April: With Banks, Private Equity are Our Friends

The coming BaaS oligopoly, mortgage insurance

In this note:

In banking, private equity is our friend

Bancorp (TBBK) is the target of a recent short report, which we look into.

2a. Is Merchants Bank (MBIN) like TBBK?

The similarities between Esquire Bank (ESQ) and Bancorp (TBBK)

Merger discounts at small banks.

Granite Point Mortgage Trust’s (GPMT) surprising disclosures.

Meet up: I will be in South Florida, New Orleans and Jacksonville in the weeks ahead and would be glad to meet a few readers; feel free to simply reply to this email.

The next $5k donation from 5 Points is going to Ronald McDonald House this month. RMH joins Children’s Hospital of Alabama and Embrace Alabama Kids as donees.

1. Private Equity are our friends

In US society, we have grown accustomed to seeing private equity take control of and wreck companies.

In banks, where private equity rarely takes more than 24.9% ownership, the story is different. Bank private equity investment usually begins a competition between management and the clock, to see if enough value can be created to justify independence.

There are two primary funds doing this, Patriot and Castle Creek. Their mandate is simple. They post the company logo on their website and beneath it either reads “realized” or “active”. Realized for smaller banks typically means the bank is sold, and active raises the obvious question of “when will this be realized?”

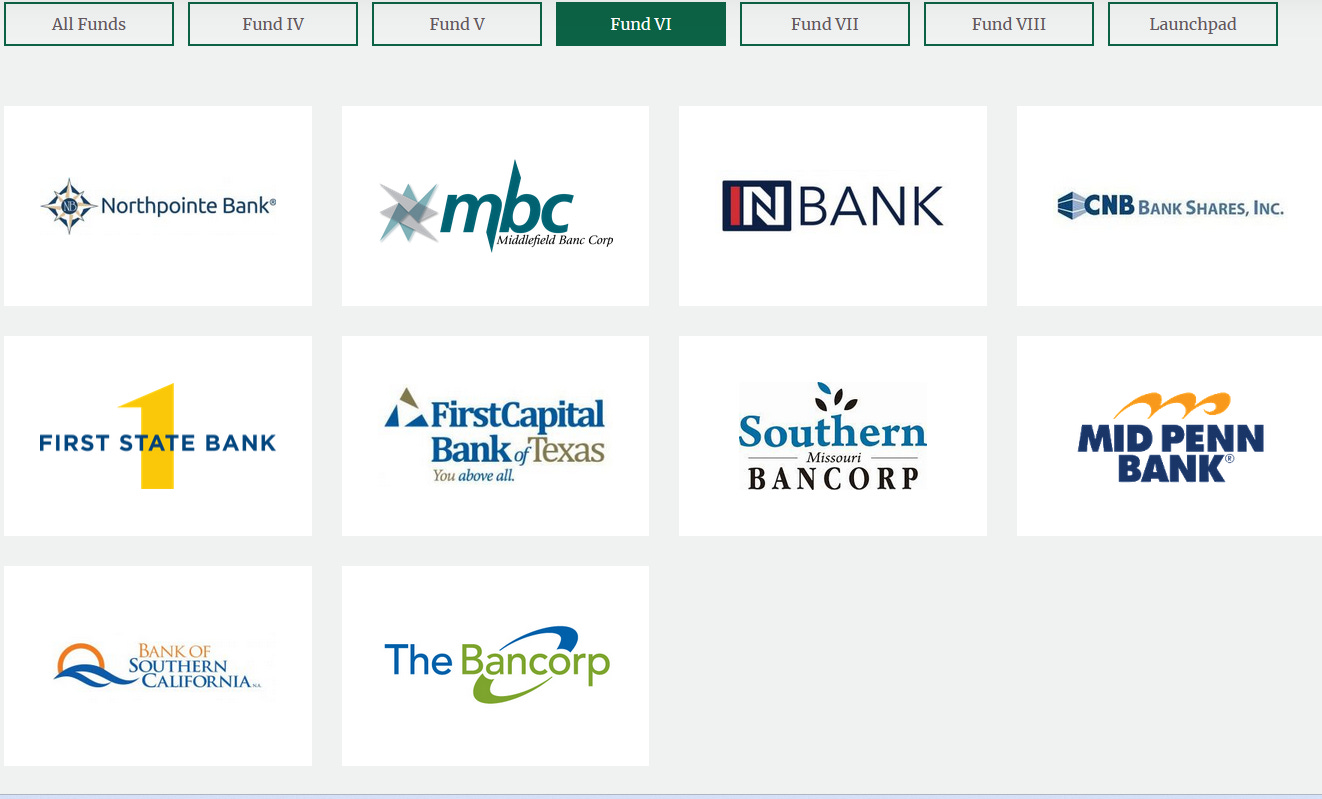

Let’s look at the example of Castle Creek Partners Fund 6 below. Fund 6 is approaching a period of harvesting.

First, below are the positions the fund has exited:

And below are the positions it still holds:

TBBK I discuss below. Bank of Southern California just entered a merger and the clock is on SMBC, MPB, MBCN, and NPBC among others. INBC’s elevated efficiency ratio may make it vulnerable to consolidation.

Patriot is the other fund and they have their work cut out for them in several positions but we will see how they do with a few that should be down the middle for acquirers, such as Freedom (FDVA), Metropolitan (MCB) or Primis (FRST).

Feel free to check ownership and fund dates from time to time to understand if a clock is running on your bank positions. The older the fund launch, the more likely the position becomes a target for exit liquidity.

2. Bancorp (TBBK):

New shortseller favorite Bancorp shares have sold off for understandable reasons, but mind the massive cash flow of the core business.

