April: European Banks are Hot!...Garbage?

A proxy revolucion!; AI is delivering for banks; Two "Buffett" situations; Why LA Banks print money; First Interstate's turnaround (FIBK).

Good morning,

Brief notes:

Proxy season: No Justice, No “Yes” Vote!

It’s proxy voting season. Don’t think of this as paperwork to get off your desk. Corporate executives are telling you their secrets and hoping you don’t pay attention.

Unfortunately, as passive and Robinhood degen behavior take share from long-term investing, the alignment between executives and owners erodes. This influences how executives are incented to treat shareholders.

My personal opinion is that about 1/4 - 1/3 of bank CEOs respect shareholders and treat them well to try to “earn” long-term partners. The rest conclude it is a game (which is it in many sectors), and are happy to extract more than appropriate. In the broader markets, the most egregious example of this is TSLA, with a few highlights below.

In proxy season therefore it is “guilty until proven innocent” and you should use a “no” vote freely.

Shareholder insults to look out for:

Staggered board terms apropos of nothing, to protect boards.

Paying bank executives based on asset size rather than performance. How often do you see small or midsized banks shrink to improve performance? Bank of Hawaii 15 years ago comes to mind, but not many others.

Allow board members to hold almost no stock, so they are incented to sustain independence even if a bank has not earned it.

Pay board members all in cash, implying the stock is less desirable.

DEI policies, which many have a passionate but differing view on and that alone can create issues (in some cases, regulators or exchanges require this policy).

Publish the work of compensation consultants, who tend to try to figure out what executives want (more money obviously), and support raises regardless of performance.

Here Triumph Bancorp (TFIN) is an example. Triumph advertises its compensation consultant as a best practice.

Triumph has missed estimates 8 of the past 12 quarters according to S&P while ROE finished 2024 at 2% after the corporate segment grew expenses 25% annually to $103 million.

Shareholder’s earnings have fallen the past three years, but executive earnings have risen smoothly:

Triumph is not an exception.

Finally, passive funds tend to blindly vote yes, so it’s up to active investors to vote no if they do not like the look and feel of their proxy.

Join the revolution!

On to The Points:

1) European bank stocks are ripping. Try to invest rather than gamble.

I begin with the disclosure that I am not an Euro bank expert, but I can read bank financial statements, and I did a diligence call with a more legitimate expert (@CorpusCol on X) to support the thesis below.

European banks are the hottest trade in financials:

Which one should we buy? European banks have long been uninvestable, but perhaps today is different and we need in. Some such as Aurelius on X and Derek Pilecki of Gator Capital have made good calls here. SocGen in particular has new management, a share repurchase in place, and is looking to improve costs while investing in digital. Their shares used to trade at book value but now are at a discount even after the run up. There are other SocGen types of stories in the EU.

Let’s take a closer look at fundamentals, flows, sentiment, and whether any worth a closer look.

And I’ll put the answer up front - if you are looking to “play the European banks” and spray buy orders across Barclays, SocGen and Deutsche you may as well just go to the Wynn because the companies’ performance is on par with the worst US banks.

However you can also spend time to find smaller, better constructed banks, for example considering the right multiple for Bawag, how to invest in Norway’s Sparebanken or are enjoying AlphaBank’s buyback. That is time well spent.

The “fundamentals” - margins The ECB boosted deposit facility rates to 4% as recently as 2023, so these banks are no longer saddled by negative yielding securities and should see margin expansion.

Except their margins are uniformly Japan-like with the exception of Santander:

What’s up with Credit Agricole? A 0.67% spread - do they allow customers to set their own rates?

No, but they do have a feature where customers fix their mortgage rate a month in advance like in the US. Oh pardon, you can set it 2 years in advance with no mark up! Why would you offer free 2-year put options across your customer base? Another question is, why invest in this?

Returning to macro, rates are now down from 4% to 2.75% in the EU and expected to fall further, so if there were a margin play it would have been in 2022-2023.

