5 Points Mid Month: Rebutting Some Doom

Consistency on sale, the 6x earnings high performer, Fintech lender waste, Bank classified asset trends, Repurchase walking the walk; Puerto Rico's bank paradise

Good morning,

In this 5 Points:

Stock Yards, Lakeland, First Financial, and the value of consistency

In the end, will it be the waste that gets fintech lenders?

Why does FFBB trade at 6x earnings run rate?

Bank classified asset trends

Walking the Walk - many banks boast of repurchases, but keep quiet on offsetting share issuance. These are the banks that actually reduced share count.

Puerto Rico: bank paradise

Brief Notes:

The Notes feature: I used Substack’s notes to write a bit about Community Bank Systems’ (CBU) new CEO after meeting him at a recent conference. Notes is a positive alternative to the Twitter echo chamber of Lehman predictions, and CEO Karaivanov is a rarity in the sector - a 42 year old CEO with a different perspective.

If you own small financials, it’s consumer lending more than CRE that you should be careful with right now.

I won’t get into the lengthy details of CRE loan structures, but the bottom line is, perhaps those consumer delinquency charts I have been publishing showing gradual increase may begin to show a steepening trendline. This was my conclusion from certain specific datapoints learned from meeting 14 bankers at a conference last week.

Why is deposit insurance still just $250,000?

I recently met a bank private equity investor who had begun lobbying on the side. The problem is GOP support is impeded by the Freedom Caucus, and Democrat support requires concessions such as higher non-economic subsidies (“Community Reinvestment”).

Many deposit sweeps exist so that customers don’t have to worry about this, but those providers charge 12-15bp basically for software that can be replicated. Good for them, but perhaps there is a better way.

Over a longer period we might expect certain better-capitalized banks to create their own software co-op, or self-select into an insurance cooperative to supplement FDIC. Many banks have already capitalized in-house captive insurance companies and Massachusetts thrifts already offer unlimited insurance due to a scheme begun decades ago.

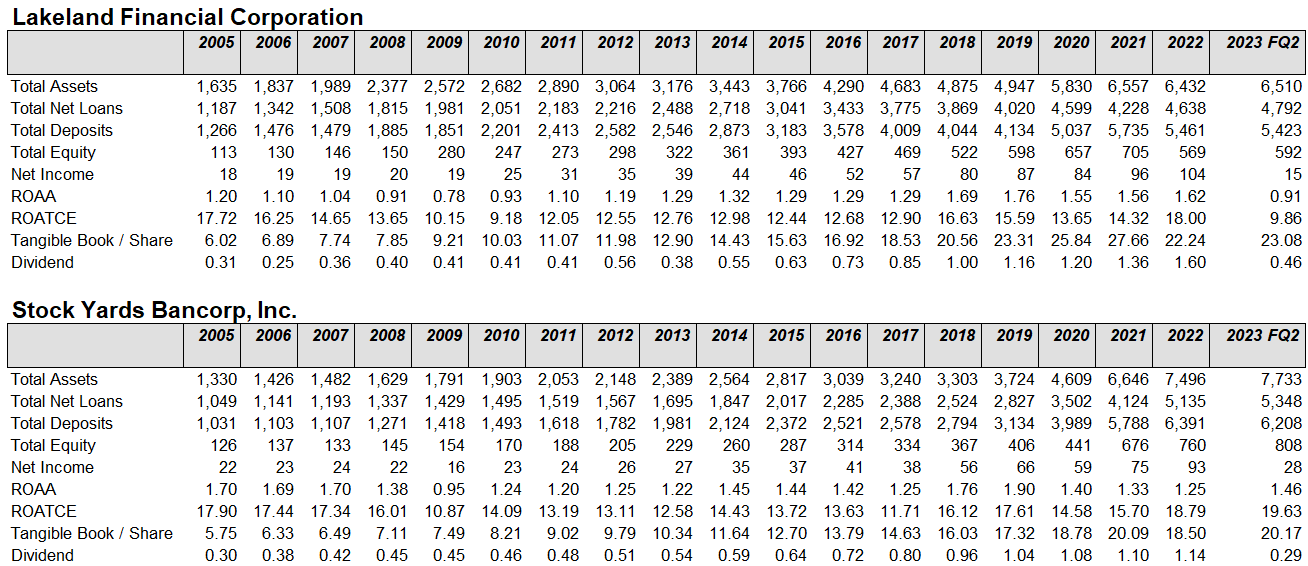

1) The value of consistency: Stockyards ($SYBT), Lakeland ($LBAI), and First Financial (FFIN) among others.

Warren Buffett said he would take a lumpy 15% over a smooth 12%. Maybe he means 15% compounded, rather than a 15% vs a 12% average. It’s drawdown math:

In that vein, let’s look at a few recent losers, the banks profiled at the top of this section. They have all gotten hit about 35%-40% this year

Such cold stocks - some margin compression and trimmed book values are what I see.

Let’s zoom out:

A total return basis shows each a 10x and 20x compounder even after recent drawdowns.

The reasons these stocks have done what they have is shown below is growth in the dividend, tangible book per share, and most importantly, the fact that you can’t tell when the GFC hit, when covid came through etc. These banks never get hit with the lumpy 15% drawdown math.

However these stocks have all gotten nailed this year.

If your timeline is the next 3 months, these stocks may do very little, trading alongside the ETF they belong to, and influenced by bond yields.

If your timeline is 3 years, enjoy the bond discount accretion, the trust cash flows, and a continuation of dividend and income growth. These are powerful machines, not often discounted so much as they are today.