February: GBFH, FFBB, and Bill Black on Pacwest / BANC

The WestAmerica trap; Why didn't the AFBI deal work?; The GBank (GBFH) story; FFBB detail; Bank OZK has been misunderstood for decades; Bill Black on how PACW survived

Good morning,

Current mood:

In this note:

1) Most bank investors fall for the “Westamerica Trap”. WABC rose 1000% from 1988 to 2004, but has been flat ever since. We look at other similar high-performing “bank bonds” you may want to avoid.

2) Credit Union buyers, and how the AFBI deal fell apart - new lessons on how to evaluate credit union deals (and buyers).

3) The story behind the selloff in FFB Bancorp (FFBB), and what’s next.

4) What’s the hype at G Bank (GBFH) about? (Note, because GBFH is about to report and for length purposes 5 Points will also profile GBFH’s technology in the March edition).

5) Zoom out at Bank OZK (OZK).

6) The Wild West: An untold story from the survival of PacWest, and other fascinating thoughts from an interview with Bill Black, former financial sector fund manager and corporate development at each PacWest and Banc of California.

1) The “WestAmerica Trap” is common in bankland - how to avoid it.

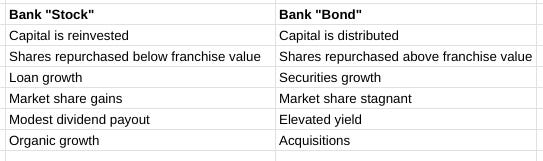

Highly profitable bank shares should rise over time, right? Yes, unless they turn into “bonds”.

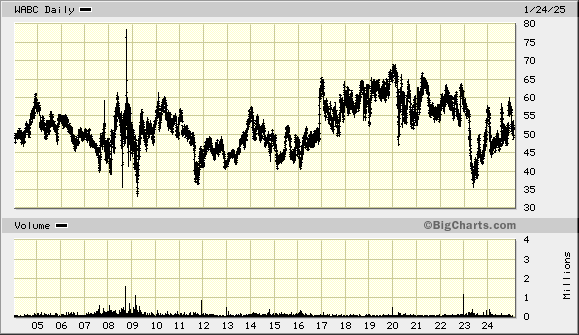

Below is a chart of WABC from 1988 through 2004, showing 1000% gains before dividends.

Below, a chart from 2004 to today, also before dividends, showing no gain for 20 years.

The same person, David Payne, has been in charge at Westamerica from 1988 through today. I only met him once, ironically around 2005, and at the time he was detailing how he would survive and everyone else would blow up. It was true! I can’t describe how he has changed, but I suspect he has kept the same mantra post GFC because his bank’s performance reflects it, increasingly acting like a bond.

The Westamerica Trap has some general characteristics, below. Most importantly, these companies switch focus from growing value per share to returning capital, and in the process capping the upside.

Incidentally, WABC made 2.1% ROA in 2004 and in 2024 it made…2.1% ROA.

But loans / deposit fell from 60% to 20% and capital grew from 6% to 13%. Payne has become more and more conservative with age.

There are scores of other banks like this though few are as dramatic. With most, an elevated ROE is offset by a spread-heavy bank not growing balance sheet but repurchasing stock at 1.5 - 2x tangible book, eliminating upside from intrinsic value growth. Butterfield (NTB) is one example of this, a beautiful, high ROE bank that pays a high dividend, repurchases stock at 1.8x tangible book, and waits for acquisitions.

Yet NTB with high fee income, cheap deposits, and good market share has gotten left by the market (albeit dividends would narrow the gap below).

From what I’ve written so far you might conclude that I’m just saying high dividend paying stocks don’t go up much, which is not a revelation. The full story has more steps, typically:

Company stops finding attractive growth outlets

Company returns capital

Returns may remain high, but tangible book value stops growing as capital is dividended or company repurchases stock well above book.

Multiple falls

So while a high dividend is a typical symptom of the Westamerica Trap, the real cause is that management cannot find anything attractive to invest in, so they default to dividends, unaccretive repurchases, and questionable acquisitions.

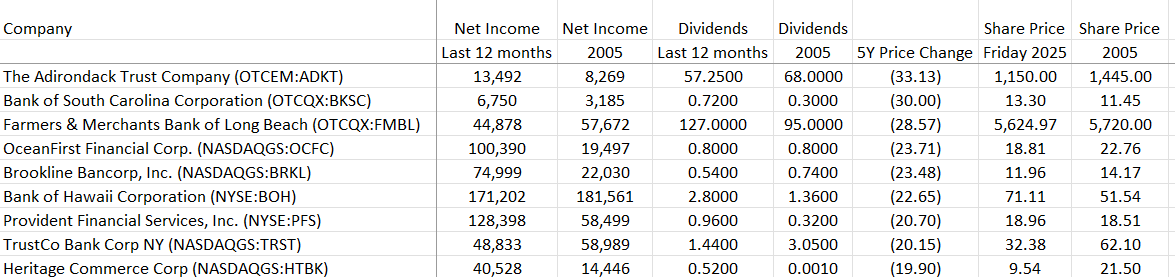

A quick screen of candidates finds a large number of banks in the “Trap”, with a few shown below. Yes, those OCFC, TRST and HTBK 2005 stock prices are correct.

2) AFBI, credit union deals, and finding the right acquirer

Last edition of 5 Points included a meme about Mike Bell of Honigman LLP, a lawyer who invented and then perfected the process for credit unions to acquire banks.

A few days later Affinity Bank (AFBI), a seller to Atlanta Postal credit union, saw its deal fall through and its share price decline 20%.

“Sam I thought you said we could make money positioning for credit union acquisitions”.

Yes you can, and true to Mr. Bell’s word there was a deal announced in California this past week, the first ever from a credit union in that state.

But CU transactions are different from what we are used to. When a bank buys a bank, we often know both sides because they are publicly traded. When a credit union buys a bank, we tend to just assume that it’s fine and we chuckle that it’s allowed but just figure it will close in a year.

The lesson here is there are smart, strong credit unions and there is the reverse.

In this light, some think the issue is related to Atlanta Postal spending tens of millions on a headquarters, blowing a hole in their income statement.

Indeed a look at APCU’s financials shows them making decent money in 2023, and then expenses ballooned and losses emerged.

Perhaps these folks should budget their expenditures in advance.

I respect management’s desire to spread out the cost of the large new headquarters with an acquisition, but this logic is a bit like “the marriage will work better if we have a child.” You have to fix a culture before you double down. The NCUA can’t be blamed for stopping Atlanta Postal in the name of safety and soundness.

So when you see a CU / bank acquisition announced, track the buyer’s financials. For those wondering, Global Credit Union, the buyer of FFNW in Seattle, is hanging on at 86% efficiency and 2% ROE in 3Q24

3) What Happened at FFB Bancorp (FFBB)?