February: Copper in the Financial Sector?

How AMBZ won, Hamilton Group's (HG) advantage, Old Glory Bank (DAAQ), LendingClub's (LC) earnings leap

Scams: Note that I’ll never send you a link asking you to “support my work”.

In this note:

A tribute to the growing Substack bank community

The 5 Points:

LendingClub’s (LC) epiphany

Hamilton Group (HG): No need for six sigma, two are fine.

How American Business Bank won in 2025, and who can win in 2026

The financial stock riding demand growth that may last our lifetimes.

Stay Woke to Old Glory Bank

Financial substack: We are in a bull market for no bullsh—.

Many of you know this already, but if looking for investment ideas and spending more time on X, the Wall Street Journal, or sellside research than Substack, consider allocating more time to Substack.

This is not to sell 5 Points, but emphasize that Substack is the only one of those entities with a feedback loop that directly rewards value. X and most media are selling attention; sellside research is selling a combination of estimate accuracy and the corporate relationship.

Further, Substack producers have to compete in a completely open marketplace. For example I followed the lead of Marc Rubinstein’s Net Interest. I can’t improve on Marc’s depth or quality of writing but fortunately we have a different focus! Jason Mikula recently explained how to launder a billion dollars on Tether and Simon Taylor is perhaps unmatched in Fintech, for enthusiasm at least. Column Bank’s Hegemoney is an excellent follow from a bank that moves billions of dollars cross border and sees firsthand how China actively seeks to replace the dollar.

Others have followed 5 Points and no doubt will surpass our little community in time, in sum or part include “The Bank Zhar”, Paul Davis’ Bank Slate, and the anons Victaurs and most recently Arkenstone among others.

In meantime I cannot slip by using AI or giving you messages like “Amerant is underwriting well” or “Comerica should disregard Holdco”. But so far so good; 5 Points subscribers are growing with growth of Substack, and hopefully you all are perceptive:

As always I continue to simply ask for your corrections, feedback, and nuanced insights.

On to the points:

1) LendingClub’s (LC) epiphany

Why earn 12% ROE when you can adopt SOFI’s accounting and make it 20%?

There are a small number of banks adopting fair-value accounting in place of reserve accounting.

To clarify, reserve accounting requires a 1-2% discount applied up front, so that if you grow loans, you suppress income. In contrast, fair-value accounting seems to mean a 1-3% markup at Lending Club, 4-6% at SOFI, and whatever the CEO feels is right at Newtek.

Reserve accounting is the global standard because it’s sustainable. In contrast, managements that hop onto fair value are incented to outrun the amortization of the loan premium, unless they sell the loans upfront. Sometimes that’s economic but other times the bank opts to hold the loan.

All of these banks are therefore holding billions on loans on balance sheet. Their amortization means that if they want to grow earnings, they need to continue originating more and more over time until credit cycles and there is a credit issue.

In contrast, traditional banks grow EPS as they slow loan growth all else equal.

So there are not many fair value lenders around, and the ones that exist are fairly new (or are BDCs with termed debt or private credit with lockups)

But SOFI has not yet endured a sustained consumer credit cycle, so what’s the problem? Apparently there isn’t one:

Like Eve in the garden, Lending Club sees the fruit on the tree and wants a taste. They are going fully to fair value as of Jan 1.

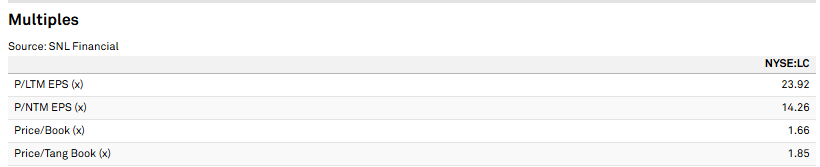

LC is not in as many businesses as SOFI but the company has a much lower multiple.

One advantage Lending Club enjoys vs SOFI is expense culture. As an example, LC CEO Sanborn gets $8mln while SOFI CEO Noto takes $24mln. $6-$8mln is de rigeur in the SOFI C Suite, including for the General Counsel and Chief Risk Officer among a list of other executives.

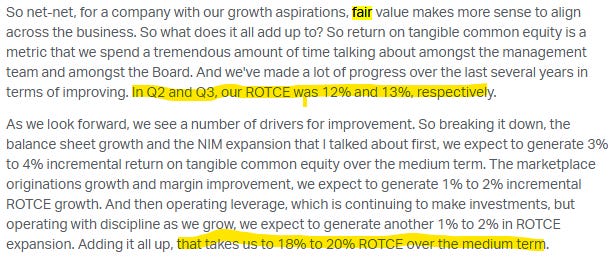

Marking up billions in loans at LC without a technology company comp scheme can therefore drive high ROE. Management outlined it in their November investor day:

It’s not clear that analysts have digested this transition, because the Street has 2026 ROE at only 12.5% per S&P.