So why did shares of banks like SocGen only rip recently?

Beyond fundamentals - it is a mix of flows and sentiment. In thinking of flows, there is the idea that Europeans have massively reallocated home from the US given disrespect from the current US President, profiled more in the linked WSJ article above.

On sentiment, investors like that in SocGen’s case, the bank has disposed of some lower value businesses and reinvested in its own shares at 50-60% of tangible book. This “trade” has gained momentum and taken a life of its own. Many other large European banks make similar promises of efficiency and better capital management. Think in terms of Citigroup and apply it to multiple EU flag bearers.

Below is the slide SocGen proposed in 2023 for a 3 year turnaround: hoping in 3 years to reach below-average metrics by US bank standards

Socgen has a nice play, but would I rather invest in a buyback play of a bank at 50% of book with 3% capital, like Socgen, or a bank at 50% of book with 18-25% capital, like SR Bancorp (SRBK) or Fifth District (FDSB) here in the US?

Frankly while I understand all the arguments around risk-based capital and contingent preferreds I think it unwise to do anything at 3% TCE but grow capital as quickly as possible, and not repurchase anything. If anything I would look to issue equity, even if I had tricked my regulator into thinking my balance sheet had low risk because mortgages have low risk weightings as is the case in Europe.

Let’s buy the laggard then? Maybe some other banks have yet to rip. UBS is only up a few percent recently.

No.

UBS’ 2024 results suggest the bank is being run for customers and employees instead of shareholders.

We know UBS is run for employees because despite being 80% fees, it only runs about 16% operating margins (the reverse of the efficiency ratio, below).

In comparison, Morgan Stanley with a similar percentage of fee income has margins almost double, and ROE triple

Granted, UBS likely is still spending on Credit Suisse integration but the fact remains that the three banks highlighted below are all less efficient than Citi, which itself is a joke among US bank investors for its inefficiency. Literally, the joke goes “Citi is a big company - how many people work there? Half of them.”

Turning from efficiency, we know UBS is run for customers because its margin is less than half a percent, instead of 3%+ at the wealth banks Colarion likes to invest in. Granted, it is easier to grow this way. Any of us with rich friends probably know someone who has a relationship with UBS.

But again, do you want to invest in the company that competes so aggressively on price that it can’t earn its cost of capital?

So we have buybacks at 30x leverage and lending at half a percent over the risk free.

Deutsche, same thing. “We are on the path to reach 10% ROTE”.

DB is 25x levered. If several of the LA banks mentioned in point 4) below were running 4% TCE they would print 35% ROE.

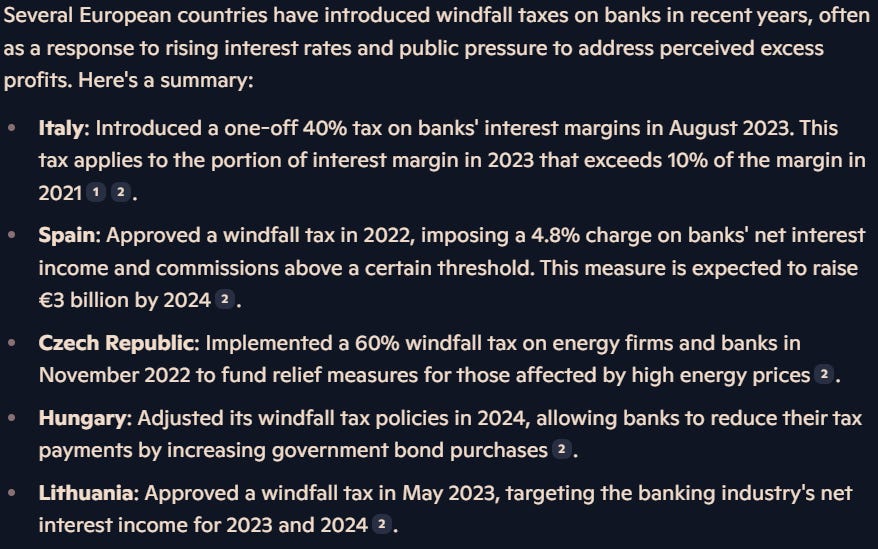

By the way, Europe is about to spend several hundred billion on defense, funded by debt, which may be funded by….bank windfall taxes. According to CoPilot:

And I have read reports that a trade war is about to start.

