Coastal's Moonshot

5 Points’ schedule change, Loan growth, the liberal bank teaches the conservative bank, Florida insurerance,

Good morning,

Important change to a monthly schedule Due to my own bandwidth issues from running an SEC-registered advisor, 5 Points is switching to a monthly schedule. While this will mean fewer notes it should improve note quality, and readers will still get 60 “points” a year. I will continue to publish short notes as appropriate during important developments. I am giving some thought to lowering the subscription price although believe readers’ “return on subscription” is currently attractive.

On to the note,

Loan growth is hard to find, which means it may increasingly be valued in 2025. We parse where to find it.

Florida insurers: A lumpy 20%+? How American Coastal is different.

Union Yes! (?) The liberal bank (AMAL) teaches the conservative bank (CBNA) a lesson in capitalism.

Coastal’s (CCB) moonshot - closed loop payments.

Printing money around the globe: What does Citi’s crown jewel do? How others might be able to begin competing.

1) Loan growth and where to find it

In bank investing, the informal rule is that whatever is scarce is highly valued. A year ago bank investors were focused on deposit costs. Today loan growth is difficult to find.

For example our largest banks’ loan balances cannot even keep up with GDP, as borrowers are siphoned away to private credit and capital markets:

So, it’s reasonable to expect the market to begin rewarding loan growth into 2025.

Below is a screen for where it exists, first inside the banking system and then outside.

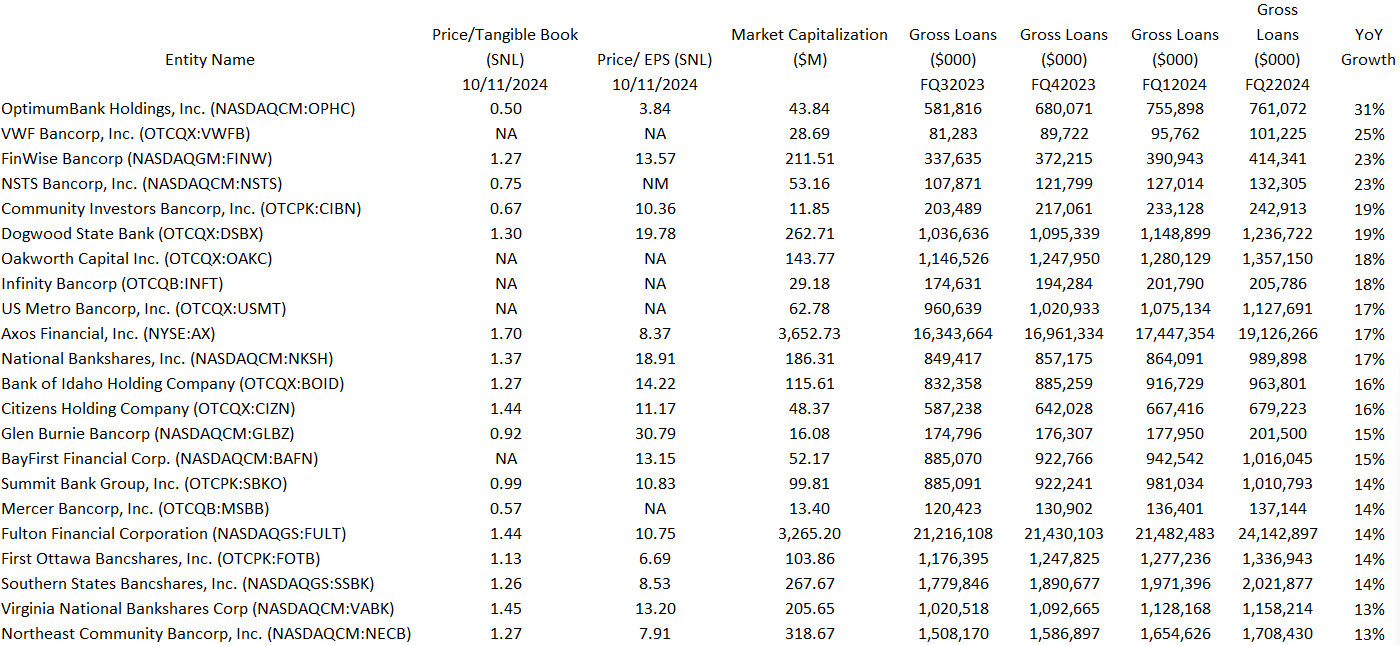

Among banks:

Some notes on the banks in this screen

OptimumBank (OPHC) seems interesting; 50% of book for 31% loan growth, and net income has approximately doubled over the past six quarters. Optimum is making great progress. This looks like an awesome value. What’s the catch? There are two.

1) Much of the growth is CD funded, and 2) The bank is paying CompassPoint to sell stock into the market at around $4.75. There are convertible preferreds in place that ultimately dilute book value down from the $9.00 range to closer to $4.50 per management but the company’s growth has come at a cost to tangible book and EPS. It’s also not clear they are provisioning sufficiently for loan growth.

VWFB, NSTS, MSBB and NECB are mutual conversions that have, to some degree, pushed loans on balance sheet in order to lever excess raised capital.

BAFN and FINW get loans from wholesale channels. FINW is actually doing some clever things to improve the quality of their loan pipeline and rely less on places like Upstart. Axos generates volume largely from online channels and an evolved network, with a record for thoughtfully onboarding loans when terms are favorable. BAFN has an excellent opportunity with small dollar SBA but it’s not clear they can properly take advantage.

Oakworth (OAKC) is historically a wealth bank but has, with mixed success, pursued larger CRE deals in and around its footprint.

CIBN is inefficient.

GLBZ has been un-investable for years but the newest new CEO is at least trying. Yet the efficiency ratio is 93% for the trailing year, which outside investors should not accept.

Infinity does not often trade but management has done some interesting things worth discussing in a future note.

I’ll go into detail about how to parse the banks after a brief look at…

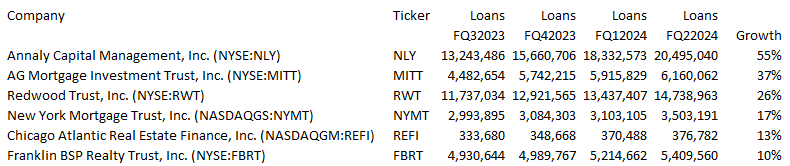

…Nonbanks

including BDCs:

You notice the growth profiles above are more aggressive. I won’t go down the list, reiterate points made in prior notes. Specifically: a) the talent and money are headed to private credit, and b) banks who cannot engage in a similar style of lending (not necessarily 6x EBITDA unitranche but at least fast execution on unusual structures), through partnerships or holdco subsidiaries, are ultimately leaving money on the table.

I was glad to see JPM CEO Dimon agree with me in his 3Q call.

Finally, mortgage REITs remind us that you can typical lever the humble agency mortgage to make a double digit return without a branch network.

Now let’s set that screen aside. The best growth banks are the ones with the best growth verticals, including built-in sources of referrals. This list includes:

Compliant BaaS banks like CCB, TBBK or FINW, and

Banks with unique loan acquisition verticals like NBN, NEWT, and VBNK among others.

These banks are not slave to client cycles. Look for this type of company.

2) Florida insurers and the potential for a lumpy 20%+; an introduction to American Coastal (ACIC)

It’s become fashionable to second guess Buffett so let’s try. A lumpy 15% and a smooth 12% can be about the same due to math:

What you should want is something closer to a lumpy 20%.