What happens when a company blows past estimates because they start marking loans up?

Do the analysts say “We disagree with management’s aggressive accounting” or “We increase the discount rate and lower target price in our DCF”? No - I’m not aware of any Mike Mayo style analysts covering LC.

Remember these analysts also cover SOFI and they want the same good relationship with LC.

Lending Club also doesn’t seem to want that message. They say the fair value “helps a little bit” and it “evens out in the end”.

Perhaps analysts will boost their estimates and applaud “margin expansion and operating leverage”.

The quants, factor investors and stock screeners can fall inline and join the bidside. A few active managers can talk about the way things should be and sell, but market structure isn’t what it used to be and they may be outnumbered.

2) Hamilton Group (HG): The third time a charm?

An investing “hack” is to take the float from an insurance company, and marry it with a premier hedge fund. Then, combine market-beating returns with float and underwriting profit and boost compounding as you lap Warren Buffet with his own model!

Unfortunately this idea usually fails.

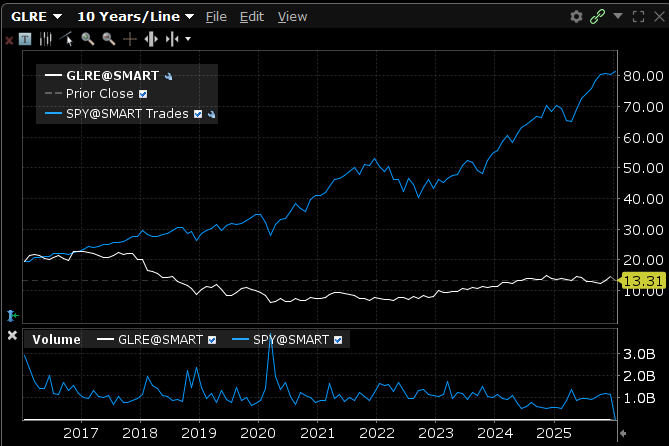

Here’s how it worked at Greenlight Re, the white line:

Third Point tried it but basically merged away in 2021. The combined entity, with a different name by 2021, gave notice to fully redeem almost all of its interests in any Third Point fund by March of this year, completing the separation.

These Warren Buffett wannabes wither for a few reasons:

Regulation. You can’t appear with a typical long/short hedge fund allocation as collateral for policy holders and get sign off. Regulators prefer duration-matched high-quality bonds to a Netflix bet into the quarter.

Buffett staked his Coke, Amex, Sees Candy etc. alongside the insurer’s own balance sheet in order to generate the synergy of a AAA rating. Plus, he built it over decades and generated trust with a long-term focus message.

Are you an insurer, or a hedge fund manager? If you are a hedge fund manager looking for an insurance vehicle to grow assets, what kind of policies can you write that will match appropriate risk and duration? Are those the most attractive markets at any given time? Maybe not. Policy risk / reward drives the business, not the investments.