If I can find a reason that these structural issues are being addressed - low growth mindset, no spread, no capital, inefficient - then I can get on board some larger EU banks. If it’s a trade on momentum, then I’m not very good at that and will leave it to others.

There are however some European banks I would look closely at. I have mentioned three at the top of this note and will spend some time on them as well as others (Irish, Dutch etc) in the next edition of 5 Points.

2) It’s not all hype - some smaller banks are generating returns for shareholders through AI

Returning to the small / microcap US financial sector, in 2025 there are two types of banks:

Those that employ coders on staff

Those that don’t.

If I could distill the banks in category 1, and focus further on just the smaller banks, I would expect strong outperformance from that subgroup over time (this is a core Colarion investment principle in this sector).

Where does AI fit in? As you may know, software development with AI is like giving a racecar driver an engine with more cylinders.

Let’s look at examples from Axos (AX), Customers (CUBI) and FFB Bancorp (FFBB).

Axos (AX) for business development has a software inside a platform called Zenith. Among many other things, it helps entertainers do their taxes. City National founded this line of business but Axos has muscled in, in which entertainers traveling across states have a way to record all the different levies from Florida to New York depending in what state for example Lebron James plays basketball or Taylor Swift holds a concert.

Unfortunately, like most software, Axos’ product gradually became dated so they sought to rebuild it. In years prior this would cost millions in developer time. Today it gets done quickly with help from automation and checked by those same developers.

Axos further branched Zenith out beyond entertainment, and incorporated machine learning inside the customer experience. Axos’ developers worked together with a firm called Ascendion to put it together and now not only is Axos part of a powerful duopoly deposit generation platform, it has a head start building other such niche use cases.

FFB (FFBB) for regulatory response

Readers know that FFB Bancorp was recently the target of a consent order from the FDIC and state related to their payments vertical. Regulators want FFBB to know their customer’s customer, which had not been a focus before (wait until they learn who Tether provides payments for!).

FFB therefore gets to go through millions of payments processed, and prove the negative.

It’s absurd in some ways but technology comes to the rescue.

The bank aggregates its payment data into a “data lake”, and has AI scan the lake for the answers to regulatory questions.

FFBB is hoping to get out of its consent order this year as a result. Like medical progress with torn ACLs or achilles, it seems the needlessly long regulatory calendar is being compressed thanks to technology.

Customers (CUBI) for workflow and “BS management”.

“BS management” in this case does not mean “balance sheet management”

Moody’s, S&P, Mckinsey, DC law firms, and Accenture…they all give regulatory cover, stamp processes as a "disinterested” third party, and charge elevated fees.

Saavy banks like Customers manage these processes tightly. In speaking to bank CEO Sidhu, the bank uses AI wherever it can to “draft” processes before involving expensive third parties.

Think for example if you are starting an LLC and you want an operating agreement. You can hire a $1k / hr attorney to draft the agreement, and he will begin a 90 page opus of complexity. Or you can enter parameters plus ask for recommended inputs from Claude, then have it professionally reviewed.

Customers Bank similarly can use AI to assist with things like testing reserve levels, figuring out loan profitability, or running compensation analysis.

Sorry, Ernst & Young.

3) The “Buffett Banks”: Marathon Bancorp (MBBC) and Bancorp (TBBK)

"When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact" - Warren Buffett

“You should invest in a business that even a fool can run, because someday a fool will.” also Warren Buffett.