this will be cleaned up and CFBK will be considered an “add” in the coming months, but this will need follow up.

- On the sale of the company, I have heard the company has tested the waters, but wanted a higher price. Part of my thesis is that the Trump administration is a new paradigm and bids can improve.

As much as anything, this is a question of, do we have confidence in private equity owner Castle Creek to help maximize value, or will they distribute shares to partners? Castle Creek has done excellent work with Fund 6, and has not made any mention of changes in their investment so we will track quarterly filings; distributing shares would be a surprising and unfortunate outcome in Fund 7.

Where does this leave us? Patience can be rewarding in M&A investing, but a CEO sale at CFBK tells us we may need to be patient indeed, even if it is just 10% of his holdings.

If putting together a merger target basket, CFBK still carries a number of the right characteristics. Depending on entry price we might elevate other contenders such as prior 5 Points-featured banks like Blue Ridge (BRBS) and First Foundation (FFWM) relative to CFBK. We suggested the board at First Foundation would push for a sale behind COO Lagomarsino, and sure enough the CEO has stepped aside to clear the way. Yes, he also sold shares, but on the way out and announced at materially higher levels.

Blue Ridge CEO Beale supports the agenda of the gold standard of aligned sponsors - major shareholder Ken Lehman.

On to the notes:

1) If you like making money you will love Mike Bell’s message.

Mike Bell is an attorney representing credit unions that want to buy banks. He presented for 45 minutes on Dec 11 at an online bank conference and almost everything he said was of value.

In place of a block of text to summarize impressions of his key points, let’s use a meme: (note - dollar amounts are buyer and seller asset sizes)

This credit union emergence remains overlooked, lightly understood, and exploitable.

The logical next steps after listening to Mr. Bell are to:

Build the target basket, casting a wider net for potential merger targets among public banks, including New Jersey and Pennsylvania.

Enjoy as more buyers come to market. Mr Bell has 150 clients, most of whom have not bought anything, but want to. As they “open” new states with initial acquisitions, the ball will increasingly get rolling and bring pressure to other banks to sell.

Don’t assume this lasts for years. Credit unions pay no taxes so are in a sense gaming the system. Perhaps in 5 years we will look back at the high-premium sellers in 2025-2026 as the lucky winners. If certain managements are dug in independent and you don’t plan to be activist, it may be best to leave them alone. The others, we want to partner with.

Future editions of 5 Points will have more to share on possible targets, but we have recently covered SFBC and TCBC as two companies that could work with Mr. Bell. First Northwest (FNWB) is another on the larger end that readers should track.

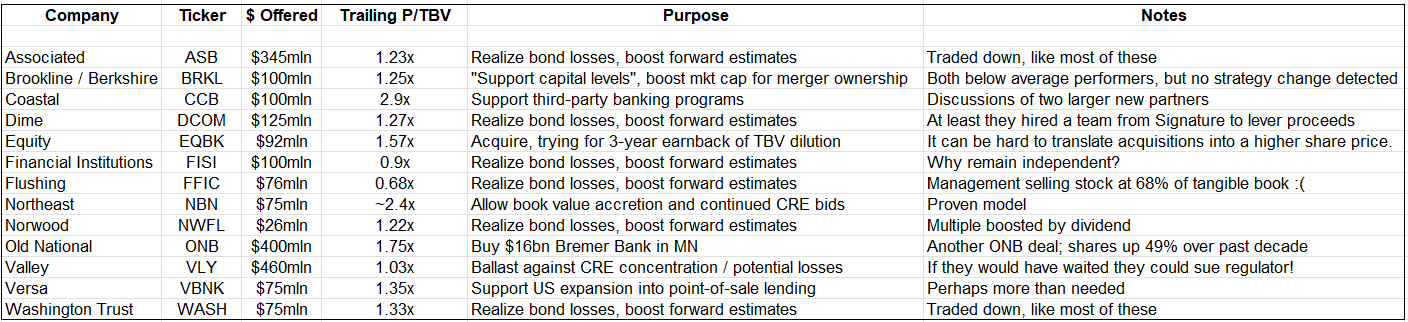

2) Several banks sold shares in early December. Who did it best?

Let’s meet the contestants:

Ideally, a bank raises money to pursue an elevated ROI business line. VBNK, CCB, and NBN among others seem to be pursuing such opportunities. Most others were to fill the hole from selling 1.5% yielding bonds and reinvesting at 5% to boost forward estimates.

Sure enough, the CCB offering was well-received, and shares have since traded up 15%. The others have not made much profit for buyers at this time.

Does it make sense to realize bond losses? Let’s use FISI as an example, considering:

The tangible book value test. FISI sold shares at about 90% of tangible book value. With the exception of recapitalizing to save a bank, selling shares below tangible book almost never makes sense for long-term shareholders.

But is the book value dilution made up from increased earnings?

Earnings accretion shown below is 7 cents vs. $0.71 book value dilution, or ten years worth, which is a long time to earn back losses. In meantime the company’s $3bn AUM and 2.7% deposit cost franchise are diluted by about 1/5.

FISI posts another slide suggesting they will use their new 8% capital ratio to expand in markets as far south as Baltimore. This would be more appealing if the bank had identified a differentiated model or team, such as from Signature bank. 10 years ago, FISI traded at $25 - right where the offering was done, and shareholders may be concerned the past is prologue.

In addition, why make bond bets in the first place? Most of these banks get a scarlet BS, for “Bond Speculation”, and it’s unclear they are out of that game.

But what about a raise like Associated in which the bank sells shares at a premium to book and also boosts EPS (from $0.56 run rate to $0.59 run rate)?

It depends on how much good franchise value Associated gives away. I can’t blame management as much in these cases, which become a gift to new shareholders at the expense of the old, but again typically if management can come up with something better to do than just go buy replacement bonds for the ones that burned them. ASB currently trades below its offer price, like Dime and many others above.

Outside of a few therefore I suggest the best “offerings” could be those that went undone - from Community Bank System (CBU) and First Financial in Texas (FFIN), two banks with underwater bonds but high multiples that did not sell a share. These banks are focused on growing their relationship and fee businesses rather than diluting good parts of the franchise in order to get a do over on a low-value part of the company. They will sell bonds as needed to fund quality loan growth and push for neutral rate management.

Keep an eye on our shelf filers too, who might have wanted to sell stock but have not (yet): Metropolitan (MCB), First Community (FCCO), Guaranty (GNTY), Burke and Herbert (BHRB).