You have read a bit about potential credit issues at TBBK here in the December post and more recently in mid March after the 2023 10K. Today the market has not only come to realize the issue, but we see in the chart below the messy process of TBBK ownership flipping from growth investors to value:

A short report recently accelerated the decline. The point of this message is that a good time to let go of TBBK shares was when insiders and some Colarion clients among other clever people reduced stakes in the $40s on the real estate risk. Today off 30% and with the underlying business among the best in public markets, the short is not so compelling.

The issue: A recent report by a generalist research group on March 21 focused on several dodgy-looking apartment complexes that serve as collateral for TBBK loans, specifically the bridge portfolio shown below:

Let’s look at the report and the credit in the context of the overall earning power

The credit issue: The Culper Research short report observes that TBBK’s 0.47% reserve on bridge apartment loans (REBL) is too low. That is unquestionably true. These are loans to wannabe real estate moguls who buy decades-old apartments and spend on upgrades in the hopes of raising rent and getting leverage on their sale price. As rates rise and new supply comes online, their speculative equity withered.

TBBK typically lends about $7.2mln on a $10mln apartment acquisition. So how big are the losses?

Culper speaks to an underwriter who suspects the toll may be over 3% of TBBK’s $2bn bridge loan portfolio. I would lean a bit higher.

More alarmingly, Culper does math averaging across the portfolio that to sell these loans underwritten to a Fannie 1.25x debt-service yet nonetheless paying 12% interest rate yields losses of 35%. I don’t think that is how this will actually work.

Instead of 12%, I posit that most of these loans would price closer to 10yr+2-3%, i.e. 6-7%, and there’s no way TBBK would not finance a stronger third-party note buyer or foreclosure investor at a competitive rate unless they somehow infuriated their regulator into forcing a firesale. Further, Bancorp has had a number of paydowns in the portfolio of late and management has been transparent about this to several investors. I don’t align myself with anything close to this math.

The report spends the majority of its content otherwise poking fun at amateur apartment developers, profiling negative online reviews of complexes, and showing pictures of damaged units. I have some experience with “workforce housing” and would say that fires and disgruntled tenants can certainly happen.

Surprisingly, although management is still saying losses will be very limited, they are telling some investors they can manage properties themselves. This will likely all play out over an extended period. Yes, the days of clean credit at TBBK are over, but the point is the company can save itself tens if not hundreds of millions through a thoughtful workout process.

The losses will be born out through foregone interest, legal and workout costs, and a component of charge offs on loan sales to new operators. That is why the underwriter is saying 3%+.

Incidentally, 4% looks like this, which is one reasonable starting point. As the 2025 maturity wave approaches we will see how accurate this is:

$80 million is a bit over one quarter of TBBK pretax income. That’s the punchline.

Or, if TBBK were to write all that all off right now, tangible common equity would go from 10.4% of assets to 9.7%, but again you might not notice because it would be mostly earned back intra-quarter. 9.7% is well above the sector average for the sector.

Rate of share buyback is the ultimate victim in this exercise.

This takes us to…

…The core business: Culper’s report did not mention Bancorp’s payments business, but this is where the short is difficult. There is a reason why TBBK is targeting 4% ROA in its out years. That number is not a fantasy; TBBK’s competitor Sutton Bank is already there.

Sutton ROE:

The business is largely in issuing cards for fintechs and other third party issuers and collecting 0% deposits at about $50 per account. It is extremely compliance intensive. As a result, all of the banks below save Green Dot print money (Green Dot and Evolve have recently received compliance orders).

If you can get payments compliance right you own a goldmine. So far TBBK has been able to do so. These banks effectively compete against each other on catching launderers, as in “We caught the scheme and Green Dot (GDOT) did not” or “Metropolitan (MCB) left the business because they were behind on people, technology and investment, so their share transfers to one of the anointed.”

At TBBK, the returns looks like this:

Those are not TBBK ROA. Those are TBBK pretax ROAs for those years if we had added $30mln provision, that is, what TBBK would have recorded if they provisioned appropriately to offset potential 4%+ losses in the REBL book.

You can short this after a 30% drawdown if you want but I might prefer to go after companies that are not close to doubling up JP Morgan’s ROA.

TBBK’s market cap is now $1.6bn and the company generates $175 - $225 million of discretionary cash annually, depending on platform growth and what provisions will look like. Today the cash goes into buying back about 25k shares every day rather than supporting asset growth.

While Culper gets credit for calling out management on the reserves and underwriting, many longer-term investors will take interest in the value of the core business after probable losses are factored.

2a) What about Merchants Bank of Indiana (MBIN)? Are they like TBBK on the bridge side?

I have gotten this question from several people. Without doing a full profile of MBIN, I will offer a short rebuttal here. There are some similarities on paper; culturally they are different.

TBBK CEO Koslowski is an executive focused on payments and compliance, who affixed a real estate group onto his platform to generate earnings yield. Management of the bank and management of the real estate group are separate and TBBK is in any event looking to embedded finance to ultimately replace some or perhaps all of what REBL provides. Embedded finance is a far superior business to traditional commoditized bank lending (again, with compliance) because the partners typically provide credit support. This is a topic for another note.

At MBIN, Michael Petrie is the patriarch, and has been a mortgage and apartment finance professional since Ronald Reagan was president. Sponsors are key to him and he has no interest in funding the kind of syndicator projects that found their way into TBBK’s book.

MBIN will see nonperformers with higher rates and the typical capital spending challenges of bridge. However the bank’s underwriting culture is distinctly different. This includes the fact that they lend recourse (TBBK does not), who they work with, who does the appraisals, what area etc. This will differentiate its outcome relative to most REITs, a few banks, and private credit lenders active in bridge apartment lending.