August: The Trade Created from Rotation into Banks

Banks are not necessarily "overbought". A look at Bayfirst's (BAFN) incentives for independence. Does FFBB have further to go? Farmers and Merchants (FMBL) tries to pick up the ball.

Good morning,

In this note:

The strong rally in banks vs the broader market has created an opportunity.

Are banks still “under-owned”?

Another look at Bayfirst (BAFN), which is trading below tangible book value in credit-union acquisition friendly state. But greed doesn’t always work in our favor.

A FFB Bancorp (FFBB) update

A look at Farmers and Merchants of Long Beach (FMBL), which is repurchasing shares at 46% of tangible book.

1) The rally in banks vs the broader market has created an opportunity.

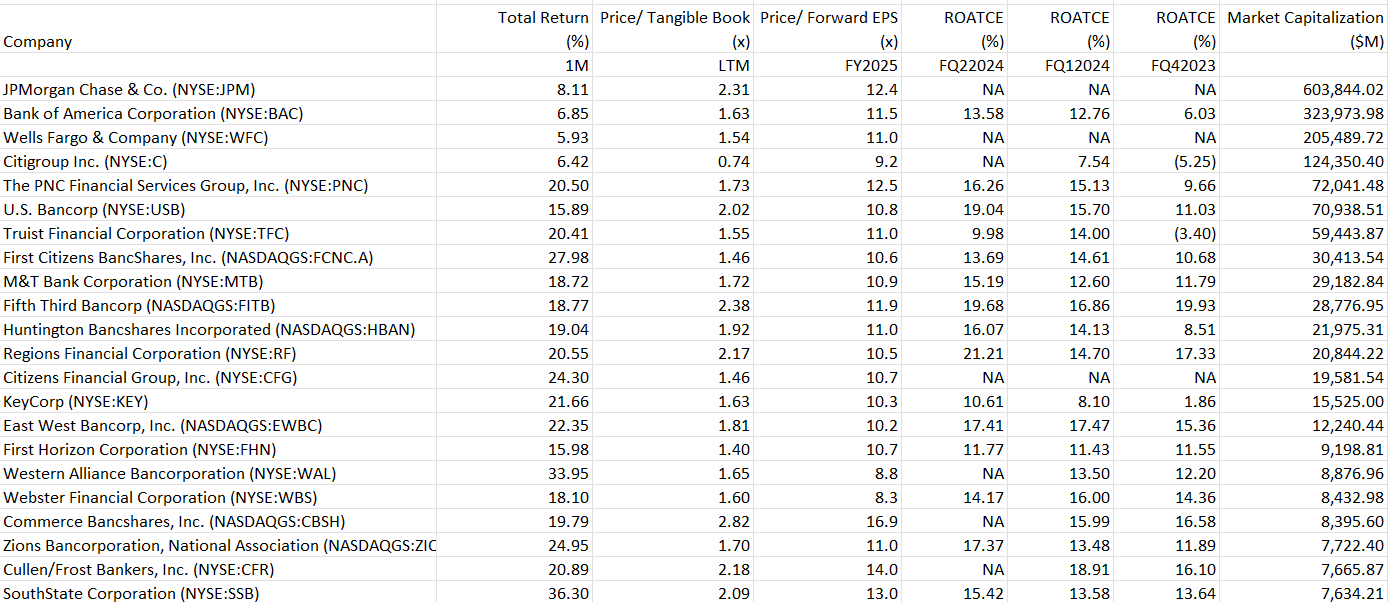

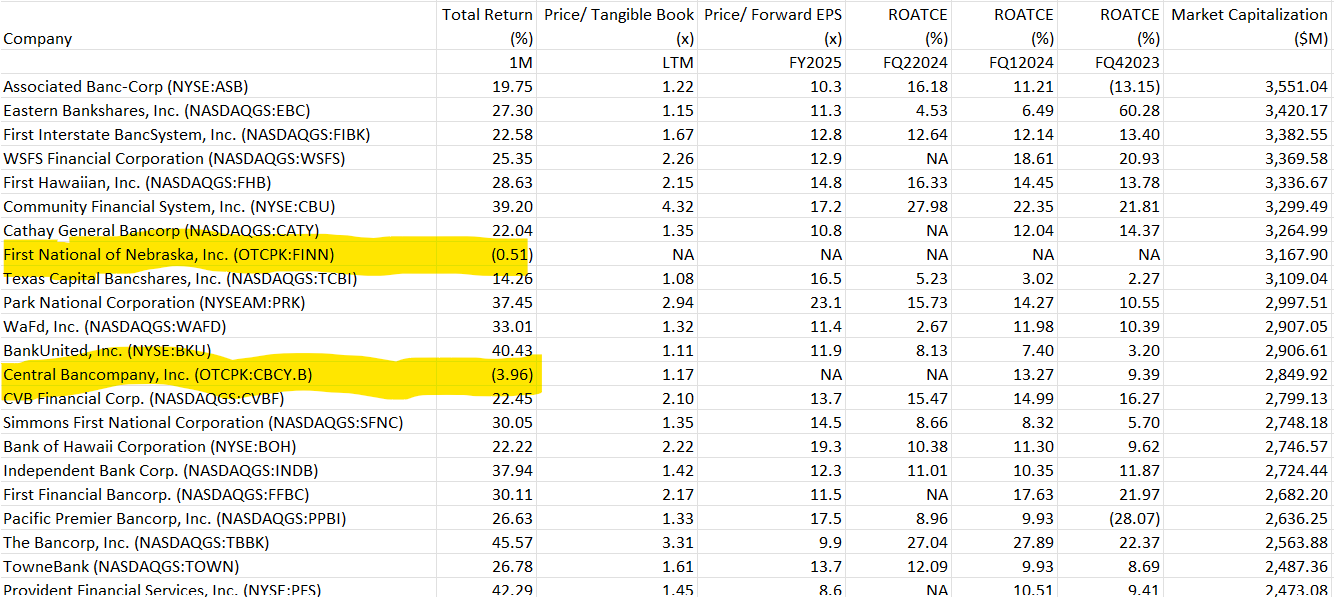

What do you notice below?

Looking again, I would suggest the numbers in yellow:

This is the reverse of what 5 Points discussed in the prior edition. A month ago, the top 4 largest banks has outperformed the S&P, and smaller regionals were mostly flat for the first half of 2024.

Over the last month however, the largest 4 - right at the $100bn market cap line - are all up about the same 6-7%, and the smaller are all up 20%+. It’s as if there were no difference between JP Morgan and Bank of America, and all that matters is their size.

Meanwhile if the sub $100bn market cap bank had a good earnings report maybe it is up 24%. A bad earnings report, up 18%, but again this is all a function of market cap. Even Comerica, which had a terrible report, is up 11%.

Going a bit further down market cap, do you notice other anomalies?

I notice two banks, and only two above the banks over $2bn market cap, whose sin was to be listed on bulletin board and not Nasdaq, so their shares broke the 20% upside pattern and actually fell. 100% batting average on being outside of the Nasdaq and having shares decline among this market cap subgroup.

