February: Bank investing and the election

Branch light banks - how CUBI manages it vs others, the wisdom of buying agencies, BAFN's BOLT program, The issue at OTCM

Good morning,

In this note:

Handicapping how the future president could affect banks.

Branch light banks: The increased challenge of execution leads to pronounced successes and failures. Investors will find opportunities ahead.

Mortgage-backed securities were toxic from 2020 - 2022 but are now a reasonable choice for bank CIOs.

Bayfirst’s (BAFN) lucrative BOLT loan program

Everyone loves OTC Markets (OTCM). Why doesn’t the stock appreciate?

Brief notes:

I’m just returning from seeing 16 banks at a well-managed Janney conference. The theme of the conference was banks investing in treasury management software to take deposits from larger banks. It was not credit migration, because there still rather little in small-bank land.

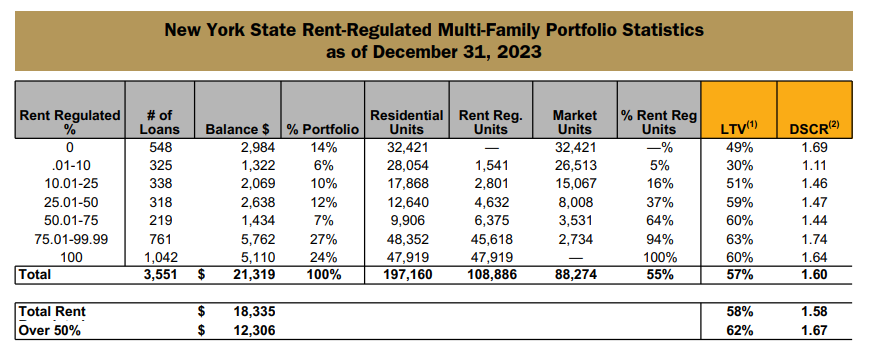

If you still want another view on New York Community (NYCB), On Jan 30 I thought the company’s biggest issue was large CRE loans, primarily rent stabilized, and on Jan 31 I thought the same, with a few updates:

a) We have a lot more data from the presentation on the rent stabilized loans, below. It turns out the issue is really about $10bn rather than the $5.1bn they disclosed prior, because another $5bn is 90%+ stabilized. Barring material rate cuts these loans are the long-term elephant in the room.

b) The company flushed a few quarters worth of earnings to build reserves, capital and liquidity to start addressing imbalances needing fixing since the early days of prior CEO Ficalora. Bank investors have gotten lulled a bit by this situation because for 15 years shorts were busted through acquisitions that masked issues. A new sheriff is in town and that’s no longer possible. In this sense, NYCB is in better shape today than it was in the beginning of the week.

c) Trading $100bn banks is not Colarion’s specialty, and buyer may need to be patient given NYCB will earn relatively little this year, but 55% of tangible seems to price in an ample amount of hate if you believe short rates will fall at least 1% this year, mitigating potential losses on rent-stabilized loans.

d) I have yet to learn how NYCB is systemic, and believe that venture deposits are 10x more radioactive in times of stress than general deposits. NYCB is not in that business.

1. What changes would a GOP President bring to the banking system?

Most of us figure we know the answer, but let’s look at the details…

A theme of small bank investing is to understand how government will waste our money through bank channels, and get in front of that. For example Kamala Harris thought her 0-2% preferred “Emergency Capital Injection Program” (ECIP) would create loans for Harlem movie theatres but it ended up going into 4-5% AA munis and then into my clients’ pockets through ripping performance of ECIP banks.

We look below at how things might change after November. While Nikki Haley may yet win the GOP nomination, for now I’m going to focus on the two 80 year-old stroke-risk candidates in the lead.

To keep this short, recall that Trump:

a) Invited bank CEOs to the White House to consider ways to boost the economy during covid, sitting next to Moynihan while complimenting the executives, and…

b) Would love some more banks to work with! Trump now banks with Axos, a bank willing to structure loans at a material spread for borrowers outside the mainstream. Kushner had a wide list of lenders he worked with, perhaps now streamlined given he focuses on some beleaguered asset classes and several partners are no longer in business.

Biden on the other hand generally sees banks as contrary to his voter base and outsources fixing that to his party leaders, on each overdraft fees and yet higher capital requirements that today cannot seem to find broad support.

With that said, below are some scenarios we might expect on a case-by-case basis:

Mergers, merger arbs (FFNW, HMST etc):

Biden: Approval with 6+ month delays, upon appropriate assurances of community involvement. This means that for larger banks, a merger can indirectly cost billions in redistributed loans or grants, with NYCB pledging $28bn to lower income communities and TD at one point committing $50 billion, and still not getting their merger.

Trump: I noticed no merger approval issues or delays under Trump. Merger spreads should tighten if he wins.

Separately, it’s possible that Trump might notice and curtail credit union acquisitions of banks, given they directly siphon badly needed corporate tax revenues.

CFPB, FDIC politicization and fees

Biden: Continuation of attack on fees, such as the $3-$8 overdraft proposal that will simply result in no more free checking accounts under $10,000 balance across the system.

Trump: FDIC activist Rohit Chopra may become a non-factor.

Puerto Rico

Puerto Rico is the recipient of around $50bn of aid across 3 Federal programs.

Trump has said “I have to say in a nice way in a very respectful way, I’m the best thing to ever happen to Puerto Rico. Not even close.” and also called it “One of the most corrupt places on earth”.

Under his administration we might expect tighter purse strings for the island to the degree it is allowed through FEMA grants or related programs.

However he would likely support tax incentives for drug manufacturing. He would like also leave open the 4% tax loophole for professionals moving businesses to Puerto Rico.

Biden has so far sped up disbursement of grants, and has left tax loopholes alone, but may be likelier to close them down the road than would Trump.

Capital rules

I could write 20 pages on this but the short answer is Dimon’s annual report list of grievances should shorten materially under Trump.

We can’t overlook the former president’s 2018 conference: As a candidate I made a promise to rescue the community banks from Dodd Frank - the disaster of Dodd Frank - and today we are keeping that commitment.

Minority banks:

Trump left them alone. Biden gave them the ECIP mentioned above. Future programs under Biden might depend on the winds of DEI, but Trump likely again leaves them to the corporate sector to support.

Of note there are several large corporations who have pledged millions to funds committed to investing in minority depository institutions and community development financial institutions, a reminder that not every issue has to be solved by the federal government.

2. Banking is fundamentally changing around how to grow without branches. Some branch-light leaders have managed it better than others.

This forces investors to dig deeper because execution risk is elevated, creating opportunities. A look at MVBF, MCB and CUBI