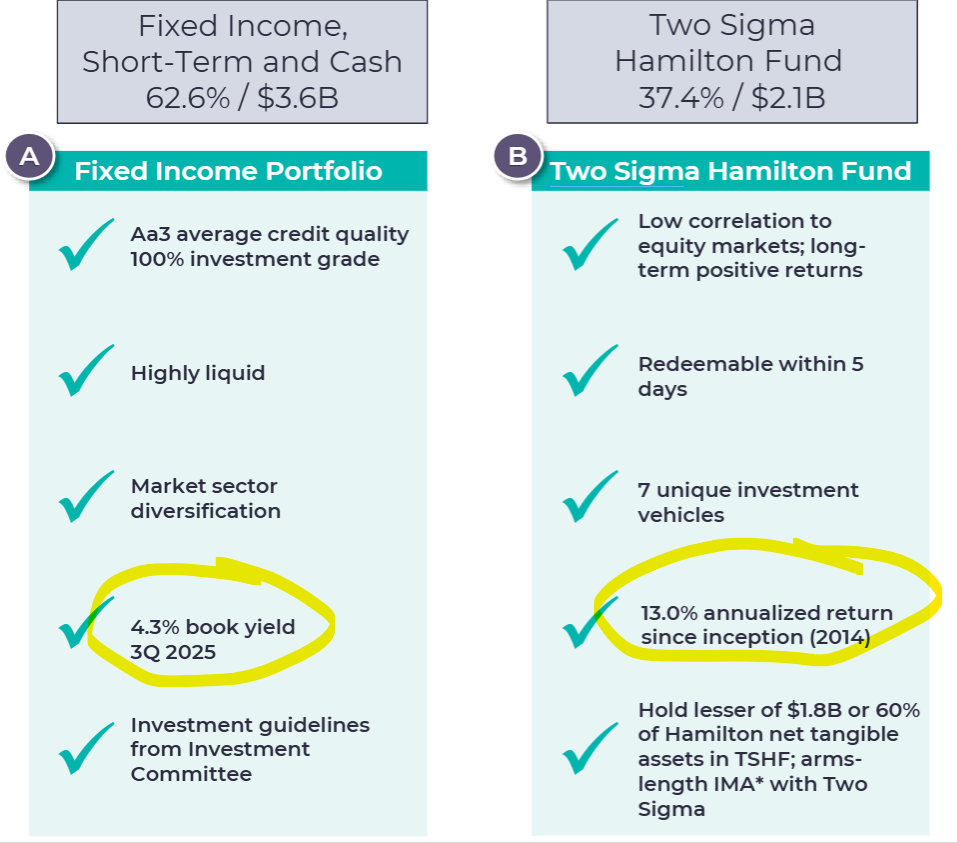

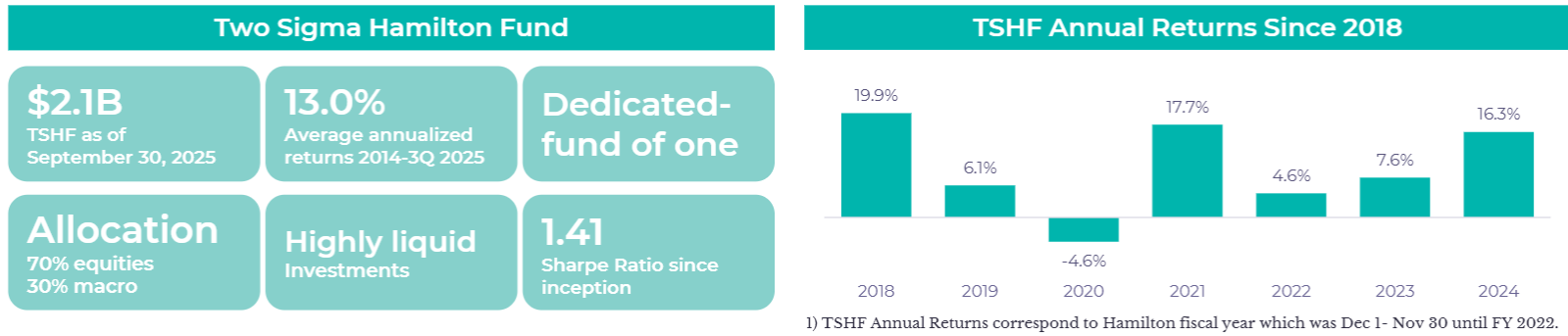

Then along comes property insurer Hamilton Group (HG) with $2bn invested with Two Sigma, a $70bn derivative of DE Shaw with its 250 PHDs and 1000 data scientists. People ask why I like to stay in microcaps - Two Sigma is part of the answer. The name comes from the combination of upper and lower case greek letters for Sigma, which in mathematical notation refer to the Sum and standard deviation. Their message is that when focused on volatility, they can size bets better and maximize returns.

That’s the rub - volatility management. If you can convince your regulator that your investments are structured around managing volatility, and are liquid, then you get to have your cake and eat it too in a way Third Point and Greenlight were not able to.

This is how Hamilton frames it:

In the table below, it’s helpful that Two Sigma’s returns are generally positive but otherwise almost random.

But more important may be “Dedicated Fund of One”. This means Hamilton can pull from Two Sigma’s alpha while suppressing vol in accordance with its risk and regulatory requirements.

I believe this qualifies as an advantage for Hamilton as long as they sustain their Two Sigma relationship.

Hamilton mixes property, casualty and specialty across several countries to generate a reasonable combined ratio averaging in the mid/ high 90s over the past 5 years, but between Two Sigma and a hefty repurchase that has retired 7mln of the company’s 109mln shares beginning 2024, any dip below tangible book value should be an opportunity.