1Q Themes and Specific Situations

1Q dispersion, Short the KRE? William Penn, Esquire, Richmond Mutual, First Sunflower, First Republic

Good evening,

Last edition I mentioned a subscription option for 5 Points to be given to charity. The beginning of month letter will remain the free to all, but for folks helping the children (some subscription proceeds literally go to Children’s Hospital of Alabama Foundation), these paywalled mid-month issues offer broad profiles of certain individual securities, in addition to sector topics.

1. 1Q dispersion: Bank earnings will differ tremendously; look at fixed-rate loans among other items.

I’ve seen several 1Q earnings reports already, across call reports and certain very small banks that have already reported, and have seen a 3% ROE and a 17% ROE.

To keep things simple on what to look for:

Banks with heavy proportion of fixed rate loans will be harder hit.

Low loan / deposit ratio = luxury.

The more sophisticated the depositor base, the more challenging the next two quarters will be, all else equal.

Deposit verticals can be valuable right now. Banking-as-a-service banks (compliance is key in this vertical) are well positioned, as one example.

Some country banks might not show much difference from 4Q.

Large banks should have no issue on net interest income (see below), all seemingly having little incremental need for deposits:

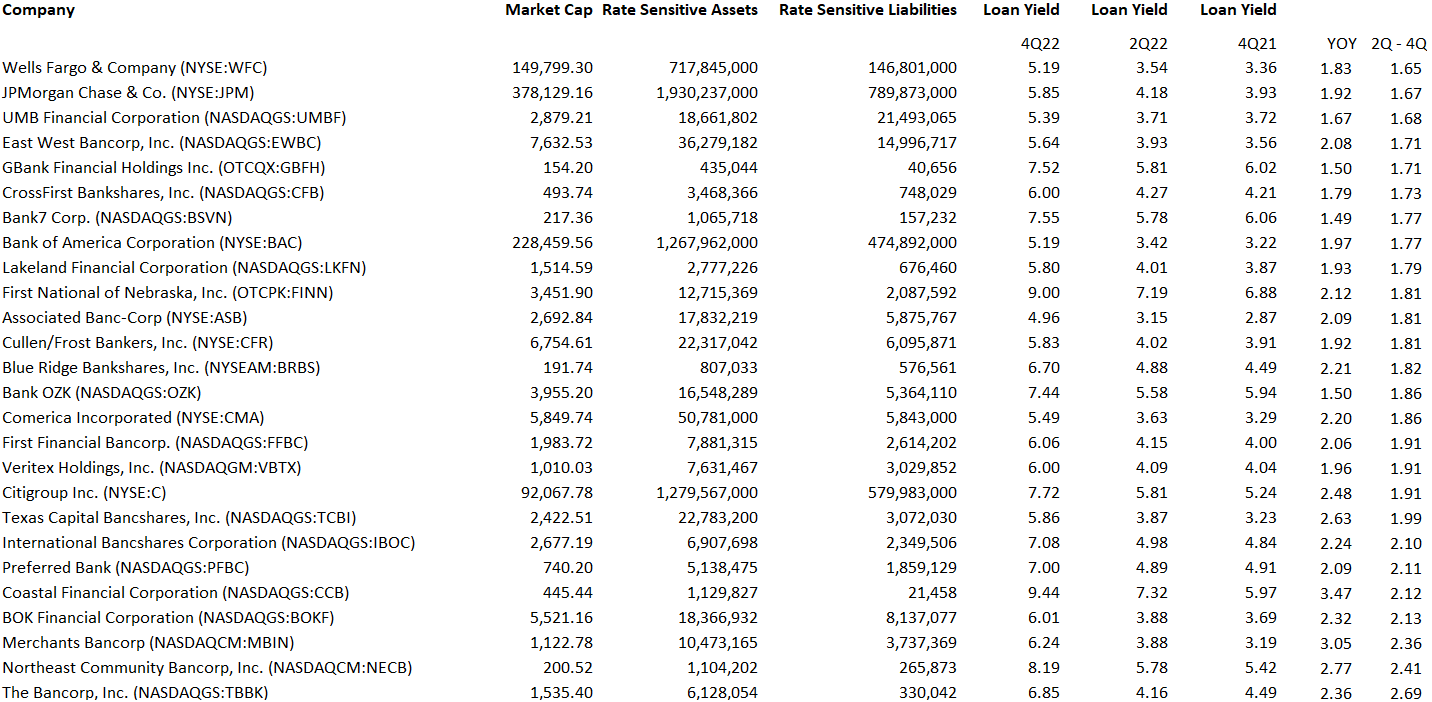

There isn’t room here to screen all the pertinent drivers. However one starting point is to look at banks that have been able to raise loan yields with higher interest rates, to help offset wherever deposit costs may go. Many of these banks are business lenders. In contrast, longer-dated CRE and residential fixed-rate mortgages are the proverbial old maid.

Below is a basic screen of some banks over $100mln market capitalization that did not have much luck raising loan yields during the second half of last year:

And below are some that have:

Bear in mind these are not static situations - some companies may be growing credit risk within their loan book (CCB’s partners for example), and we are not even looking at securities holdings.

But if you are looking for compressed margins along the lines of what FNBT just reported (to 1.75%), then the screen on top will hold several candidates.