The setup from here. Sometimes the market offers a wide door to walk through. Our clients own a number of Nasdaq banks and a number of OTC banks. You can imagine where capital is getting allocated among this rally.

The broader market has no idea what to do with banks, so when narratives change they play the entire sector through the ETF button. Inefficiencies gap out - this is one of those times.

I could almost guarantee that FINN would be up 20% since July 1 if it traded on Nasdaq, but it doesn’t so it is down.

I’m not here to tell you what names to buy (I do respect the person who runs FINN), but I am telling you that this Nasdaq / OTC arbitrage opening is an easier hurdle to jump over than is trying to parse among all the Nasdaq names.

2) But are banks “over-owned”?

I don’t think so.

We have established that chasing listed banks is perhaps not the best value in the sector, but does that mean banks are about to sink back to June levels? Eyeballing the chart in point 1) above of banks vs the S&P 500 suggests they are “overbought”, meaning relative strength is stretched by various measures.

One good datapoint says no. Pardon the strange look of the short interest chart below, but focus on the green line and the “80” and “0” at right.

It is a chart of the KRE (S&P Regional Bank ETF) and the green line is short interest as a percent of float. Notice that before Silicon Valley, that short interest was about 27% of the KRE, meaning more people wanted to own it vs short it.

More recently it has only fallen from 78% from 91% at the beginning of July. In other words, almost nobody wants to own KRE still; it is almost exclusively used to sell short.

But what does it mean to be “under-owned”. Let’s compare KRE, which as of last week had what Ortex reported as a 78% short interest above, to tech and large-cap dominated QQQ.

You can see below that QQQ short interest is about 7%.

In other words, Nasdaq / tech remain extremely popular by comparison.

Keep track of KRE short interest - when it drops below 50% then perhaps you can consider the sector slightly popular again.